Dual Pressure Quantitative Trading Strategy

Overview

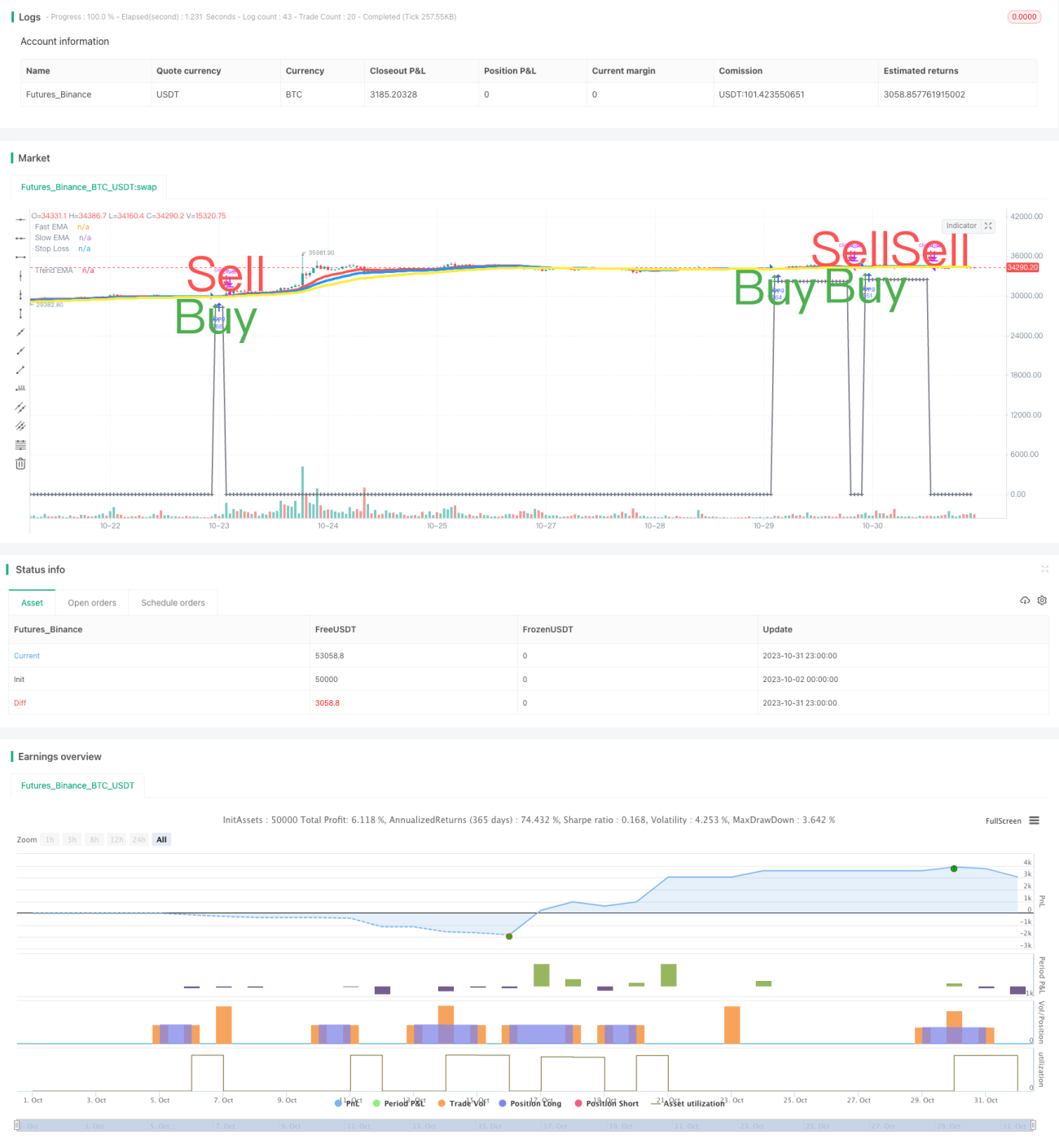

The Dual Pressure quantitative trading strategy is a trend following strategy that combines Stochastic and volume indicators. It mainly uses the Stochastic K and D lines together with volume indicators to generate buy and sell signals, complemented by moving average crosses for additional signals.

Strategy Logic

Buy Signals

The main buy signal triggers when:

-

Both K and D lines cross below oversold area (e.g. 20) and turn up, and both K and D are rising

-

Volume is above a threshold (e.g. 1.4 times average volume)

-

Close is above open (white candle)

Additional buy signals can come from:

-

Golden cross: Fast EMA crosses above slow EMA, both rising

-

Both K and D rise from low into middle zone (e.g. from below 20 to 20-80)

Sell Signals

Main sell signals trigger when:

-

Both K and D enter overbought area (e.g. above 80)

-

Death cross: Fast EMA crosses below slow EMA

-

K crosses below D, and both K and D are falling

Stop Loss

A percentage (e.g. 6%) below buy price is set as stop loss level. Falling below triggers stop loss.

Advantage Analysis

- Dual stochastic avoids false signals

- Volume filters noise and ensures trend

- Multiple signals combined improve accuracy

- Moving averages assist overall trend

- Stop loss controls risk

Advantage 1: Dual Stochastic Avoids False Signals

Single stochastic can generate many false signals. The dual stochastic combination filters false signals and improves reliability.

Advantage 2: Volume Filters Noise and Ensures Trend

The volume condition filters low volume non-trending spots and reduces risk of being trapped.

Advantage 3: Multiple Signals Improve Accuracy

Multiple indicators must align to trigger real trading signals. This improves signal reliability.

Advantage 4: Moving Averages Assist Overall Trend

Rules like dual moving averages ensure signals align with overall trend. This avoids counter-trend trades.

Advantage 5: Stop Loss Controls Risk

The stop loss logic realizes profits and controls loss on single trades.

Risk Analysis

- Parameters need careful optimization, improper settings lead to poor performance

- Stop loss placement must consider gap risk

- Liquidity risk should be monitored for trading instruments

- Lookback issue between different timeframes

Risk 1: Parameters Need Careful Optimization

The strategy has multiple parameters. They need optimization for different instruments, otherwise performance suffers.

Risk 2: Stop Loss Placement Must Consider Gap Risk

The stop loss point should account for price gapping scenarios. It should not be too close to buy price.

Risk 3: Monitor Liquidity Risk

For illiquid instruments, volume rules may filter too many signals. Volume thresholds need to be relaxed.

Risk 4: Lookback Issue Between Timeframes

Misalignment between signals on different timeframes may happen. Signals must be verified to match.

Enhancement Opportunities

The strategy can be enhanced in areas like:

-

Optimize parameters for robustness

-

Introduce machine learning for adaptive parameters

-

Improve stop loss strategy to reduce stop loss rate

-

Add filters to reduce trade frequency

-

Explore conditional orders or profit taking to improve reward

Opportunity 1: Optimize Parameters for Robustness

Methods like genetic algorithms can systematically optimize parameters for stability across market regimes.

Opportunity 2: Introduce Machine Learning for Adaptive Parameters

Models can assess market conditions and adjust parameters accordingly, achieving dynamic optimization.

Opportunity 3: Improve Stop Loss Strategy to Reduce Stop Loss Rate

Better stop loss algorithms can reduce unnecessary stops while maintaining risk control.

Opportunity 4: Add Filters to Reduce Trade Frequency

Strengthening filters can reduce trade frequency, lower costs, and improve per trade returns.

Opportunity 5: Explore Conditional Orders or Profit Taking

According to market conditions, conditional orders or profit taking strategies can better maximize profit while controlling risk.

Conclusion

The strategy balances trend, risk control, costs and other aspects. The core advantages are dual stochastic plus volume for trend and stop loss for risk control. Next steps are to enhance robustness, adaptive parameters, stop loss optimization etc. to yield steady profits in more market regimes.

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// SW SVE - Stochastic+Vol+EMAs [Sergio Waldoke]

// Script created by Sergio Waldoke (BETA VERSION v0.5, fine tuning PENDING)

// Stochastic process is the main source of signals, reinforced on buying by Volume. Also by Golden Cross.- 1