Monday Reversal Intraday Trend Following Strategy

Overview

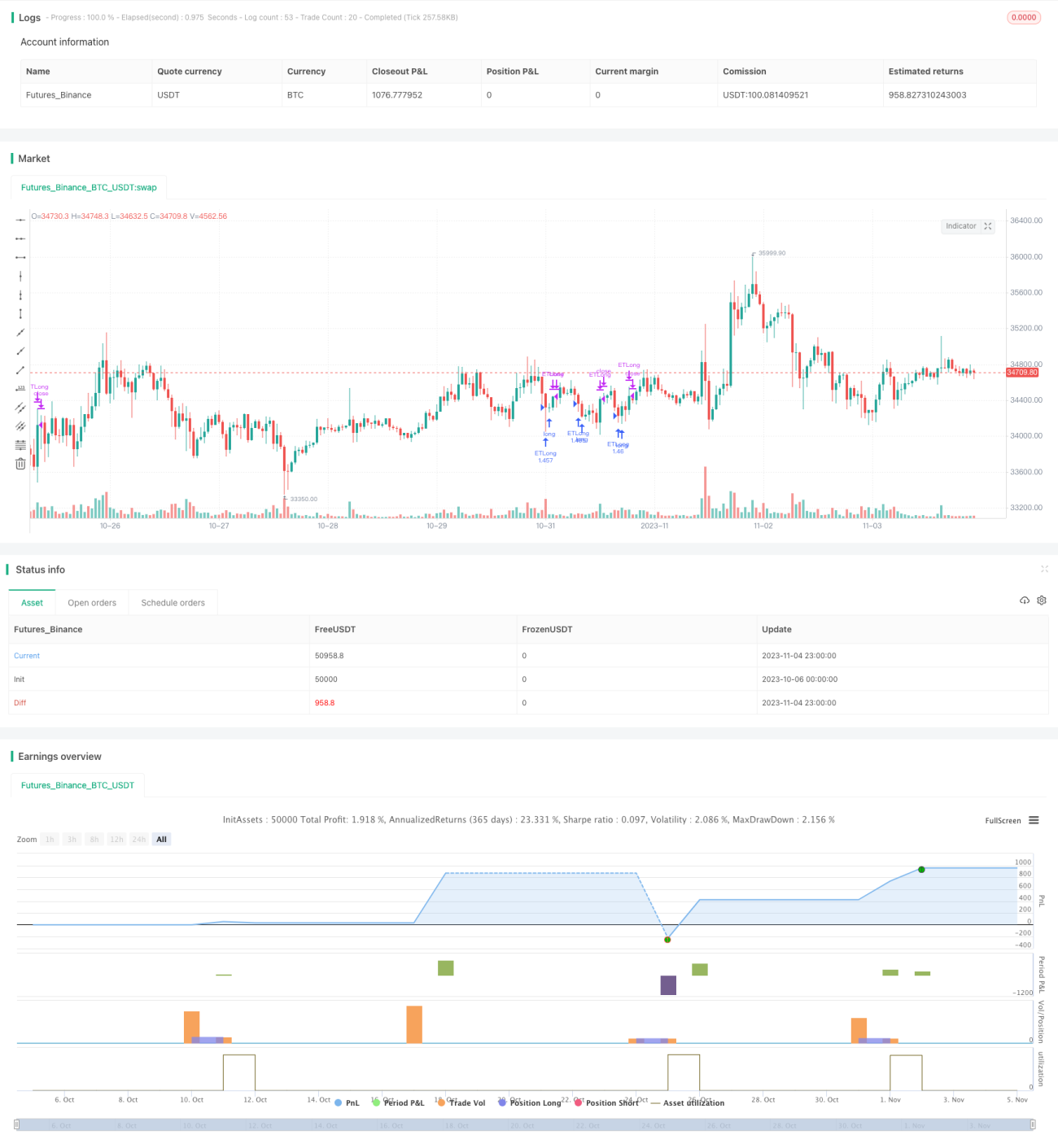

The main idea of this strategy is to profit from Monday's intraday reversal using trend following.

Principles

The core logic is:

-

Check if it is Monday, if yes, continue to next steps;

-

Identify if an uptrend reversal pattern exists - Close[1] < Close[2] and Close[2] < Close[3];

-

If reversal pattern confirmed, go long at the close of 3rd bar to follow the trend;

-

Exit if today's high is breached, or stop loss is hit;

-

Close position after 6 hours.

The strategy capitalizes on specific Monday reversal, identifies reversal patterns to go long at relative lows for profits. Stop loss in place to control risks.

Advantages

The biggest advantages are:

-

Profits from Monday reversals during specific periods;

-

Clear entry signals from reversal candlestick patterns;

-

Stop loss and take profit to control risks;

-

Trend following approach maximizes profits;

-

Simple and easy to understand logic;

Risks

There are some risks:

-

Losses if Monday reversals not significant;

-

Price may retrace after entry leading to stop loss;

-

Sudden market changes may result in large stop loss;

-

Holding too long may also lead to losses;

The solutions are optimizing stop loss, shortening holding time, and controlling single loss size.

Enhancements

The strategy can be improved by:

-

Using machine learning to identify reversals more accurately;

-

Optimizing stop loss strategies like trailing stop or partial stop loss;

-

Incorporating more factors to judge trend strength;

-

Dynamically adjusting holding time;

-

Using algorithms to find optimal parameters;

-

Adding position switching for two-way trading;

These can increase the win rate and profitability.

Conclusion

In conclusion, the strategy capitalizes on Monday reversals, with clear entry/exit rules, to implement a simple trend following strategy. It can achieve better results than fixed stop loss/take profit. Further optimizations are needed to address market uncertainty. The strategy provides a reference for intraday trading.

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("ET Forex TurnaroundMonday", overlay=true)

FirstYear = input(2018, minval=2000, maxval=2023, step=1)

FirstMonth = 1 //input(1, minval=1, maxval=12, step=1)- 1