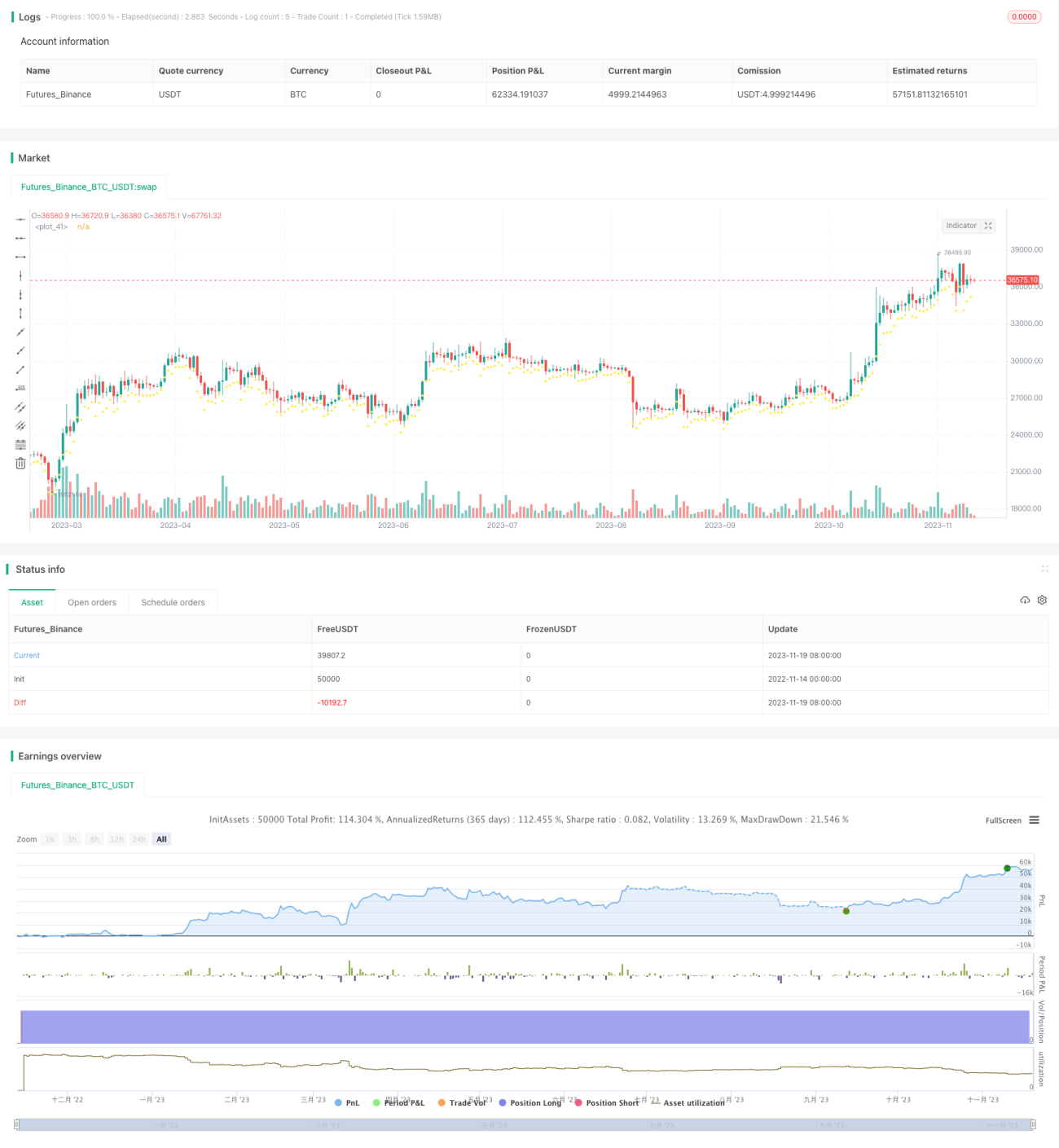

Dual-direction Volatility Swallowing Strategy

Overview

This strategy is a dual-direction trading strategy that tracks volatility. It uses the Average True Range (ATR) indicator to set stop losses and determines the trend direction based on the price breaking through the stop loss level. It opens reverse positions when the trend direction changes.

Strategy Logic

The strategy uses 3-day ATR to calculate volatility. The ATR value multiplied by a coefficient is used as the stop loss level. When the price is above the stop loss level, it judges it as an uptrend and closes long positions when the price falls below the stop loss level. When the price is below the stop loss level, it judges it as a downtrend and closes short positions when the price rises above the stop loss level. It opens reverse positions when the trend changes. The stop loss level is optimized during trends and reset when trends change.

Advantage Analysis

- Uses ATR to dynamically track market volatility and lower the chance of stop loss being hit

- Dual-direction trading profits from market fluctuation

- Opens reverse positions early in trend changes for higher win rate

Risk Analysis

- Extreme volatility may cause stop loss fails as ATR lags

- GAP risk exists for long positions

- May trade small profits frequently

To mitigate risks: increase ATR coefficient for wider stop levels, limit trade frequency, set minimum take profit levels, etc.

Optimization Directions

- Combine other indicators for trend change signals

- Optimize ATR parameters

- Add trade sizing control

Summary

This is an overall stable dual-direction trailing stop strategy. ATR sets dynamic stop levels to control drawdowns. Dual-direction trading also increases profit chances. Further optimizations can make the strategy more robust, enhancing trend following capabilities.

/*backtest

start: 2022-11-14 00:00:00

end: 2023-11-20 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("BCH Swinger v1", overlay=true, commission_value = 0.25, default_qty_type=strategy.percent_of_equity, default_qty_value = 100)

/////////////////////////////////////////////////////////////- 1