Traffic Light Trading Strategy Based on EMA

Overview

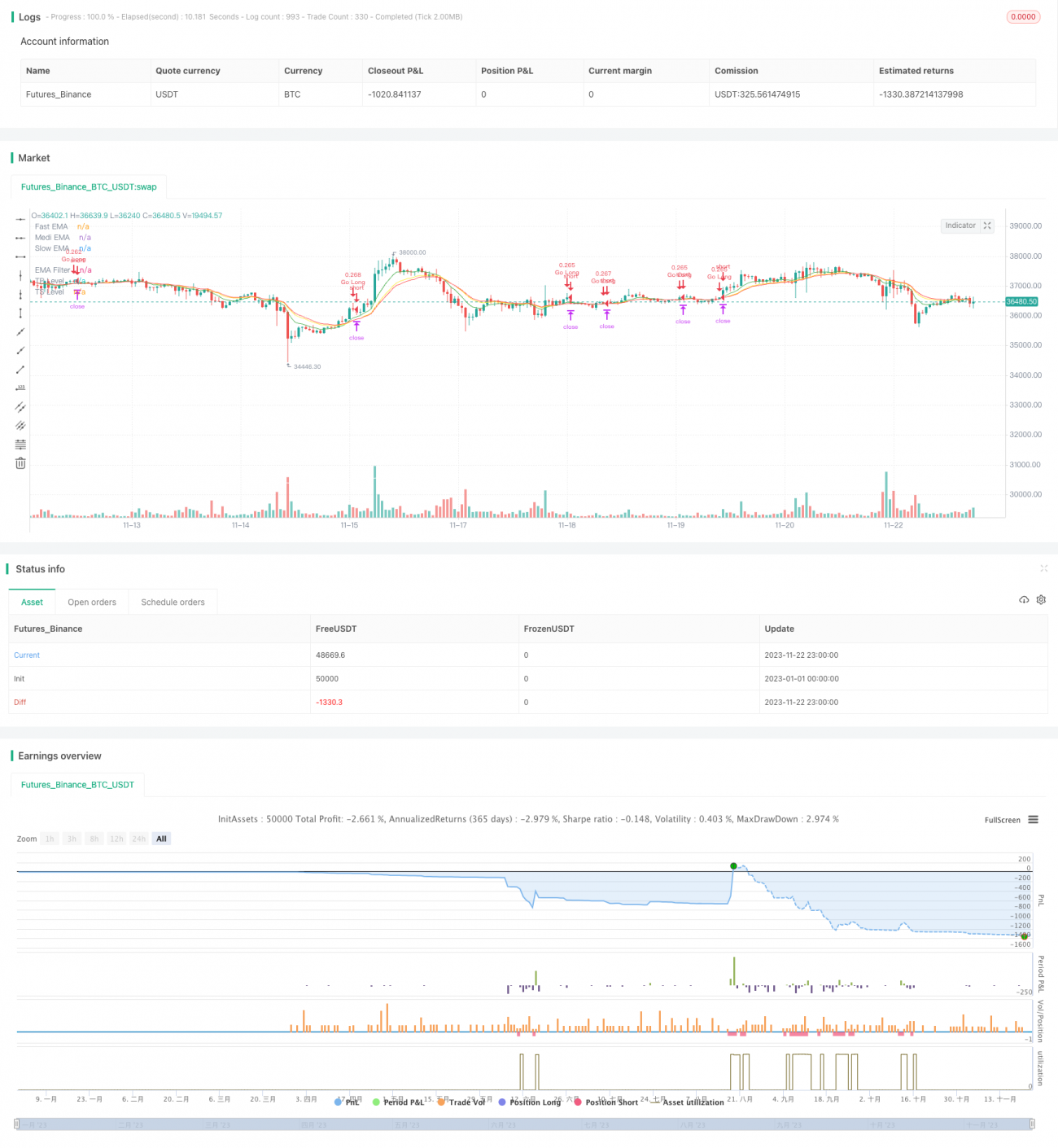

This strategy uses 4 EMA lines of different periods to generate trading signals based on their arrangement order, similar to the red, yellow and green traffic light. So it is named “Traffic Light Trading Strategy”. It comprehensively judges the market from both trend and reversal perspectives, aiming to improve the accuracy of trading decisions.

Strategy Principle

-

Set up 3 EMA lines of fast (8 periods), medium (14 periods) and slow (16 periods), plus 1 long-period (100 periods) EMA line as a filter.

-

Determine long and short opportunities based on the order of the 3 EMA lines and their crossover with the filter:

-

When fast line crosses above medium line or medium line crosses above slow line, it is determined as long signal.

-

When medium line crosses below fast line, it is determined as close long signal.

-

When fast line crosses below medium line or medium line crosses below slow line, it is determined as short signal.

-

When medium line crosses above fast line, it is determined as close short signal.

- Judge the trend direction and strength through the order of the 3 EMA lines, combined with the crossover between the EMA lines and filter to determine reversal points, which organically incorporates trend following and reversal trading.

Advantage Analysis

This strategy integrates the advantages of both trend following and reversal trading, which can grasp market opportunities well. The main advantages are:

- Using multiple EMA lines makes the judgment more solid and reduces false signals.

- Flexible settings for long and short conditions avoid missing trading opportunities.

- The combination of long-period and short-period EMA lines makes comprehensive judgments.

- Customizable profit taking and stop loss allows better risk control.

Through parameter optimization, this strategy can adapt to more products and has demonstrated strong profitability and stability in backtests.

Risk Analysis

The main risks of this strategy lies in:

- When the order of the multiple EMA lines becomes messy, it increases the difficulty in judgment and causes hesitation in trading.

- It cannot effectively filter out the false signals from abnormal market fluctuations, which may cause losses in significant volatility.

- Improper parameter settings may result in over-relaxed or over-strict stop profit/loss criteria, leading to missing profits or over-losses.

It is suggested to further improve the stability of the strategy and control risks by optimizing parameters, setting stop loss level, trading cautiously etc.

Optimization Directions

The main optimization directions of this strategy:

- Adjust the cycle parameters of EMA lines to adapt to more products.

- Add other indicators like MACD, Bollinger Bands etc to increase judgment accuracy.

- Optimize profit taking/stop loss proportions to achieve the best balance between risk and return.

- Add adaptive stop loss mechanisms like ATR Stop Loss to further control downside risk.

Continuous enhancement in stability and profitability of the strategy can be achieved by introducing parameters adjustments and risk control measures in multiple aspects.

Conclusion

This Traffic Light Trading Strategy incorporates trend following and reversal trading by using 4 sets of EMA lines to form trading signals. It has demonstrated strong profitability through parameter optimization to adapt to more products. Going forward, by further strengthening risk control and introducing diversified indicators, it has the potential to become a stable and efficient quantitative trading strategy.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1