Dual EMA Golden Cross Trading Strategy

Overview

This strategy combines dual EMA golden crosses, normalized ATR noise filter, and ADX trend indicator to provide more reliable buy signals for traders. It integrates multiple indicators to filter out false signals and identify more reliable trading opportunities.

Strategy Principle

The strategy uses 8-period and 20-period EMAs to build a dual EMA golden cross system. It generates buy signals when the shorter period EMA crosses above the longer period EMA.

In addition, the strategy has set up several auxiliary indicators for filtering:

-

14-period ATR, normalized to filter out minor price fluctuations in the market.

-

14-period ADX to identify the strength of trends. Trades are considered only in strong trends.

-

14-period SMA of volume to filter out time points with small trading volumes.

-

4/14-period Super Trend indicator to judge bullish or bearish market direction.

Only when the trend direction, normalized ATR value, ADX level and volume conditions are met, the EMA golden cross will eventually trigger the buy signal.

Strategy Advantages

-

Reliability from multiple indicators combination

Integrating indicators like EMA, ATR, ADX and Super Trend forms a strong signal filtering system, higher reliability.

-

More flexibility in parameter tuning

Threshold values of normalized ATR, ADX, holding period etc. can be optimized, higher flexibility.

-

Distinguishing bull and bear markets

Identify bull and bear markets using Super Trend, avoid missing opportunities.

Strategy Risks

-

Difficulty in parameter optimization

Too many parameters, difficulty in finding the optimum combination.

-

Risk of indicator failure

There is still risk of false signals due to lagging nature of indicators. Proper stop loss theory needs consideration.

-

Low trading frequency

Frequency tends to be low due to multiple filters, long no-trade duration possible.

Optimization Directions

-

Optimize parameter combination

Finding optimum combination requires large amount of backtesting data.

-

Incorporate machine learning

Use ML algorithms to automatically optimize parameters over time. Improve adaptiveness.

-

Consider more market factors

Combining indicators of market structure, emotions etc. improves diversity.

Conclusion

This strategy comprehensively considers trend, volatility and volume price factors. Through multi-indicator filtering and parameter tuning, it forms a reliable trading system. The reliability is high and can be further improved via optimization.

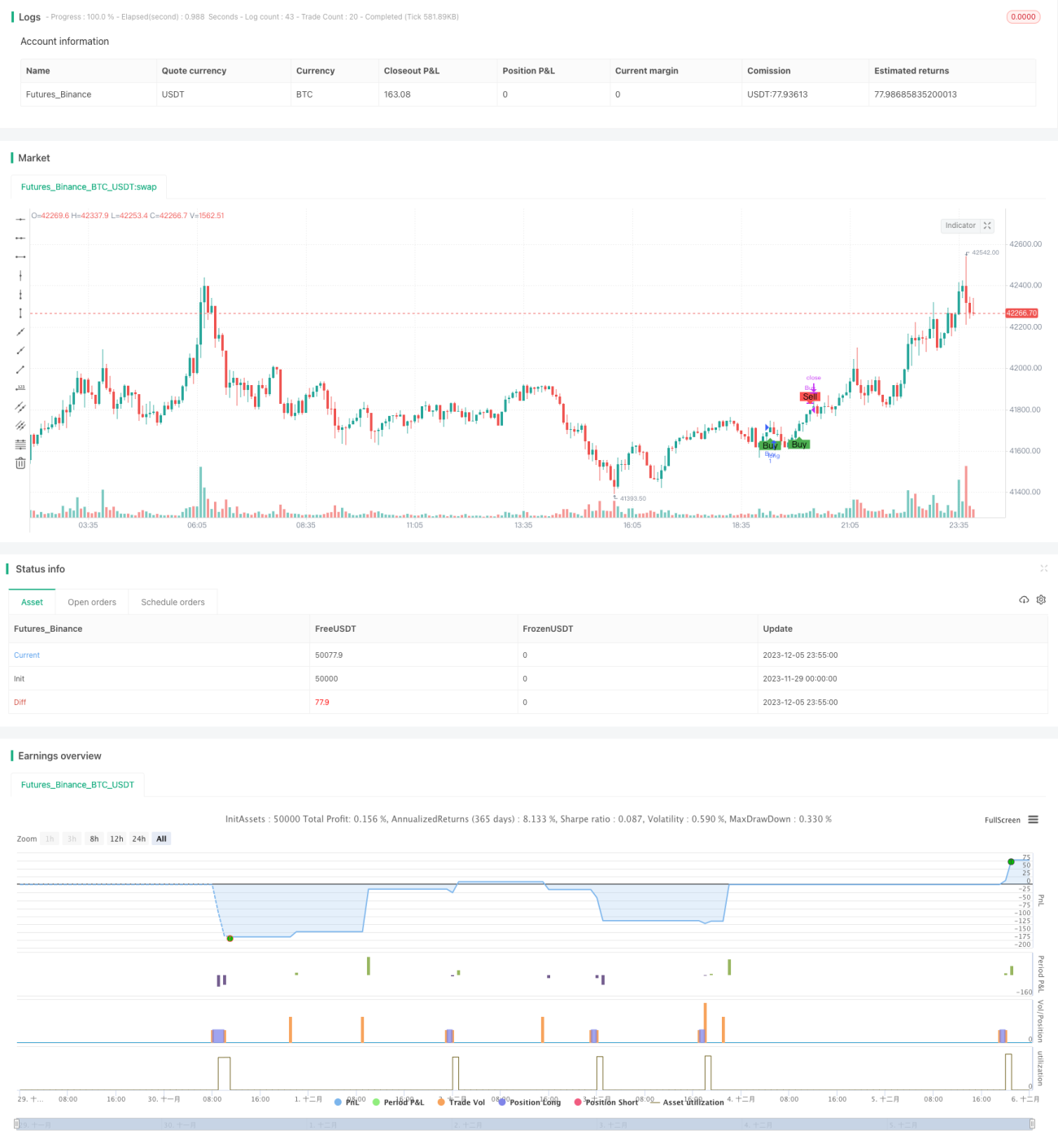

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Description:

//This strategy is a refactored version of an EMA cross strategy with a normalized ATR filter and ADX control.

//It aims to provide traders with signals for long positions based on market conditions defined by various indicators.- 1