Bitcoin Trading Strategy Based on Quantitative Indicators

Overview

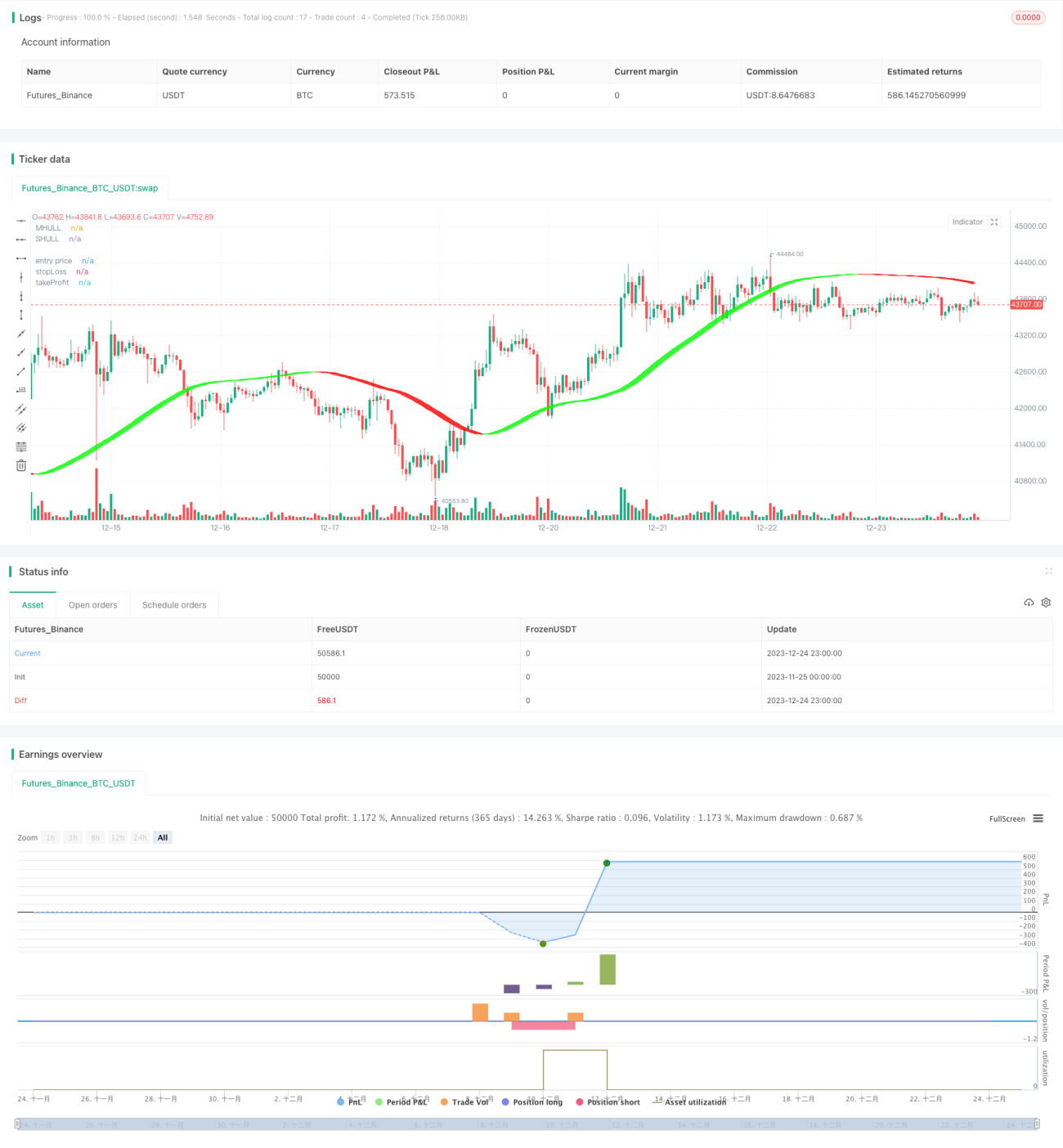

This strategy uses multiple quantitative indicators to determine the timing of buying and selling Bitcoin and automate trading. It mainly includes the Hull indicator, Relative Strength Index (RSI), Bollinger Bands (BB) and Volume Oscillator (VO).

Strategy Principle

-

Use the modified Hull Moving Average to determine the main trend direction of the market, combined with Bollinger Bands to assist in determining breakout buy and sell points.

-

The RSI indicator combined with an adaptive volatility range determines the overbought and oversold zones to generate trading signals. Two sets of parameters are also set up for duplicate signal verification.

-

The Volume Oscillator determines the momentum of buying and selling to avoid false breakouts.

-

Set stop loss/take profit ratios in advance to preset stop loss and take profit levels for risk management.

Advantage Analysis

-

The Hull curve can capture trend changes faster, and Bollinger Bands can help reduce false signals.

-

Optimization of RSI parameters and verification of duplicate signals make it more reliable.

-

Volume Oscillator combined with trends and indicator signals avoids inaccurate trading.

-

Preset stop loss and take profit methods can automatically control single profit and loss and effectively manage overall risk.

Risk Analysis

-

Improper parameter settings may result in too high trading frequency or deteriorated signal performance.

-

Sudden market events may cause prices to fluctuate violently, resulting in stop loss being triggered and greater losses.

-

When the trading variety is changed to other coins, the parameters need to be retested and optimized.

-

If volume data is missing, the Volume Oscillator will fail.

Optimization Directions

-

Test more RSI parameter combinations to find the optimal parameters.

-

Try combining RSI with other indicators like MACD and KD to improve signal accuracy.

-

Add model prediction modules and use machine learning to judge market direction.

-

Test the parameters when applied to other trading varieties.

-

Optimize the stop loss and take profit algorithms to maximize profits.

Summary

This strategy combines multiple quantitative technical indicators to determine entry and exit timing. Through parameter optimization, risk control and other methods, it has achieved automated Bitcoin trading with good results. But it still requires continuous testing and optimization to adapt to market changes. It can serve as a reference for investors to assist in trading decisions.

- 1