Intraday Trend Following Strategy with Multiple Stop Loss

Overview

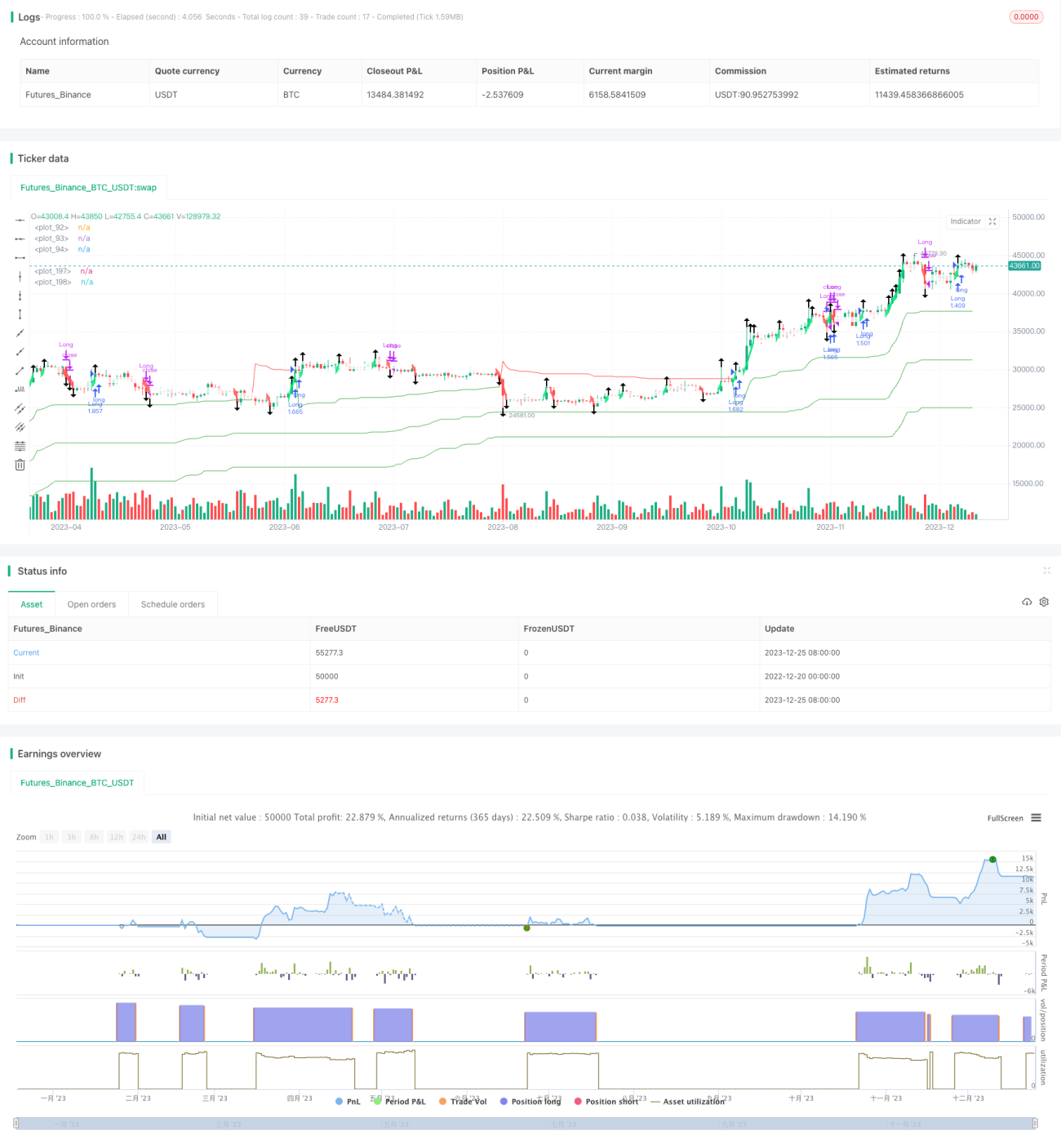

This strategy incorporates multiple ATR trailing stops and an improved Renko bricks to capture intraday trending moves. It combines trend indicators and brick charts to enable multi-timeframe analysis and identify trend direction for effective stops.

Strategy Logic

The core of this strategy lies in the multiple ATR stop loss mechanism. It sets 3 groups of ATR stops - 5 ATR, 10 ATR and 15 ATR. When price breaks these 3 stops downward, it indicates a trend reversal, prompting position exit. Such triple stop setting effectively filters out false signals from short-term noises.

Another key component is the improved Renko bricks. They are partitioned based on ATR values and incorporate SMA to determine trend bias. It is more sensitive than regular Renko bricks in capturing early trend changes. Brick color flip signals stops.

Entry signal triggers when price breaks above 3 ATR stops. Exit when price hits any ATR stop or Renko brick color changes.

Advantages

- Triple stops effectively control risks

- Improved Renko bricks enable early stops

- Combining trend and brick charts ensures catching trends

- Multi-timeframe analysis makes trend identification more reliable

- Adjustable parameters suit different market regimes

Risks and Enhancement

Main risk is stop loss penetration causing extended losses. Can optimize via:

- Adjust ATR stop multiples - relax in strong trends and tighten in weak trends

- Fine-tune Renko brick ATR periods to balance sensitivity and stability

- Add other stop indicators e.g. Donchian Channel for reliability

- Implement filters to avoid whipsaws during consolidations

Conclusion

This strategy works well for strong intraday trends. Its scientific stop loss mechanism and early trend change detection by improved Renko bricks are noteworthy. Fine-tuned parameters can adapt it to varying market conditions. Worth live testing as a trend following system.

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Lancelot vstop intraday strategy", overlay=true, currency=currency.NONE, initial_capital = 100, commission_type=strategy.commission.percent,

commission_value=0.075, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

- 1