Improved RSI Scalping Strategy based on Relative Strength Index

Overview

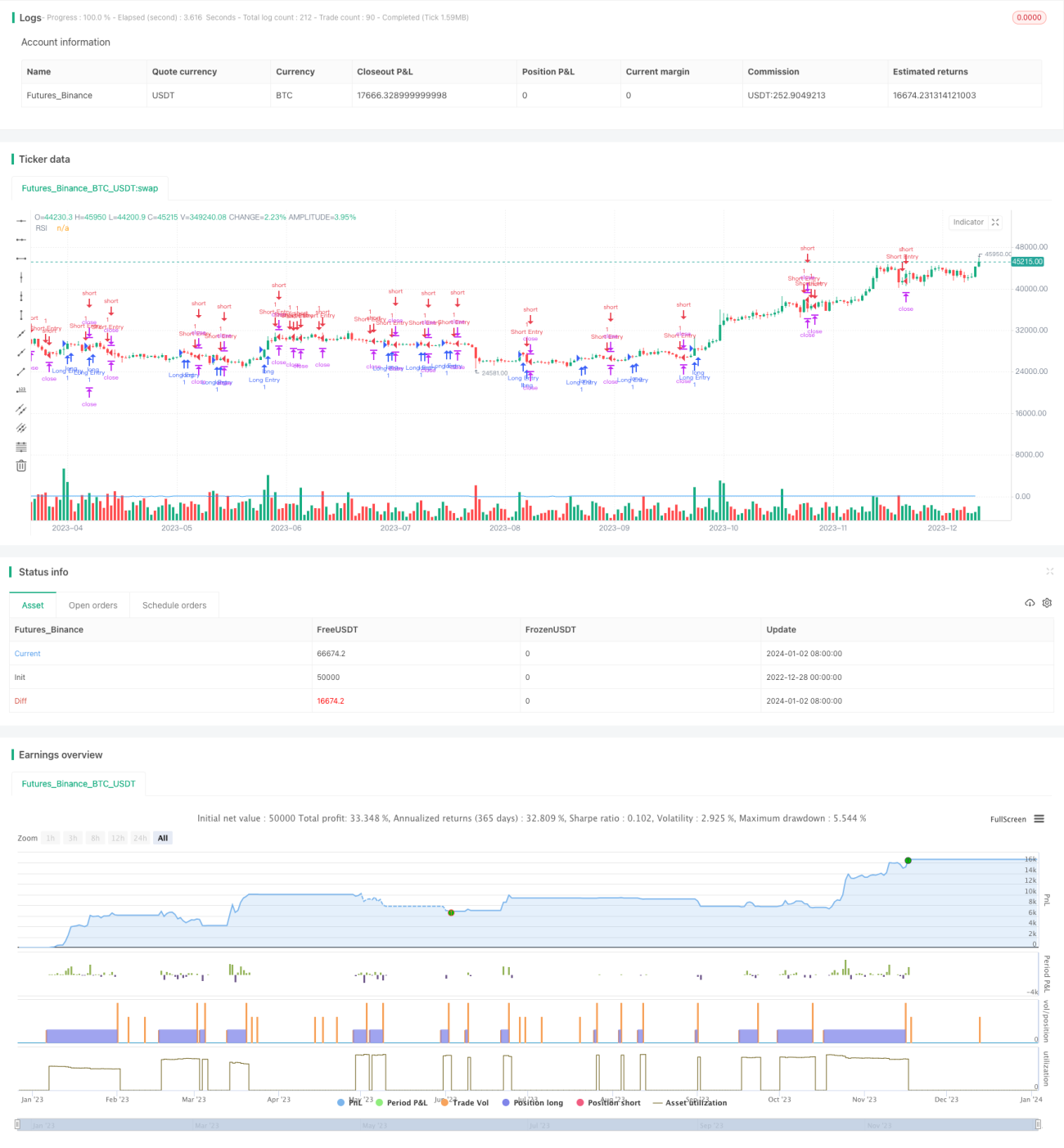

The core idea of this strategy is to combine the RSI indicator and custom AI conditions to discover trading opportunities. It will establish long or short positions when multiple conditions are met, and use fixed take profit and stop loss levels.

Trading Logic

The strategy is implemented through the following steps:

- Calculate 14-period RSI values

- Define two custom AI conditions (long and short)

- Combine AI conditions with RSI overbought/oversold zones to generate entry signals

- Calculate position size based on risk percentage and stop loss pips

- Compute take profit and stop loss price

- Enter positions when entry signals are triggered

- Exit positions when take profit or stop loss is hit

Additionally, the strategy will generate alerts on signal creation and plot RSI values on the chart.

Advantage Analysis

The strategy has several key advantages:

- Combining RSI and AI conditions lead to more accurate trade signals

- Using multiple condition combinations effectively filters out false signals

- Position sizing based on risk management principles controls per trade risk

- Fixed take profit/stop loss provides clarity on risk and reward

- Highly customizable through parameter tuning

Risk Analysis

There are also some risks to consider:

- Incorrect RSI parameters may lead to inaccurate signals

- Poorly designed custom AI logic can generate false signals

- A stop loss level too tight may result in excessive stopping out

- Fixed take profit/stop loss may lose more profits or create more losses in volatile markets

These can be mitigated by tuning RSI parameters, optimizing AI logic, relaxing stop loss distances, etc.

Enhancement Opportunities

Some ways the strategy can be further improved:

- Incorporate more custom AI conditions to determine trend based on multiple factors

- Optimize RSI parameters to find best combinations

- Test different take profit/stop loss mechanisms like trailing stops or moving take profit

- Add additional filters like volume spikes to detect quality trading opportunities

- Employ machine learning to automatically generate optimal parameters

Summary

In summary, this is a highly configurable and optimizable advanced strategy for trading based on RSI and custom AI logic. It determines trend direction through a combination of multiple signal sources, executes trades with risk management and take profit/stop loss procedures. The strategy can provide good trading performance for users, with abundant expansion and optimization capabilities.

- 1