Trend and Oscillation Double Strategy

Overview

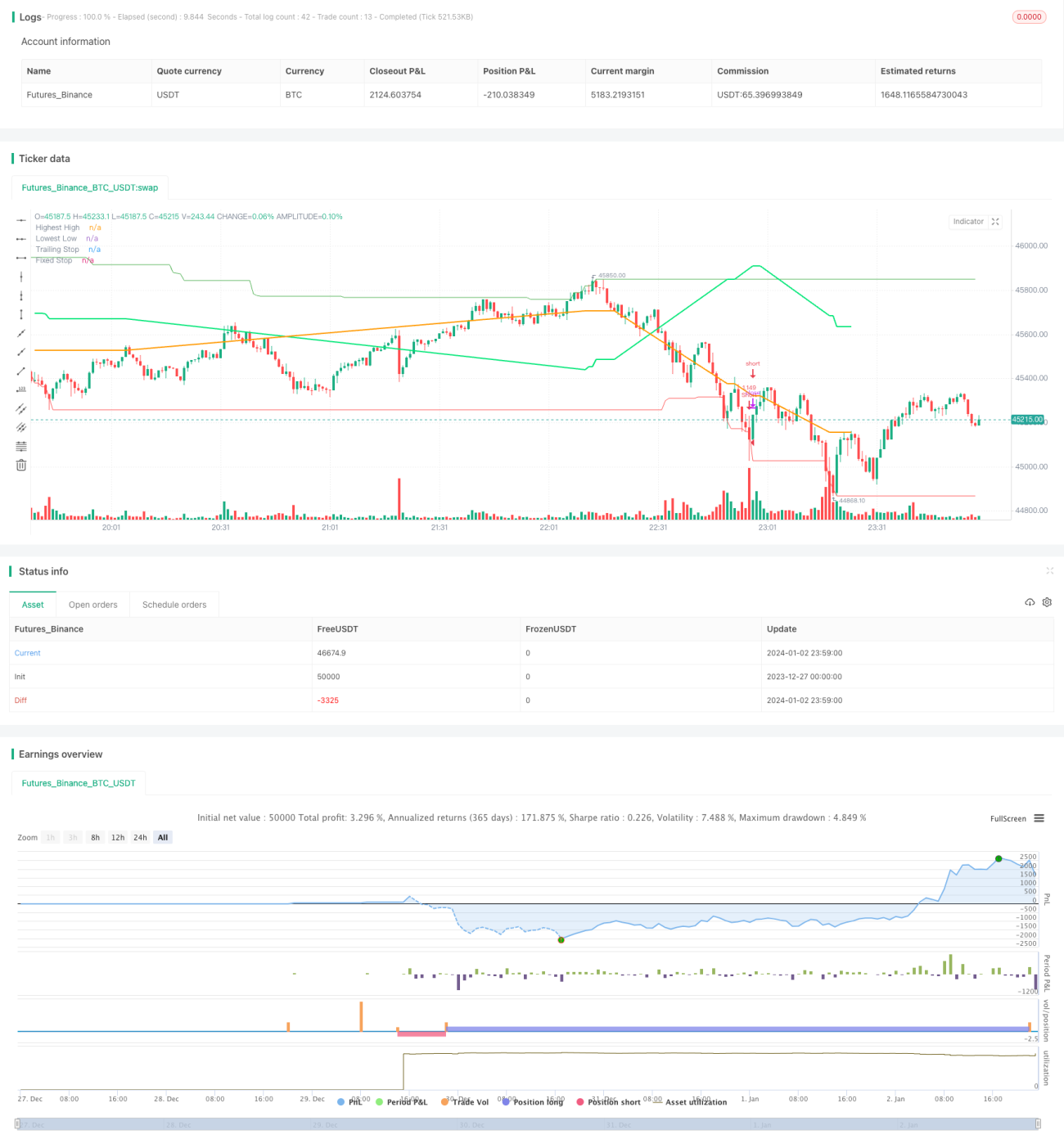

The Trend and Oscillation Double Strategy is a quantitative trading strategy that combines trend and oscillation. It utilizes the combination of two indicators to identify the direction and strength of the trend, and find better entry opportunities during trend oscillations.

Principles

The strategy mainly utilizes two open indicators: Trend Surfers and Mawreez's Trend Oscillator.

Trend Surfers is a trend tracking stop loss indicator. By calculating the highest and lowest prices over a certain period, it judges the price movement and gives suggested stop loss positions. For example, when the price breaks through the highest price of the most recent 168 K-lines, it is a bullish signal; when the price breaks through the lowest price of the most recent 168 K-lines, it is a bearish signal.

Mawreez's Trend Oscillator is a dual-line oscillation indicator. Similar to MACD, it judges the direction and strength of the trend through the difference in DI. The values above 0 axis of this indicator curve indicate bullishness, while those below indicate bearishness.

The trading rules of this strategy are:

Long entry: Buy when Trend Surfers break through the highest line and Mawreez's Trend Oscillator shows bullish signal

Short entry: Sell when Trend Surfers break through the lowest line and Mawreez's Trend Oscillator shows bearish signal

The stop loss method is a combination of trend tracking stop loss and fixed stop loss.

Advantage Analysis

This strategy combines trend and oscillation indicators, which can capture trends and find better entry prices during oscillations. The main advantages are:

- The double indicator filtering can effectively avoid false breakouts

- The combination of trend and oscillation makes it easier to seize the low price in price ranges for bargain hunting or exit at high price for profit taking

- The multiple stop loss methods can control risks very well

Risk Analysis

There are also some risks with this strategy:

- The combination of double indicators may lead to missing trading signals

- Conflicting signals may occur between the trend indicator and oscillation indicator

- Fixed stop loss may stop out too early

To mitigate these risks, the following measures can be taken:

- Relax the parameters of the indicators properly to reduce filtration rate

- Add rules of trend judgment to avoid indicator conflicts

- Dynamically adjust stop loss positions

Optimization Directions

There is room for further optimization of this strategy:

- Test different parameter combinations and cycle parameters to find the optimal parameters

- Increase auxiliary rules based on volatility, trading volume etc.

- Adopt machine learning techniques to dynamically optimize indicators and parameters

Summary

The Trend and Oscillation Double Strategy integrates the advantages of trend tracking and oscillation indicators. It can identify trend directions and seize oscillation opportunities. With parameter and rule optimization, the profitability of this strategy can be further enhanced. This strategy has good prospects for development.

- 1