Multi-timeframe MA Trend Following Strategy

1

Follow

1802

Followers

Overview

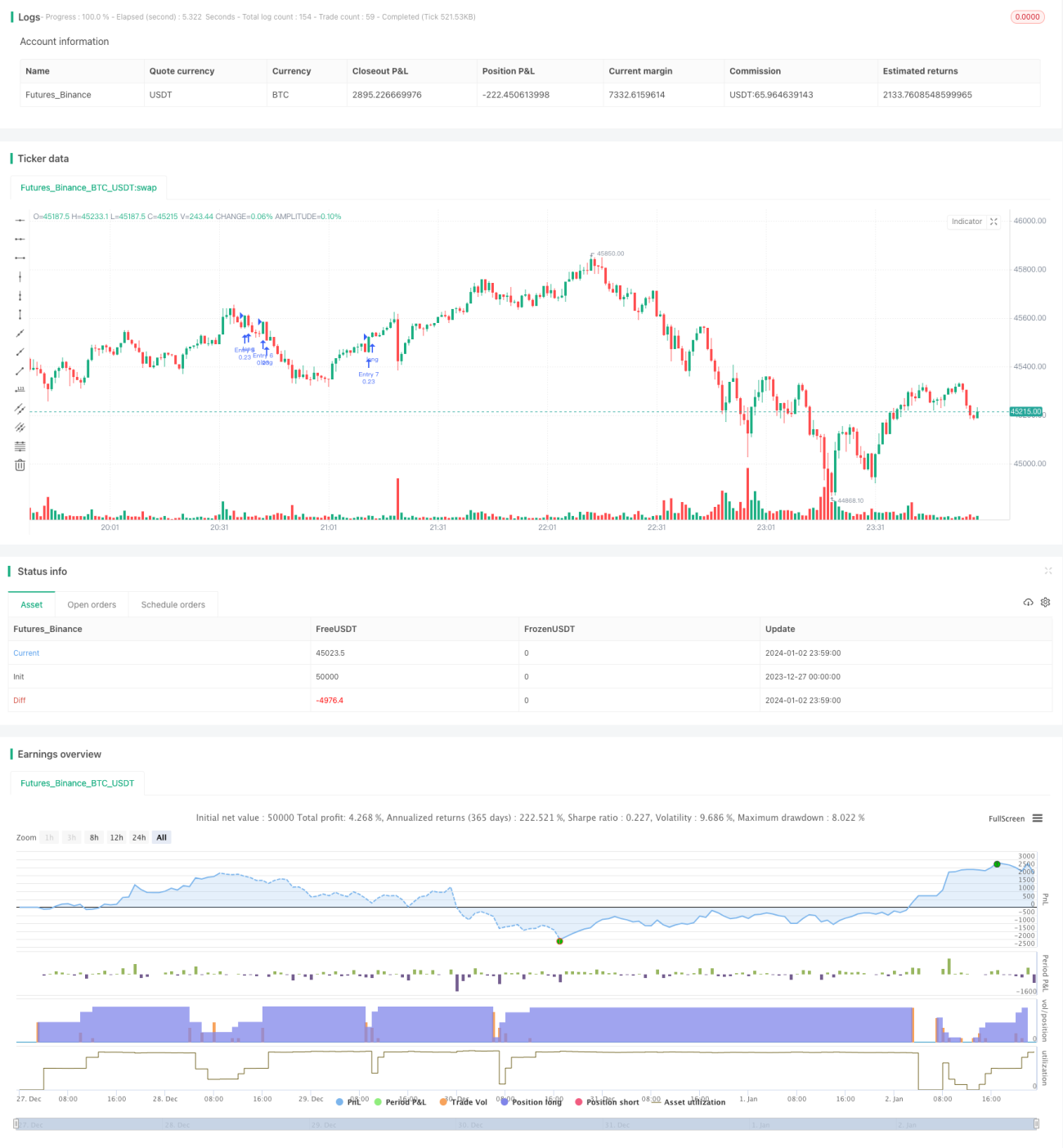

This strategy is based on the multi-timeframe moving average crossover to track middle-long term trends. It adopts a pyramiding position to chase rises and achieve exponential capital growth. The biggest advantage is being able to catch the mid-long term trends and pyramid entries in batches and stages to obtain excess returns.

Strategy Logic

- Build multiple timeframes based on 9-day MA, 100-day MA and 200-day MA.

- Generate buy signals when shorter period MA crosses above longer period MA.

- Adopt 7 staged pyramiding entries. Check existing positions before adding new entry, stop pyramiding when 6 positions already opened.

- Set fixed 3% TP/SL for risk control.

Above is the basic trading logic.

Advantages

- Effectively catch mid-long term trends and enjoy exponential growth.

- Multi-timeframe MA crossover avoids short-term noise.

- Fixed TP/SL controls risk for each position.

- Pyramid entries in batches to obtain excess returns.

Risks & Solutions

- Risk of huge loss if fail to cut loss in trend reversal. Solution is to shorten MA periods and quicken stop loss.

- Risk of margin call if loss beyond tolerance. Solution is to lower initial position size.

- Risk of over 700% loss if strong downtrend. Solution is to raise fixed stop loss percentage.

Optimization Directions

- Test different MA combinations to find optimal parameters.

- Optimize pyramiding stages quantity. Test to find best number.

- Test fixed TP/SL settings. Expand TP range for higher profitability.

Summary

The strategy is very suitable to catch mid-long term trends. Pyramid entries in batches can achieve very high risk-reward ratio. There are also some operation risks, which should be controlled by parameter tuning. Overall this is a promising strategy worth live trading verification and further optimization.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1