Breakout and Intelligent Bollinger Bands Price Channel Strategy

Overview

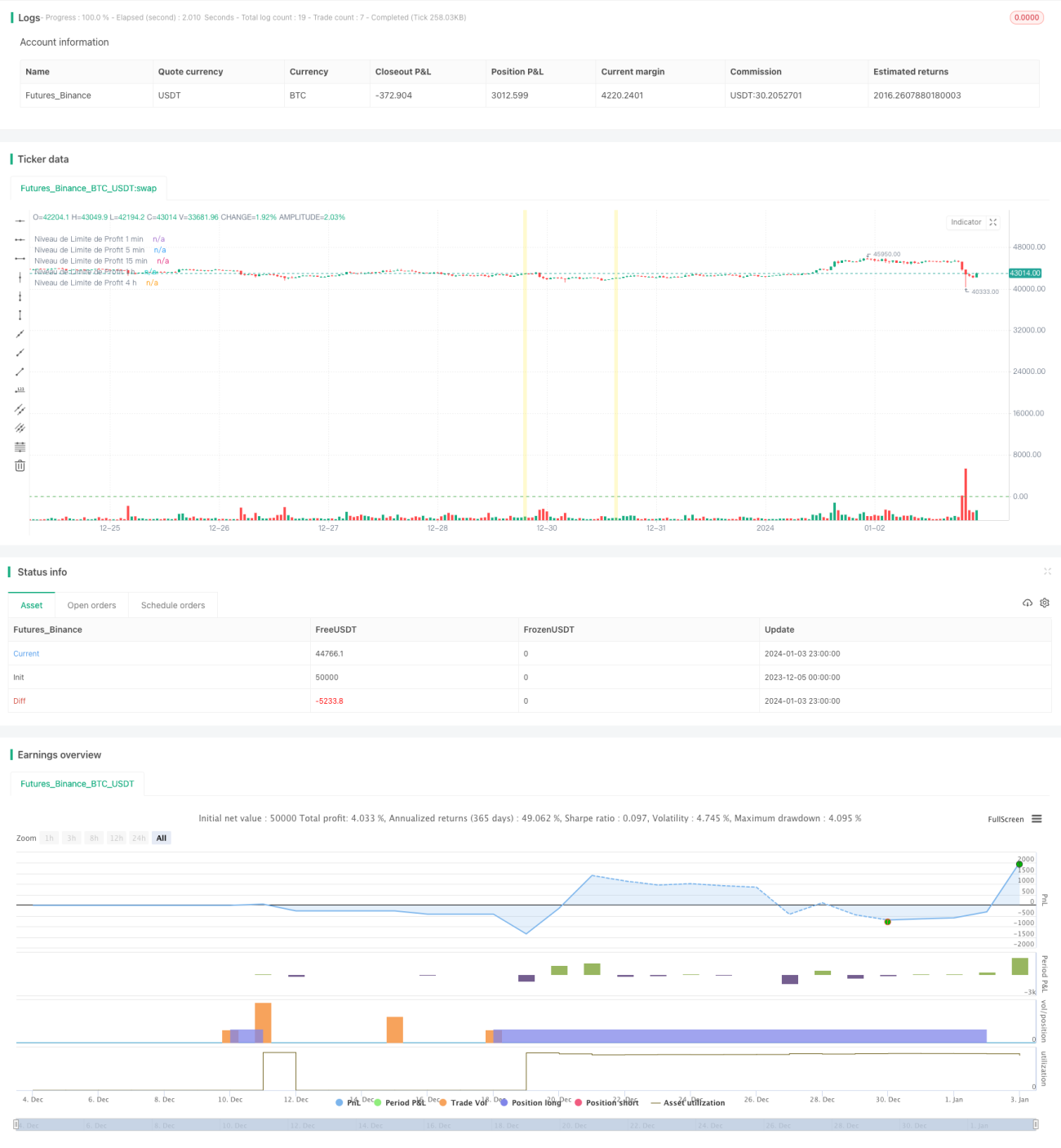

This strategy is a breakout strategy that combines multiple timeframes (1 min, 5 min, 15 min, 1 hour and 4 hours) to detect support and resistance areas on the chart.

Strategy Logic

The strategy uses Bollinger Bands and price channels to determine support and resistance zones. First, it calculates the Simple Moving Average (SMA) and Standard Deviation (STDEV) of closing prices for each timeframe to determine the upper and lower bands. It then detects “Breaker Blocks” which are determined based on price breakouts from support or resistance levels along with trading volume. A Breaker Block forms when price breaks out of a support or resistance level with high volume.

Once a Breaker Block is detected, a buy signal is generated if price breaks above the lower band, and a sell signal is generated if it breaks below the upper band. The strategy also plots price channels for each timeframe, representing support and resistance levels.

In addition, the strategy sets profit limit levels for each timeframe. This means price levels assigned to positions should be closed out at a profit. Stop-loss levels are also set to limit losses.

Advantage Analysis

- Utilizes multi timeframe analysis for more comprehensive market trend judgment

- Combining Breaker Blocks, Bollinger Bands channels and volume makes signals more reliable

- Setting profit and stop loss targets helps with risk control

Risk Analysis

- Poor Bollinger Bands parameter setting may cause false signals

- Breakouts could be short term market noise, leading to whipsaws

- Multi timeframe judgment increases strategy complexity

Risks can be further mitigated by optimizing Bollinger parameters, increasing holding period or setting stops.

Optimization Directions

This strategy can be optimized in several aspects:

-

Optimize Bollinger parameters for better reflection of true support and resistance

-

Add machine learning algorithms to judge breakout direction and momentum

-

Incorporate volatility indices to determine optimal entry and exit timing

-

Combine more indicators like MACD, KD to determine trends and energy

Summary

This strategy integrates multi-timeframe technical analysis, manages risks through breakout trading and profit stop loss management. It is a flexible and reliable breakout system. But parameter tuning and risk control according to actual markets need continual testing and optimization.

- 1