Triangular Moving Average Crossover Trading Strategy

Overview

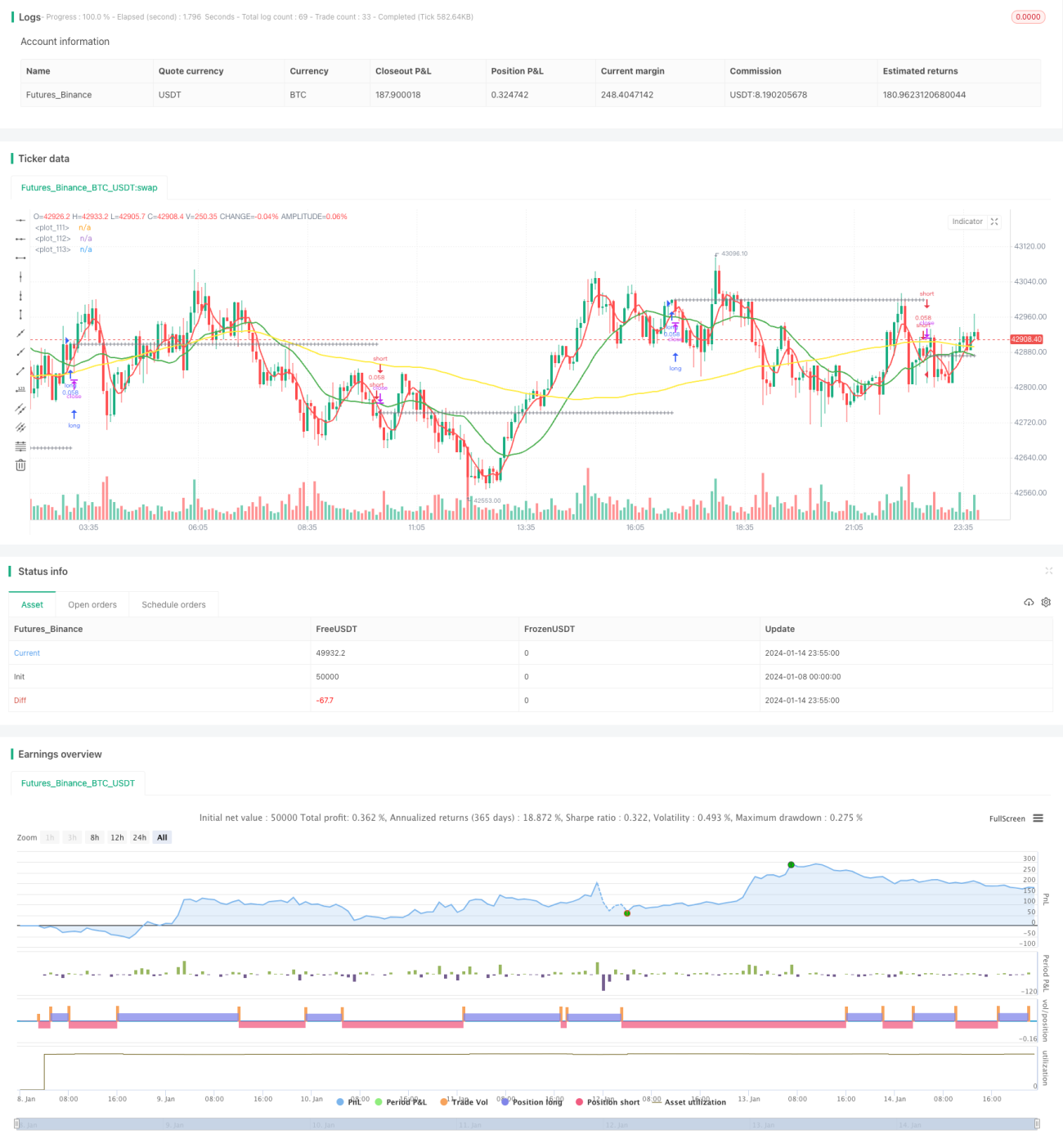

The Triangular Moving Average (TMA) Crossover trading strategy is a typical technical analysis strategy. It utilizes three moving average lines of different time lengths to capture trends and implement low-risk trading. When the short-term moving average crosses over the medium-term moving average upwards, and the medium-term moving average is above the long-term moving average, a buy signal is generated. When the short-term moving average crosses below the medium-term moving average downwards, and the medium-term moving average is below the long-term moving average, a sell signal is generated.

Strategy Logic

The TMA strategy mainly relies on three moving average lines to determine the trend direction. The short-term moving average responds sensitively to price changes; the medium-term moving average provides a clearer judgment of the trend; the long-term moving average filters out market noise and determines the long-term trend direction.

When the short-term moving average crosses over the medium-term moving average upwards, it indicates the price has started to break out upwards. At this time, if the medium-term moving average is above the long-term moving average, it means the current market is in an uptrend. Therefore, a buy signal is generated here.

On the contrary, when the short-term moving average crosses below the medium-term moving average downwards, it indicates the price has started to break out downwards. At this time, if the medium-term moving average is below the long-term moving average, it means the current market is in a downtrend. As a result, a sell signal is generated.

This strategy also sets stop-loss and take-profit lines. After entering a trade, stop-loss and take-profit prices will be calculated based on the percentage settings. If the price touches either line, the position will be closed.

Advantage Analysis

- Utilize three moving averages together to improve judgment accuracy

- Set stop-loss and take-profit to effectively control per trade risk

- Customizable moving average parameters suitable for different products

- Seven options for moving average types, diversified strategy types

Risk Analysis and Solutions

-

Wrong signals when three MAs are consolidating

Solution: Adjust MA parameters properly to avoid wrong signals

-

Over-aggressive stop-loss/take-profit percentage

Solution: Fine-tune percentages; cannot be too big or too small

-

Improper parameter settings leading to too many or too few trades

Solution: Test different parameter combinations to find optimum

Optimization Directions

The TMA strategy can be optimized from the following aspects:

-

Test different type and length combinations to find optimum

Test different MA length or type combinations for best results

-

Add other technical indicators as signal filters

Add indicators like KDJ, MACD etc. for multi-factor verification

-

Select parameters based on product characteristics

Shorten MA periods for volatile products; Lengthen periods for steady products

-

Utilize machine learning to find optimum parameters

Auto parameter sweeping to quickly locate optimum

Conclusion

The TMA Crossover strategy is an easy-to-use trend following strategy overall. It utilizes three MAs together to capture trends and sets stop-loss/take-profit to control risks, enabling stable profits. Further improvements can be achieved through parameter optimization and integrating extra technical indicators. In conclusion, this strategy suits investors seeking steady gains.

/*backtest

start: 2024-01-08 00:00:00

end: 2024-01-15 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Kozlod - 3 MA strategy with SL/PT", shorttitle="kozlod_3ma", overlay = true, default_qty_type = strategy.percent_of_equity, default_qty_value = 5)

// - 1