Dual Moving Average Crossover MACD Trend Following Strategy

Overview

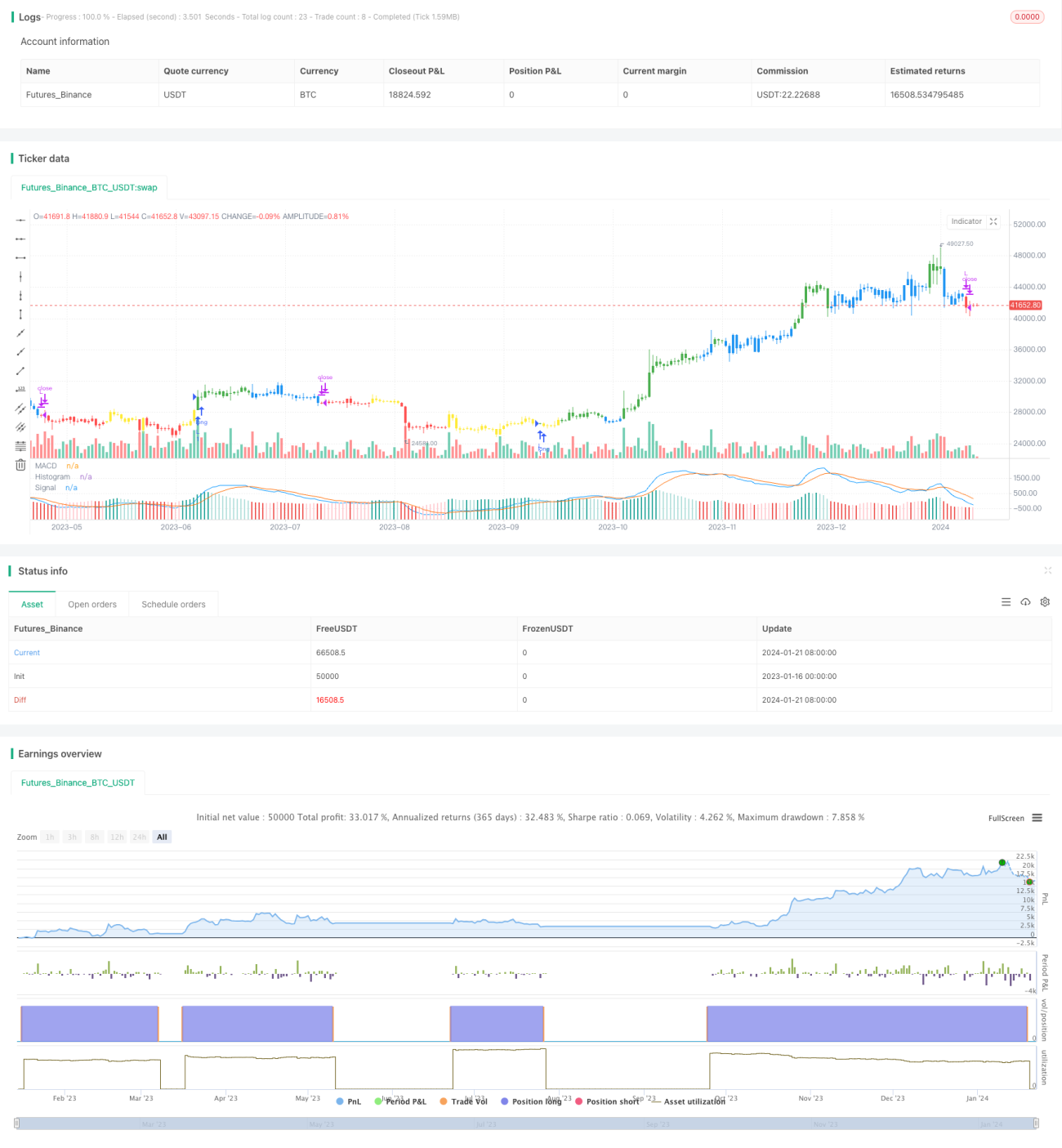

This strategy is an automated trading strategy based on the dual moving average crossover of the MACD technical indicator. It utilizes the signal line crossover of MACD to determine the trend direction for trend following.

Strategy Logic

The strategy first calculates the three lines of the MACD indicator: fast line, slow line and histogram. The fast line is a faster moving average over a shorter period while the slow line is a slower moving average over a longer period. The histogram is the difference between the fast and slow lines. When the fast line crosses above the slow line, it is a golden cross signal indicating a buy signal. When the fast line crosses below the slow line, it is a death cross signal indicating a sell signal.

The strategy utilizes this logic to go long on golden crosses and close position on death crosses; or go short on death crosses and close position on golden crosses to automatically follow the trend. Meanwhile, the strategy also judges if the absolute MACD line is positive or negative to avoid false signals and ensure truly capturing trend reversal points.

Advantages of the Strategy

- Utilizes dual moving average crossover to determine trend direction accurately and capture trend reversal

- MACD technical indicator reduces false signals and improves signal quality

- Flexibility to go long or short or only long/short

- Adjustable parameters cater to different market environments

Risks of the Strategy

- Dual moving average crossover has lagging effect, may miss partial profits at the beginning of reversals

- MACD indicator prone to false signals during market consolidation

- Parameters need proper adjustment to avoid overly sensitive or inert

Risk Mitigations:

- Combine with other indicators to filter signals

- Tune parameters to lower trading frequency

- Only adopt the strategy when trend is obvious

Enhancement Areas

The strategy can be enhanced from the following aspects:

-

Incorporate other indicators like KDJ, Bollinger Bands etc to confirm signals and filter false signals

-

Improve entry mechanism, e.g. add breakout filter to avoid premature or late entries

-

Optimize parameter settings, adjust fast and slow line periods based on different timeframes and market regimes

-

Add stop loss to control single trade loss

-

Expand to other products like forex, crypto currencies etc

Summary

The dual moving average crossover MACD trend following strategy utilizes MACD indicator to determine trend direction combined with signal line crossovers to effectively filter signals and capture trend reversals for automated trend following. The advantages lie in accurate trend judgment, flexible parameter tuning catering to market environments. Risk management is important to avoid false signals. Further optimizations with additional technical indicators and parameter tuning can improve strategy performance.

- 1