Momentum Moving Average Crossover Trading Strategy

Overview

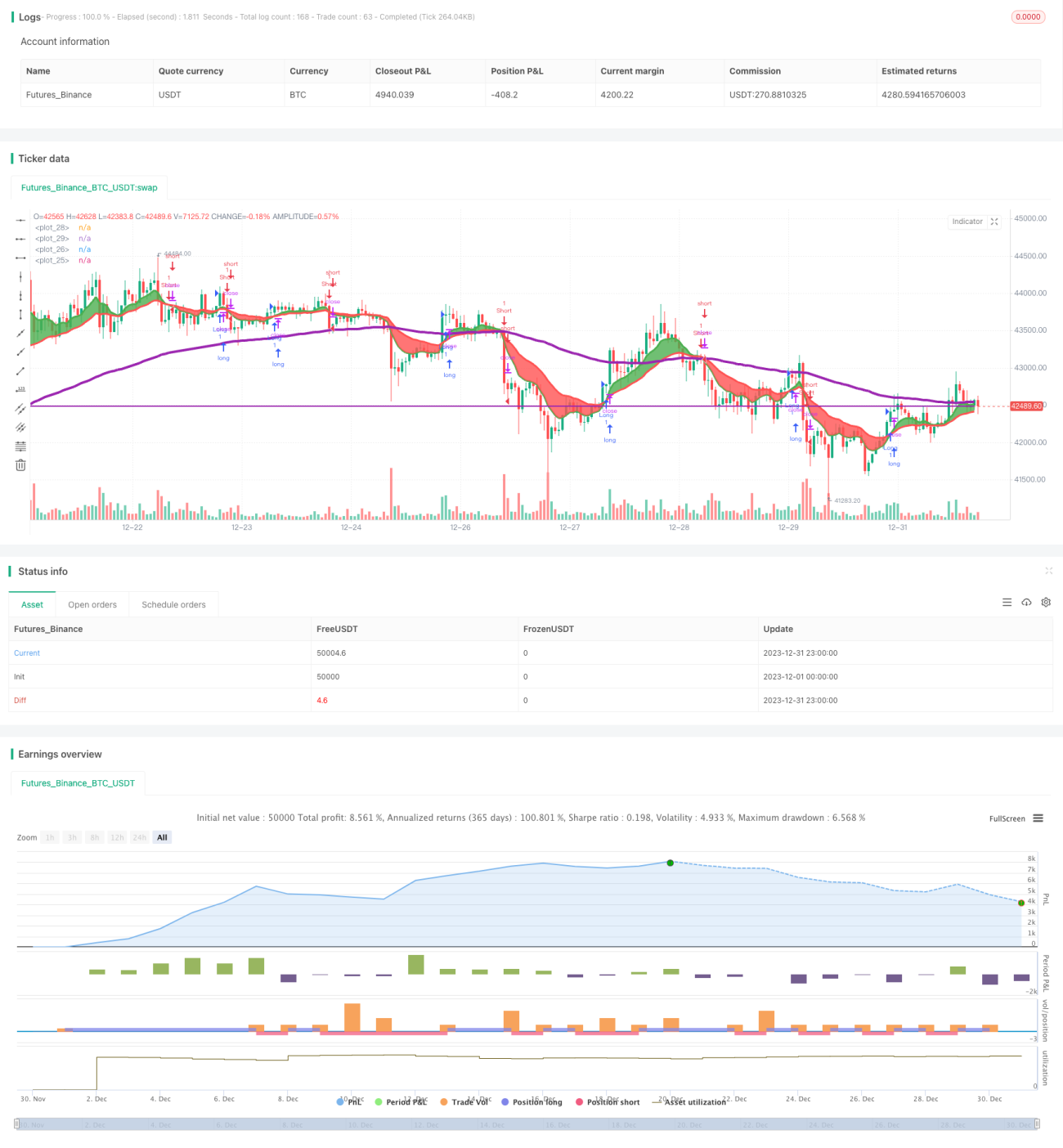

This strategy generates trading signals based on the crossover between fast and slow moving average lines to determine market trends and entry points. When the fast EMA crosses above the slow EMA, it is judged that the market is in an upward trend and a buy signal is generated. When the fast EMA crosses below the slow EMA, it is judged that the market is in a downward trend and a sell signal is generated. The strategy also sets stop loss and take profit prices to manage risks.

Strategy Logic

The strategy uses the crossover between a fast EMA (8-day) and slow EMA (21-day) to determine market trend. The specific logic is:

- Calculate the 8-day EMA and 21-day EMA

- When the 8-day EMA crosses above the 21-day EMA, it is determined that the market trend has reversed and an upward trend has started

- When the 8-day EMA crosses below the 21-day EMA, it is determined that the market trend has reversed and a downward trend has started

- During an uptrend, a buy signal is generated. During a downtrend, a sell signal is generated

- Set stop loss and take profit prices to manage risks for each position

The strategy combines momentum indicators and trend analysis to effectively capture market direction and reversal points. The fast and slow EMA crossover along with the moving average can filter out some noisy trading signals.

Advantage Analysis

The main advantages of this strategy are:

- Fast and slow EMA crosses can effectively determine market trends and trading signals

- Large optimization space for strategy parameters where EMA periods can be further tuned

- Noise signals can be filtered out effectively by incorporating momentum indicators

- Active risk control by configuring stop loss and take profit logic

In summary, the strategy combines trend and momentum indicators. Through parameter tuning, it can adapt to different market environments and is a relatively flexible short-term trading strategy.

Risk Analysis

There are also some risks with this strategy:

- In ranging markets, frequent EMA crossover signals may generate more false trades

- Gap risk is not handled effectively

- Long-term trend direction is not considered

To address these risks, some optimizations can be made:

- Add other filters like Bollinger Bands, KDJ to reduce false signals

- Incorporate higher timeframe indicators to determine long-term trend

- Optimize parameters like EMA lengths to adapt to different markets

- Manual intervention to avoid huge slippage losses from gaps

Optimization Directions

There is still large room for optimizing this strategy:

- Optimize EMA period parameters based on historical performance

- Add other technical indicators for signal filtering e.g. KDJ, MACD to improve accuracy

- Optimize stop loss and take profit settings to better fit market characteristics

- Use machine learning techniques for automated parameter optimization

These measures can greatly improve the stability, adaptability and profitability of the strategy.

Conclusion

In conclusion, this is a typical short-term trading strategy based on trend following and momentum indicator crosses. It combines EMA crossover logic and stop loss/take profit to quickly capture directional market opportunities. There is ample room for optimization by introducing other assist indicators and automated parameter tuning methods, which can make the strategy performance more stable and outstanding. It suits investors who have some market understanding and are willing to trade frequently.

- 1