Multiple Indicator Quantitative Trading Strategy

Overview

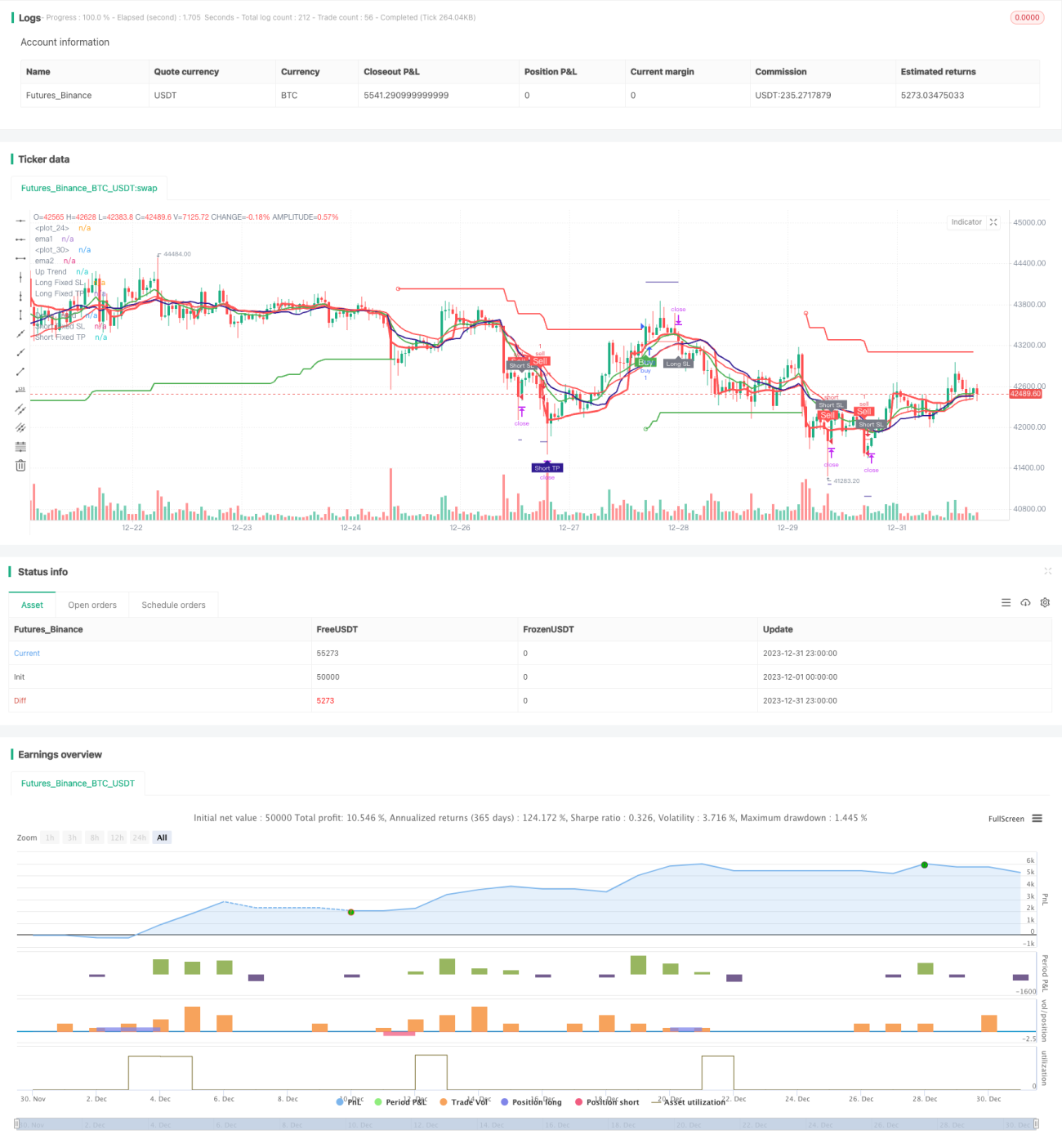

This strategy utilizes multiple technical indicators for quantitative trading. It mainly uses indicators including EMA crossovers, SuperTrend, RSI, MACD etc. to generate trading signals.

Strategy Logic

The core logic is based on the following aspects:

-

EMA Crossover: Compute fast EMA1 and slow EMA2. When EMA1 crossover above EMA2, generate buy signal. When EMA1 crossover below EMA2, generate sell signal.

-

VWMA: Compute VWMA. When close price crossover above VWMA, it is a buy signal. When close price crossover below VWMA, it is a sell signal.

-

SuperTrend: Compute the upper band and lower band based on ATR and multiplier parameter. Determine trend direction. Generate buy signals in uptrend and sell signals in downtrend.

-

RSI: Compute RSI indicator. When RSI is above overbought level, it is sell signal. When RSI is below oversold level, it is buy signal.

-

MACD: Compute MACD, signal line and histogram. When MACD line crossover above signal line, generate buy. When MACD line crossover below signal line, generate sell.

The strategy adopts "AND" logic to combine signals above. Only when multiple indicators emit buy/sell signal simultaneously, a final trading signal will be generated.

Advantages

This strategy combines multiple indicators to filter the market and avoid false signals. Main advantages:

-

Multiple indicators combination avoids errors of single indicator.

-

Combination of trend indicator and oscillator capture extra profit during trends.

-

Use of stop loss logic limits maximum loss per trade.

-

Martingale logic provides chance to break even after losses.

Risks

Main risks:

-

Too conservative indicator combination may miss some trading chance. Simplify the indicators combination when necessary.

-

Martingale logic may lead to significant losses. Set reasonable limitation to the number of additional entries.

-

Improper use of stop loss may lead to unnecessary stop out. Adopt adaptive stop loss mechanism.

-

Improper parameter tuning may lead too more false signals. Optimize parameters to find the best combination.

Optimization

The strategy can be further optimized in the following aspects:

-

Evaluate different combination of indicators, determine the weights.

-

Test different parameters for each indicator.

-

Add adaptive stop loss logic.

-

Add dynamic position sizing mechanism.

-

Leverage machine learning to optimize parameters and models.

Summary

In summary, this is a very practical quantitative trading strategy. It combines the strength of multiple classical technical indicators for market analysis. Further parameter tuning and model optimization can lead to better results.

- 1