RSI Indicator Based Stock Trading Pyramiding Strategy

Overview

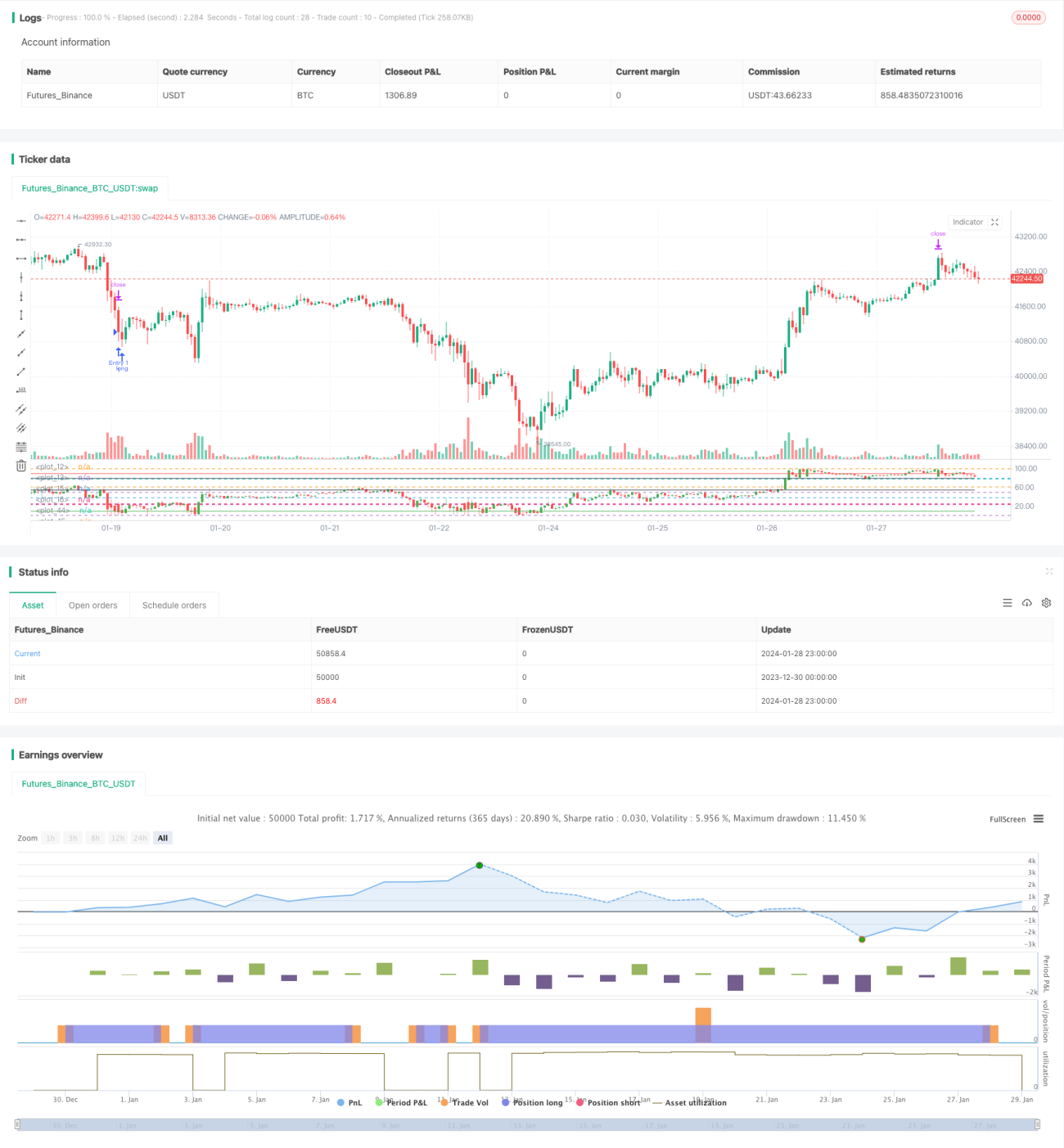

This article mainly introduces a stock trading pyramiding strategy designed based on the Relative Strength Index (RSI) indicator. The strategy uses the RSI indicator to determine overbought and oversold areas of stocks and implements profit making through pyramiding principles.

Strategy Principle

- Use the RSI indicator to judge whether the stock has entered the overbought or oversold area. RSI below 25 is oversold, and above 80 is overbought.

- When the RSI enters the oversold area, start going long. When the RSI enters the overbought area, start going short.

- Adopt the pyramiding method, with up to 7 additional purchases. Set take profit and stop loss points after each additional purchase.

Advantage Analysis

- Using the RSI indicator to determine the overbought and oversold areas can capture larger price reversal opportunities.

- The pyramiding method can obtain relatively better returns when the market moves correctly.

- Setting take profit and stop loss after each additional purchase can control risks.

Risk Analysis

- The effect of RSI indicator to determine overbought and oversold areas is unstable, and wrong signals may occur.

- The number of additional purchases needs to be set reasonably, too many additional purchases will increase risks.

- The setting of stop loss points needs to consider volatility, cannot be set too small.

Optimization Directions

- Consider combining other indicators to filter RSI signals and improve the accuracy of determining overbought and oversold statuses. Such as KDJ, BOLL and other indicators.

- Can set floating stop loss to track price. Adjust dynamically according to volatility and risk control requirements.

- Consider using adaptive parameters based on market conditions (bull market, bear market, etc.).

Summary

This strategy combines the RSI indicator with the pyramiding strategy. While judging the overbought and oversold statuses, it can obtain more returns through additional purchases. Although the accuracy of RSI judgment needs to be improved, through reasonable parameter optimization and combination with other indicators, it can form an effective trading strategy. This strategy has some universality and is a relatively simple and straightforward quantitative trading method.

- 1