Scalping Dips in Bull Market Strategy

Overview

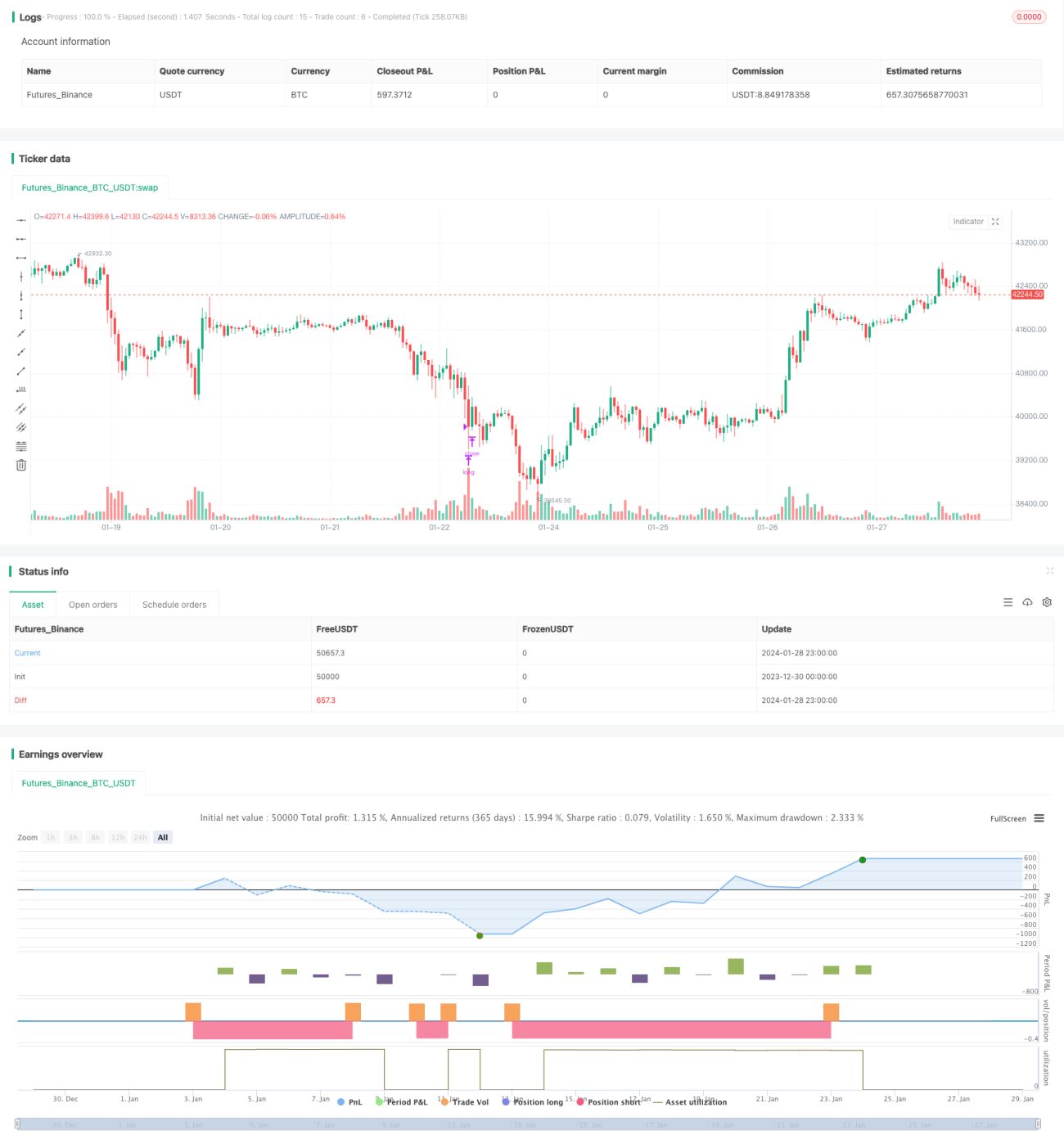

The Scalping Dips in Bull Market strategy is a trend-following strategy. It buys the dip during bull markets, sets a wide stop loss to lock in profits when exiting positions. This strategy is suitable for bull markets and can yield excess returns.

Strategy Logic

This strategy first calculates the percentage price change over a lookback period. When the price drops by more than the preset callback percentage, a buy signal is triggered. At the same time, the moving average line needs to be above the close price as a confirmation of the uptrend.

After entering a position, stop loss and take profit prices are set. The stop loss percentage is large to ensure sufficient funds; the take profit percentage is small for fast profit taking. When the stop loss or take profit is triggered, the position will be closed.

Advantage Analysis

The advantages of this strategy are:

- Aligns with the trend following methodology to obtain excess returns

- Reasonable callback percentage and trend criteria ensure accuracy

- The stop loss design fully considers capital safety

- Quick profit taking by take profit settings and drawdown control

Risk Analysis

There are also some risks with this strategy:

- Overly deep retracement or trend reversal may lead to losses

- Drawdown risk from the wide stop loss

- Difficulty satisfying stop loss/profit conditions during range-bound markets

Counter measures: Strictly control position sizing, adjust stop loss percentage, properly reduce take profit exit ratio to mitigate risks.

Optimization Directions

The strategy can be optimized in the following aspects:

- Dynamically adjust the callback percentage to optimize entry opportunities

- Add more indicators to improve decision accuracy

- Incorporate volatility measures to dynamically tune stop loss/profit ratios

- Optimize position sizing to better control risks

Conclusion

The Scalping Dips in Bull Market strategy locks in excess returns using a wide stop loss. It capitalizes on buying callback dips in bull market trends for profit opportunities. Fine tuning parameters and risk controls can yield good steady returns.

- 1