Strategy of Indicators Combination Breakthrough Trend Tracking

Overview

The strategy is named "Strategy of Indicators Combination Breakthrough Trend Tracking". It combines various indicators to identify market trend directions and carry out trend tracking operations. The main components include:

- Using Wave Trend indicator to judge the main trend of the market

- Filtering out some false signals with RSI and MFI indicators

- Determining specific operational directions with EMA indicator

- Entering the market with breakthrough tracking method to ensure following the trend

Strategy Principle

The strategy mainly judges the direction and strength of the major trend, and sets bidirectional trading of long and short. The specific operating principles are as follows:

Long signal:

- Price is above 200-day EMA, indicating a bull market

- Price pulls back to around 50-day EMA forming support

- Wave Trend reverses to upward trend and a buy signal appears

- Both RSI and MFI show overbought

- 3 consecutive K-lines break through 50-day EMA successively, indicating a breakthrough upwards

Short signal:

Opposite of long signal

Profit taking and stop loss:

Two options provided: lowest price/highest price stop loss, ATR stop loss

Advantage Analysis

The strategy has the following advantages:

- Integrates multiple indicators to determine the major trend and avoid false breakouts

- Adopts EMA to determine operational direction, easy to follow trends

- Trailing stop loss method achieves sustained profits

- Capable of going both long and short, following the market in either direction

Risk Analysis

The strategy also has some risks:

- Probability of wrong signals from the indicators

- Stop loss point set too small, increasing stop loss risk

- High trading frequency leads to hidden loss from trading fees

To reduce the above risks, optimization can be done in the following aspects:

- Adjust indicator parameters to filter wrong signals

- Appropriately loosen the stop loss point

- Optimize indicator parameters to reduce trading frequency

Optimization Directions

From the code level, the main optimizable directions of this strategy include:

- Adjusting parameters of Wave Trend, RSI and MFI to find the best parameter combination

- Testing the performance of different EMA cycle parameters

- Adjusting risk-reward ratio factors of profit taking and stop loss to obtain optimal configuration

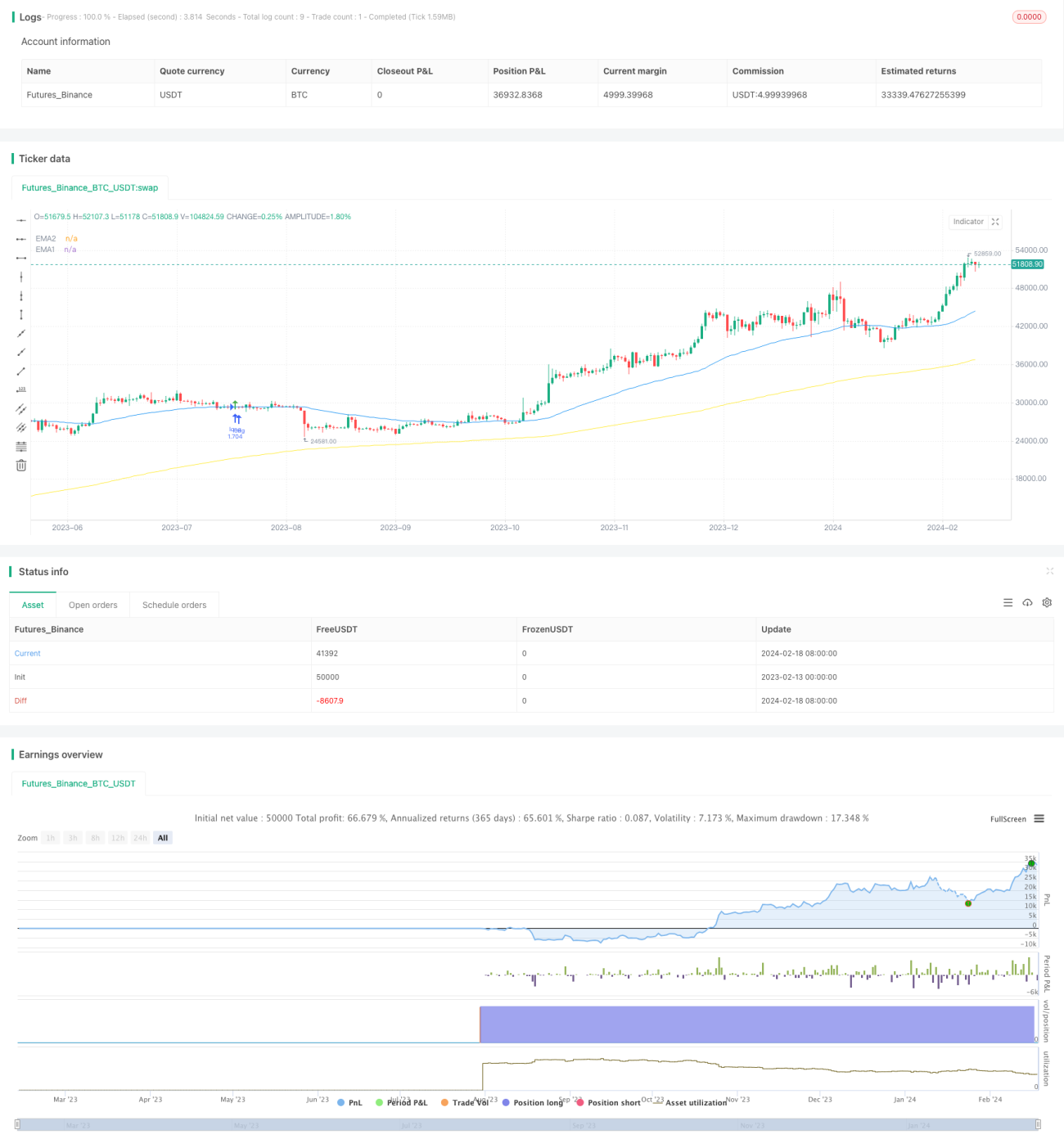

Through parameter adjustment and testing, the strategy can maximize returns while reducing drawdowns and risks.

Conclusion

The strategy integrates multiple indicators to determine the major trend direction, uses EMA indicator as specific operation signal, and uses trailing stop loss to lock in profits. Through parameter optimization, relatively good steady profits can be obtained. But the certain system risks should also be noted, the effectiveness of indicators and changes in market environment need to be continuously monitored.

- 1