Trading Psychology Balancing Strategy

Overview

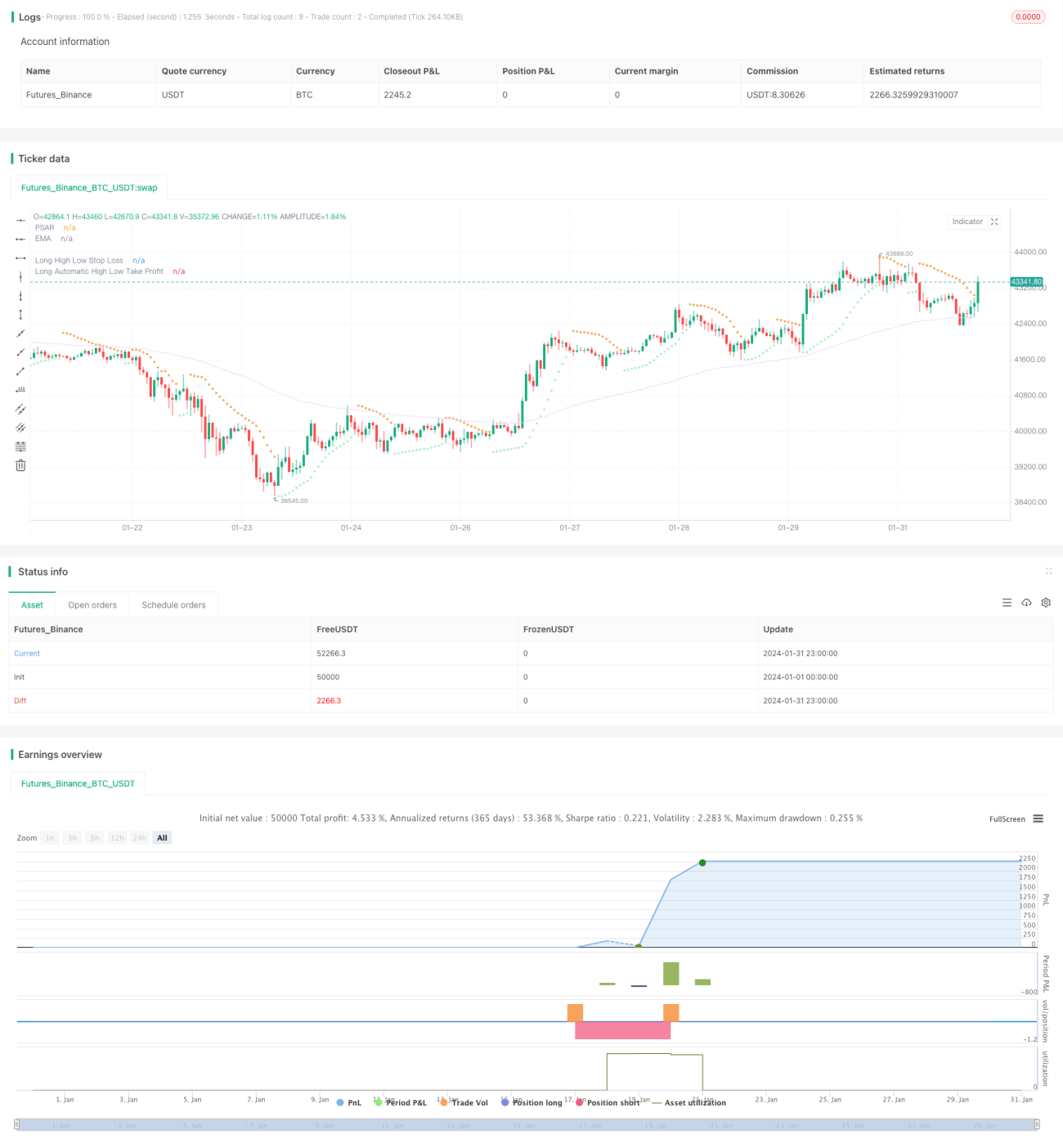

The goal of this strategy is to balance the psychology and performance of traders through adjusting various parameters, in order to obtain more steady returns. It uses indicators like moving averages, Bollinger Bands and Keltner Channels to determine market trends and volatility, together with the PSAR indicator to identify reversal signals. The TTM Squeeze indicator is leveraged to gauge momentum. Trading signals are generated through the combination of these indicators. In the meantime, risks are managed via the high-low stop loss and risk-reward take profit methods.

Strategy Logic

The core logic of this strategy is as follows:

-

Judge trends: the EMA moving average is used to determine the direction of price trends. Prices above EMA signify uptrends while prices below EMA indicate downtrends.

-

Identify reversals: the PSAR indicator spots price reversal points. PSAR dots appearing above prices signal longs while dots emerging below prices call for shorts.

-

Gauge momentum: the TTM Squeeze indicator measures market volatility and momentum. It compares Bollinger Bands and Keltner Channels to quantify volatility squeezes and surges. Squeeze implies extremely low volatility while a squeeze release signals an impending large directional price move.

-

Generate trading signals: long signals are triggered when prices crossover above the EMA line and PSAR dots, accompanied by a TTM Squeeze release. Short signals occur when prices crossover below the EMA and PSAR, together with a TTM Squeeze triggering.

-

Stop loss method: the high-low stop loss bases stop levels on recent high/low prices multiplied by a set factor.

-

Take profit method: the risk-reward take profit automatically calculates profit targets based on the stop loss distance from current prices multiplied by a preset risk-reward ratio.

The various parameters allow traders to balance psychology by controlling trade frequency, position sizing, stop loss levels and take profit points.

Advantage Analysis

The main edges of this strategy include:

-

Higher signal accuracy from multiple indicator consensus

-

Mainly reversal-focused, reduces likelihood of false breakout fades

-

TTM Squeeze gauges consolidations to avoid ineffective trades

-

Simple and adjustable high-low stop loss

-

Risk-reward take profit quantifies profit ratio for easy tuning

-

Flexible parameters to match personal risk preferences

Risk Analysis

The risks of the strategy consist of:

-

Increased chance of missing entry signals from multiple indicators

-

Underperformance in persistent trending markets

-

Occasional stop loss breaches beyond expectations

-

Potential invalidation of risk-reward exits by price whipsaws

-

Inappropriate parameter tuning may lead to losses or over-stopping out

Optimization Directions

Possible improvement areas cover:

-

Add or adjust indicator weights for higher signal accuracy

-

Optimize reversal and trend parameters for better profit capture

-

Refine high-low stop loss levels for maximized effectiveness

-

Test different risk-reward ratios for optimum results

-

Adjust position sizing to minimize single-trade loss impacts

Summary

In summary, through indicator combos and tunable settings, this strategy is capable of balancing trading psychology and securing steady positive results. Despite some remaining upside, it has already demonstrated practical applicability. Further live market feedback and calibration will likely enhance it into an effective tool for managing emotions and achieving long-term stable profits.

- 1