Spaced Out Trading Strategy

Overview

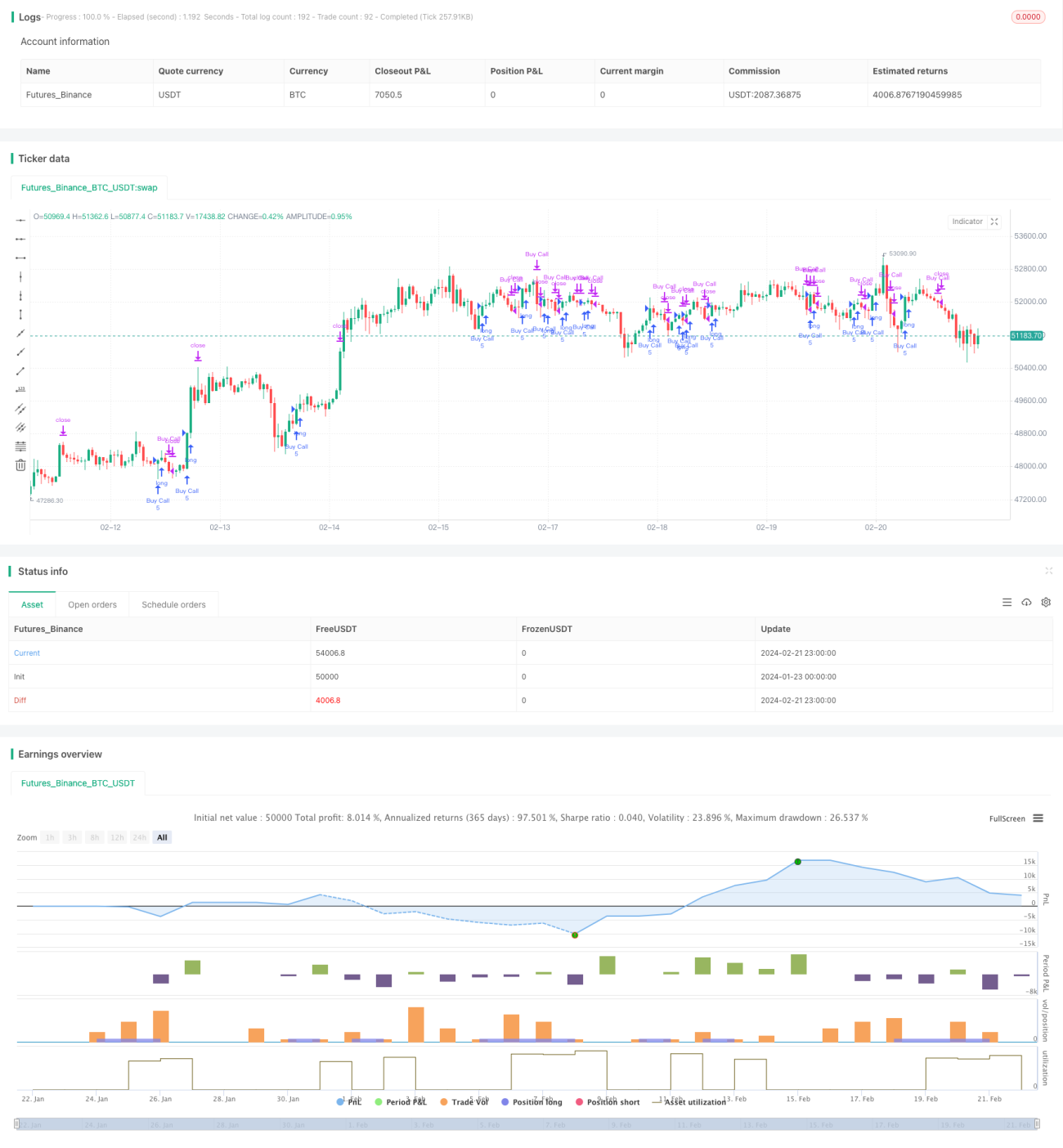

The Spaced Out Trading Strategy is a trend-following strategy based on moving averages. It utilizes a 30-day exponential moving average (EMA) to identify price trends and enters trades when prices break out above/below the EMA. It exits trades when prices fall back below/above the EMA line. This strategy works well with 30-min to daily timeframes.

Strategy Logic

The core logic relies on the relationship between price and the 30-day EMA to generate entry and exit signals. Specifically:

- Calculate the 30-day EMA as the benchmark for the trend.

- Enter long trades when prices break out above the EMA.

- Exit trades when prices fall back below the EMA.

By capturing trend breakouts, it aims to capitalize on momentum moves and trend-following opportunities.

Advantage Analysis

The main advantages of this strategy include:

- Simple logic that is easy to understand and implement at low costs.

- Smoothens price fluctuations using EMA and focuses on the main trend.

- The 30-day EMA provides a medium-term lens to capture both swing and long-term trends.

- Customizable parameters adaptable across products and market regimes.

Risks and Mitigations

Some of the key risks are:

- Whipsaw risk from prices reversing after temporary breakout of EMAs. Can use longer EMA periods.

- Risk of accumulated losses from sustained trend reversal. Can set stop-loss limits.

- Suboptimal EMA period risk. Can ensemble adaptive EMA or multiple EMAs.

Enhancement Opportunities

Some ways the strategy can be upgraded:

- Add adaptive EMAs tailored to market volatility and asset characteristics.

- Build multi-EMA systems combining short and long-term EMAs.

- Incorporate stop-loss mechanisms e.g. moving average stop, range bound stop.

- Combine with other indicators e.g. momentum, volatility for signal filtering.

- Parameter optimization via machine learning algorithms.

Summary

The Spaced Out Trading Strategy aims to capture trends by trading price breakouts of EMA levels. It is a simple and practical quantitative strategy. With customizable loss limits and judicious optimizations, it can be a stable strategy providing sustainable returns across medium to long-term holding periods.

- 1