ZLSMA-Enhanced Chandelier Exit Strategy with Volume Spike Detection

Overview

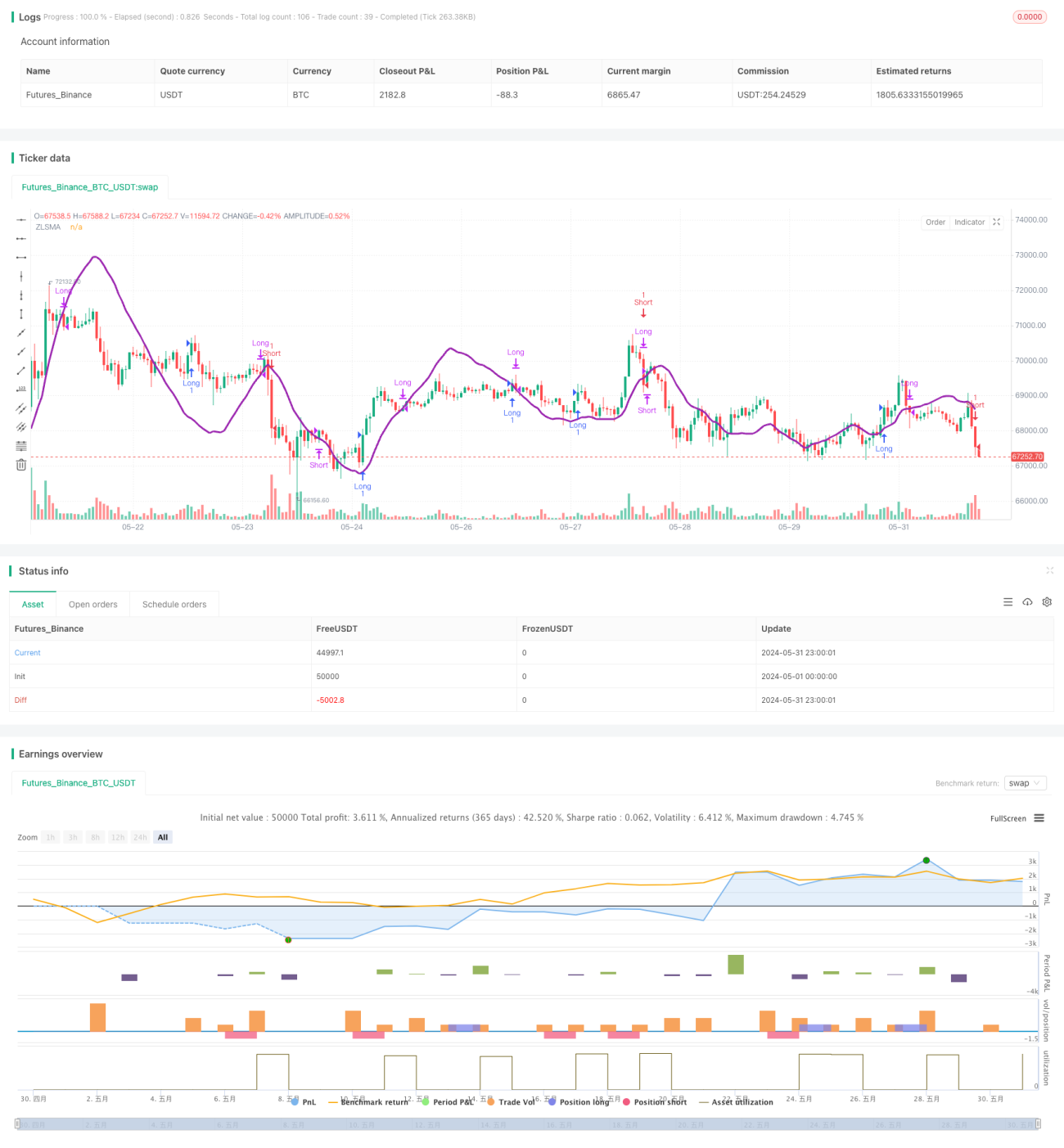

This strategy combines the Chandelier Exit rule, the Zero-Lag Smoothed Moving Average (ZLSMA), and the Relative Volume (RVOL) spike detection to form a complete trading system. The Chandelier Exit rule dynamically adjusts the stop-loss position based on the Average True Range (ATR), allowing it to better adapt to market changes. The ZLSMA accurately captures price trends, providing direction guidance for trading. The RVOL spike detection helps the strategy avoid low-volatility consolidation markets, improving trading quality.

Strategy Principle

- Calculate ATR and determine long and short stop-loss positions based on ATR and the highest/lowest prices.

- Calculate ZLSMA as a basis for judging trend direction.

- Calculate RVOL and determine whether a volume spike occurs by comparing RVOL with a set threshold.

- Long entry: When the current close crosses above the ZLSMA and RVOL is greater than the threshold, open a long position with the stop-loss set at the recent low.

- Short entry: When the current close crosses below the ZLSMA and RVOL is greater than the threshold, open a short position with the stop-loss set at the recent high.

- Long exit: When the current close crosses below the ZLSMA, close the long position.

- Short exit: When the current close crosses above the ZLSMA, close the short position.

Strategy Advantages

- The Chandelier Exit rule dynamically adjusts the stop-loss position, reducing the risk associated with fixed stop-losses.

- The ZLSMA responds quickly to price changes, providing reliable trend judgment for trading.

- The RVOL spike detection helps the strategy avoid low-volatility consolidation markets, improving trading quality.

- The strategy logic is clear and easy to understand and implement.

Strategy Risks

- In markets with unclear trends or frequent fluctuations, this strategy may result in a high number of trades, increasing transaction costs.

- The performance of the strategy is greatly influenced by parameter settings (such as ATR period, ZLSMA period, RVOL threshold, etc.), and inappropriate parameters may lead to poor strategy performance.

- The strategy does not consider position management and risk control, which need to be incorporated when applying the strategy in practice.

Strategy Optimization Direction

- Introduce trend confirmation indicators, such as moving average systems or momentum indicators, to further improve the accuracy of trend judgment.

- Optimize the logic of RVOL spike detection, such as considering multiple consecutive RVOL spikes before trading, to further improve signal quality.

- Add profit-taking logic to the exit conditions, such as closing a position if a certain profit target is reached, to lock in profits.

- Optimize strategy parameters based on market characteristics and trading instruments to find the best parameter combination.

- Combine position management and risk control principles to improve the strategy's robustness and reliability.

Summary

The ZLSMA-Enhanced Chandelier Exit Strategy with Volume Spike Detection is a trend-following strategy that controls trading risk while capturing trend opportunities through dynamic stop-loss, trend judgment, and volume spike detection. The strategy logic is clear and easy to understand and implement, but it still needs to be optimized and improved based on specific market characteristics and trading instruments when applied in practice. By introducing more signal confirmation indicators, optimizing exit conditions, reasonably setting parameters, and implementing strict position management and risk control, this strategy has the potential to become a robust and efficient trading tool.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Chandelier Exit Strategy with ZLSMA and Volume Spike Detection", shorttitle="CES with ZLSMA and Volume", overlay=true, process_orders_on_close=true, calc_on_every_tick=false)

// Chandelier Exit Inputs

lengthAtr = input.int(title='ATR Period', defval=1)- 1