Adaptive Trend Following Strategy Combining AlphaTrend and KAMA with Risk Management

Overview

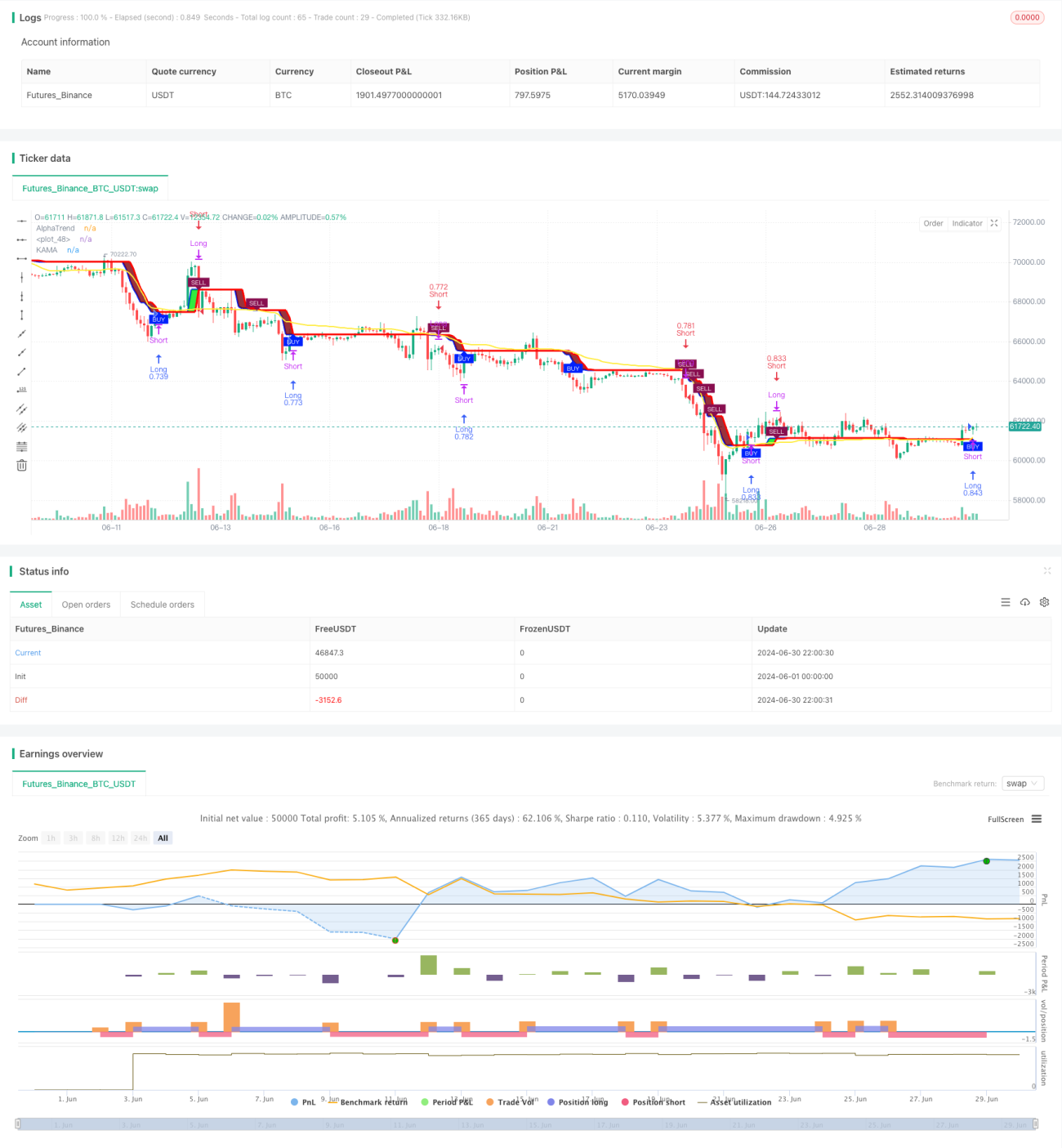

This strategy is a trend-following system that combines the AlphaTrend indicator with the Kaufman Adaptive Moving Average (KAMA), while also incorporating risk management features. The strategy aims to capture market trends while managing risk through partial profit-taking. At its core, the strategy uses the AlphaTrend indicator to identify overall trend direction, while KAMA is employed to generate more precise entry and exit signals. Additionally, the strategy includes a percentage-based partial profit-taking mechanism to lock in profits when specific targets are reached.

Strategy Principles

-

AlphaTrend Indicator Calculation:

- Uses Average True Range (ATR) to calculate upper and lower channels.

- Determines trend direction based on Money Flow Index (MFI) or Relative Strength Index (RSI) values.

-

KAMA Calculation:

- Employs Kaufman Adaptive Moving Average, dynamically adjusting its sensitivity based on market volatility.

-

Trade Signal Generation:

- Buy signal: Triggered when KAMA crosses above the AlphaTrend line.

- Sell signal: Triggered when KAMA crosses below the AlphaTrend line.

-

Risk Management:

- Implements partial profit-taking mechanism, closing half the position when a preset profit percentage is reached.

-

Position Management:

- Uses account equity percentage for position sizing, ensuring flexibility in capital utilization.

Strategy Advantages

-

Strong Trend Adaptability: Combination of AlphaTrend and KAMA allows for better adaptation to various market environments.

-

High Signal Reliability: Multiple condition confirmations increase the reliability of trading signals.

-

Comprehensive Risk Management: Partial profit-taking mechanism helps secure profits in volatile markets.

-

Flexible Position Management: Equity-based position sizing adapts to different capital scales.

-

Excellent Visualization: The strategy provides a clear graphical interface for easy analysis and monitoring.

Strategy Risks

-

False Breakout Risk: May generate frequent false signals in choppy markets.

-

Lag: As a trend-following strategy, it may react slowly to trend reversals.

-

Parameter Sensitivity: Strategy performance may be sensitive to parameter settings.

-

Drawdown Risk: Partial profit-taking might result in missing out on big moves in strongly trending markets.

-

Market Adaptability: The strategy may underperform in certain specific market conditions.

Strategy Optimization Directions

-

Dynamic Parameter Adjustment:

- Implement adaptive adjustment of AlphaTrend and KAMA parameters to suit different market environments.

- Reason: Improve strategy adaptability across different market cycles.

-

Multi-Timeframe Analysis:

- Introduce multi-timeframe confirmation mechanism to enhance signal reliability.

- Reason: Reduce false breakouts and improve trade success rate.

-

Volatility Filtering:

- Add an ATR-based volatility filter to reduce trading in low volatility environments.

- Reason: Avoid overtrading in ranging markets.

-

Intelligent Stop-Loss:

- Implement dynamic ATR-based stop-loss for more flexible risk management.

- Reason: Better adapt to market volatility and protect profits.

-

Market State Classification:

- Introduce a market state classification mechanism to adopt different trading strategies in various market states.

- Reason: Enhance strategy performance across various market environments.

Conclusion

The Adaptive Trend Following Strategy Combining AlphaTrend and KAMA with Risk Management is a comprehensive and powerful trading system. It achieves precise market trend capture by combining the strengths of the AlphaTrend indicator and KAMA. The strategy's risk management mechanisms, especially the partial profit-taking feature, provide traders with an effective tool for protecting profits in volatile markets. While inherent risks exist, such as false breakouts and parameter sensitivity, continuous optimization and adjustment give this strategy the potential to become a reliable trading system. Future optimization directions, such as dynamic parameter adjustment and multi-timeframe analysis, will further enhance the strategy's adaptability and robustness. Overall, this is a strategy worth in-depth study and practice, particularly suitable for traders seeking to balance trend following with risk management.

/*backtest

start: 2024-06-01 00:00:00

end: 2024-06-30 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('AlphaTrend with KAMA and Risk Management', shorttitle='AT+KAMA+RM', overlay=true, format=format.price, precision=2, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// AlphaTrend Inputs- 1