Dynamic Position Dual Moving Average Crossover Strategy

Overview

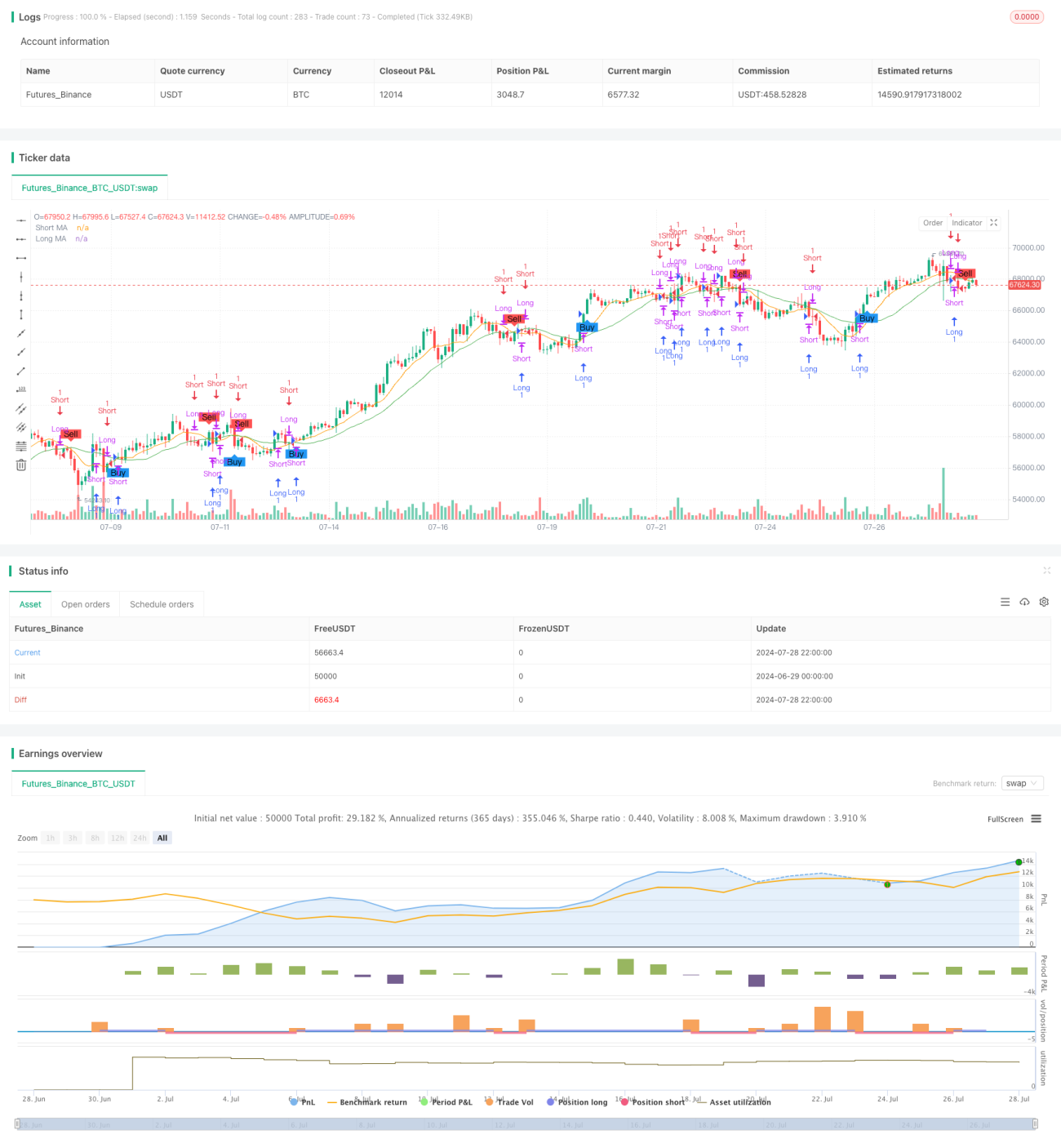

The Dynamic Position Dual Moving Average Crossover Strategy is a quantitative trading approach that utilizes the crossover signals of two Simple Moving Averages (SMAs) with different periods to execute trades. This strategy leverages the crossover of short-term and long-term moving averages to determine market trends and dynamically adjusts position direction based on crossover signals and the relationship between price and the long-term average. The strategy operates on a daily timeframe and allows for flexibility in sensitivity and reaction speed through adjustable moving average parameters.

Strategy Principle

- Moving Average Calculation: The strategy employs two SMAs - a 9-day and a 21-day.

- Trade Signal Generation:

- Buy Signal: Short-term MA (9-day SMA) crosses above the long-term MA (21-day SMA)

- Sell Signal: Short-term MA crosses below the long-term MA

- Position Management:

- Opening Positions: Enter long on buy signals; enter short on sell signals

- Closing and Reversing Positions:

a) When holding a long position, close and go short if the opening price is below the long-term MA or a sell signal occurs

b) When holding a short position, close and go long if the opening price is above the long-term MA or a buy signal occurs

- Risk Control: The strategy does not use fixed stop-losses but controls risk through dynamic position adjustment

Strategy Advantages

- Trend Following: Captures market trends using MA crossovers, potentially yielding significant returns in strong trends

- Dynamic Positioning: Flexibly adjusts positions based on price-MA relationship, enhancing adaptability

- Simplicity: Clear and easy-to-understand logic, facilitating implementation

- Adjustable Parameters: MA periods can be tuned to suit different market environments and instruments

- All-Weather Trading: Operates continuously under various market conditions

- Automated Execution: Can be fully automated, reducing emotional interference

- Risk Management: Avoids slippage losses associated with fixed stop-losses through dynamic position adjustment

Strategy Risks

- Unfavorable in Choppy Markets: May incur losses due to frequent trading in sideways or volatile markets

- Lagging Nature: Moving averages are inherently lagging indicators, potentially missing initial phases of sharp moves

- False Breakout Risk: Short-term price fluctuations may trigger false MA crossovers, leading to erroneous signals

- Lack of Stop-Loss: Absence of fixed stop-losses may result in significant losses in extreme market conditions

- Overtrading: Frequent position adjustments can lead to high transaction costs

- Parameter Sensitivity: Strategy performance is highly dependent on MA period selection

- Single Indicator Limitation: Relying solely on MA crossovers may overlook other crucial market information

Optimization Directions

- Incorporate Additional Indicators: Combine with RSI, MACD, etc., to improve signal reliability

- Optimize Entry Timing: Add volume and volatility filters to reduce false breakouts

- Implement Stop-Loss Mechanisms: Introduce fixed or trailing stop-losses to control per-trade risk

- Adjust Position Sizing: Dynamically size positions based on market volatility for better capital management

- Add Market State Identification: Distinguish between trending and ranging markets, applying different strategies accordingly

- Optimize Parameter Selection: Use historical data backtesting to find optimal MA period combinations

- Introduce Trend Strength Filters: Implement indicators like ADX to trade only in strong trend conditions

- Develop Adaptive Parameters: Automatically adjust MA periods based on market volatility for improved adaptability

Conclusion

The Dynamic Position Dual Moving Average Crossover Strategy is a classic and practical quantitative trading method that captures market trends by leveraging MA crossover signals and dynamically adjusting positions. This strategy is simple to understand, fully automatable, and demonstrates good trend-following capabilities with flexibility. However, it also faces potential risks such as poor performance in choppy markets and lagging signals. By incorporating additional technical indicators, optimizing parameter selection, and implementing stop-loss mechanisms, the strategy's stability and profitability can be further enhanced. Traders employing this strategy should adjust parameters and manage risks according to specific trading instruments and market environments to achieve long-term, stable trading results.

/*backtest

start: 2024-06-29 00:00:00

end: 2024-07-29 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="MA Cross Backtest", overlay=true, default_qty_type=strategy.cash, default_qty_value=10)

// Parâmetros das Médias Móveis- 1