1

Follow

1802

Followers

Overview

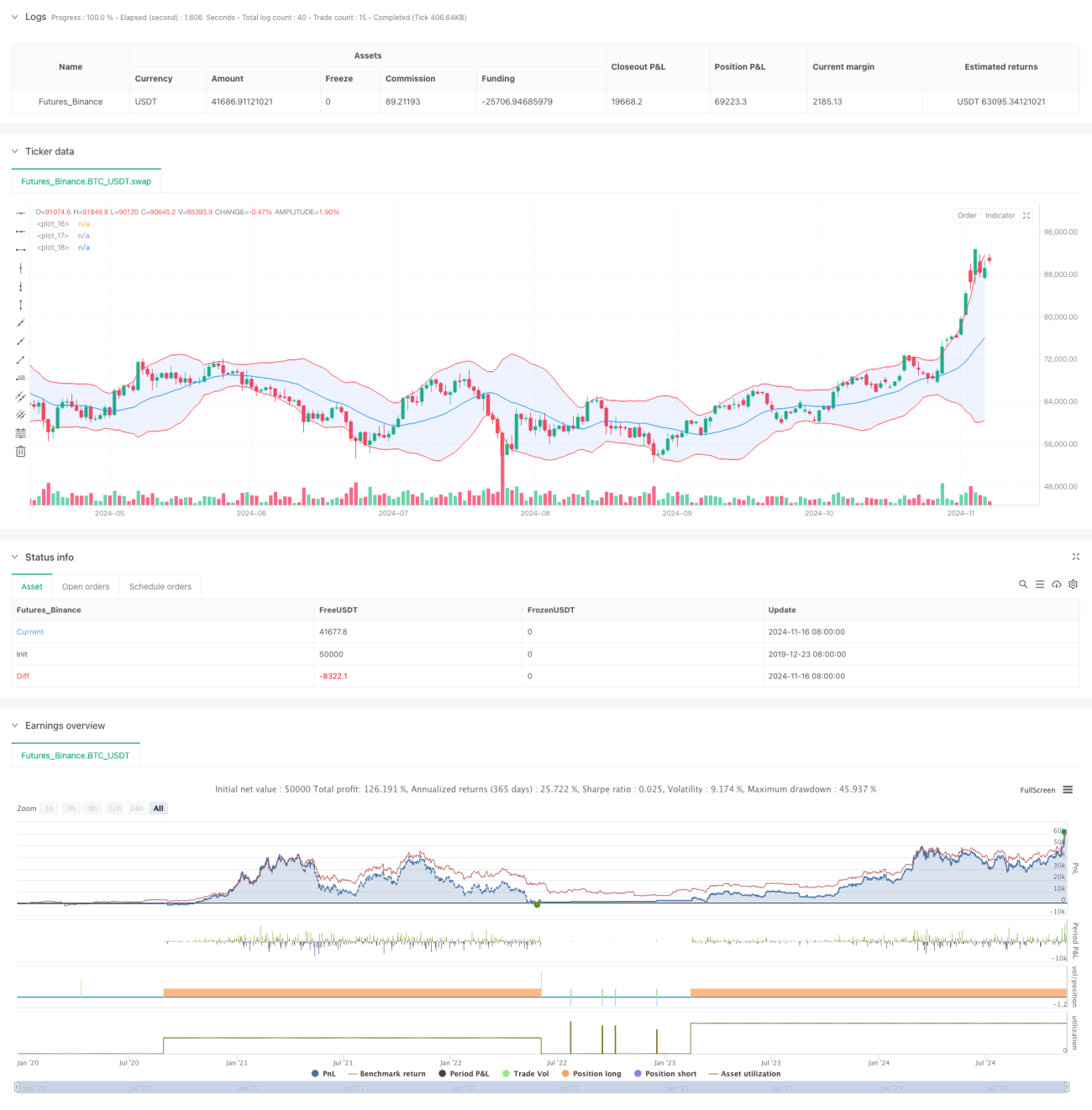

This strategy is a mean reversion trading system based on Bollinger Bands, optimized with trend filters and dynamic stop-loss mechanisms. It applies statistical principles to trade price deviations from the mean while using technical indicators to improve win rates and manage risks.

Strategy Principles

The strategy is built on several key components:

- Uses 20-period Bollinger Bands as the primary signal source with 2 standard deviation bandwidth

- Incorporates 50-period EMA as a trend filter to ensure trade direction aligns with medium-term trends

- Employs 14-period ATR for dynamic stop-loss and profit targets to improve risk-reward ratios

- Enters long when price touches lower band and is above EMA, shorts when price touches upper band and is below EMA

- Sets profit target at 2x ATR and stop-loss at 1x ATR

Strategy Advantages

- Combines benefits of mean reversion and trend following for improved reliability

- Dynamic stop-loss and profit targets adapt to market volatility

- Clear entry and exit rules minimize subjective judgment

- Fixed 2:1 risk-reward ratio promotes long-term profitability

- Technical indicator combination reduces false signals

Strategy Risks

- May miss major trends in strongly trending markets

- Frequent trading possible in narrow consolidation ranges

- Slippage risk during market gaps

- Requires ongoing parameter monitoring and adjustment

- Trading costs may impact strategy returns

Optimization Directions

- Add volume indicators for confirmation

- Implement volatility filters to avoid high volatility periods

- Optimize parameter adaptation mechanisms

- Include additional technical indicators for cross-validation

- Enhance money management system

Summary

This strategy combines classical technical analysis with modern quantitative methods. Through multiple indicator confirmations and strict risk control, the strategy demonstrates good practicality. Thorough backtesting and demo trading are recommended before live implementation.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1