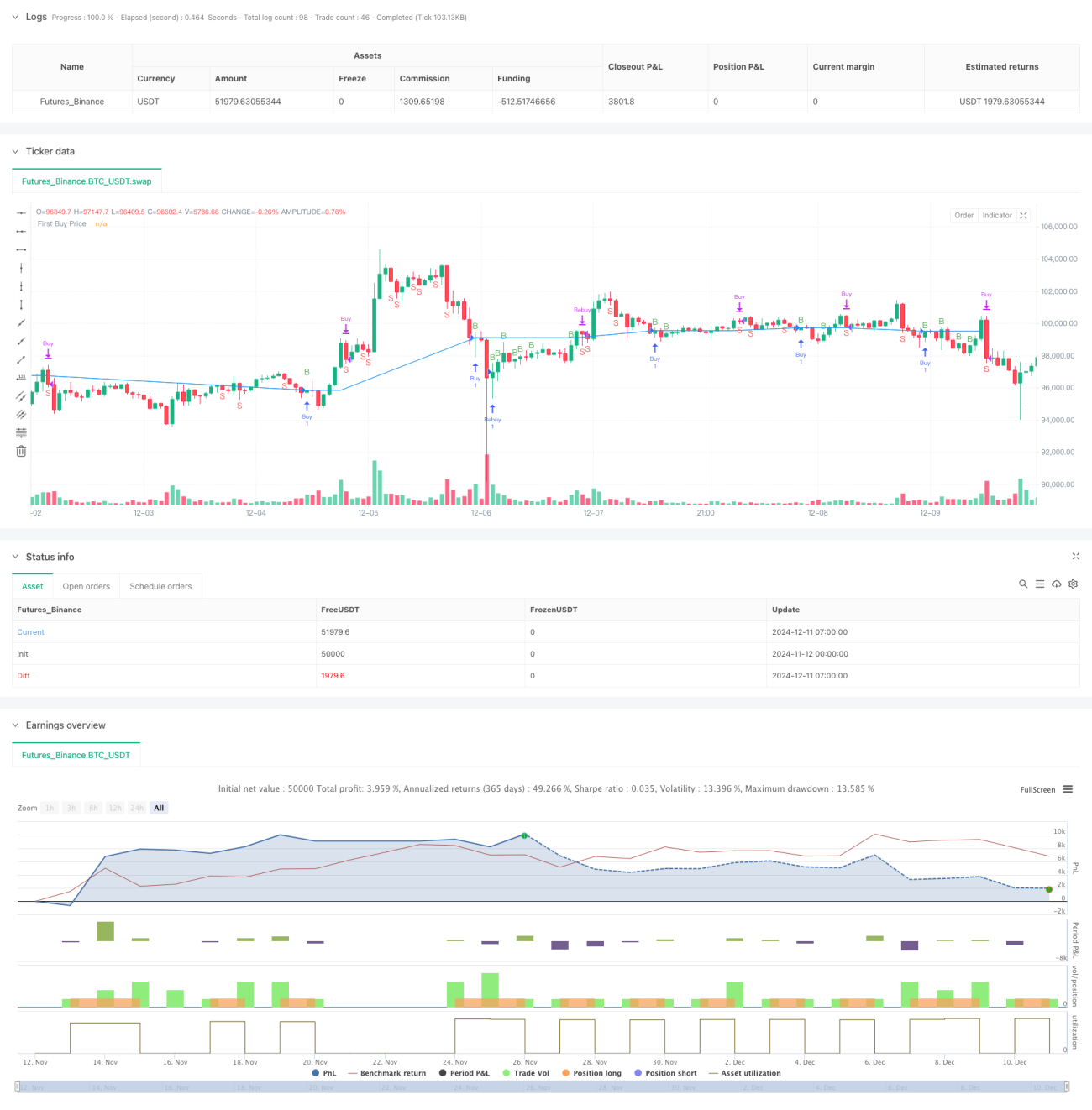

Overview

This strategy is an adaptive trading system based on dual RSI (Relative Strength Index) indicators. It combines RSI indicators from different timeframes to identify market trends and trading opportunities while optimizing trading performance through money management and risk control mechanisms. The core strength of the strategy lies in the synergy between multi-period RSIs to enhance profitability while maintaining trading safety.

Strategy Principles

The strategy uses a 7-period RSI indicator as the primary trading signal, combined with a daily RSI as a trend filter. A long position is initiated when the short-period RSI breaks above 40 and the daily RSI is above 55. If the price drops below the initial entry price during a position, the system automatically adds to the position to lower the average cost. Positions are closed when RSI breaks below from above 60. A 5% stop-loss is implemented for risk control. The strategy also includes a money management module that automatically calculates position sizes based on total capital and preset risk ratios.

Strategy Advantages

- Multi-period RSI combination improves signal reliability

- Adaptive position averaging mechanism effectively reduces holding costs

- Comprehensive money management system adjusts positions based on risk preference

- Fixed stop-loss protection strictly controls risk per trade

- Considers trading costs for more realistic trading conditions

Strategy Risks

- RSI indicators may generate false signals in volatile markets

- Position averaging mechanism may lead to significant losses in continuous downtrends

- Fixed percentage stop-loss may be too conservative in high volatility periods

- Trading costs can significantly impact returns during frequent trading

- Strategy execution requires sufficient liquidity

Optimization Directions

- Incorporate volatility indicators (like ATR) for dynamic stop-loss adjustment

- Add trend strength filters to reduce false signals in ranging markets

- Optimize position averaging logic with dynamic adjustments based on market volatility

- Include RSI confirmations from additional timeframes

- Develop adaptive position sizing system

Summary

This is a complete trading system combining technical analysis and risk management. It generates trading signals through multi-period RSI coordination while controlling risk through money management and stop-loss mechanisms. The strategy is suitable for trending markets but requires parameter optimization based on actual market conditions. The system's good extensibility leaves room for further optimization.

- 1