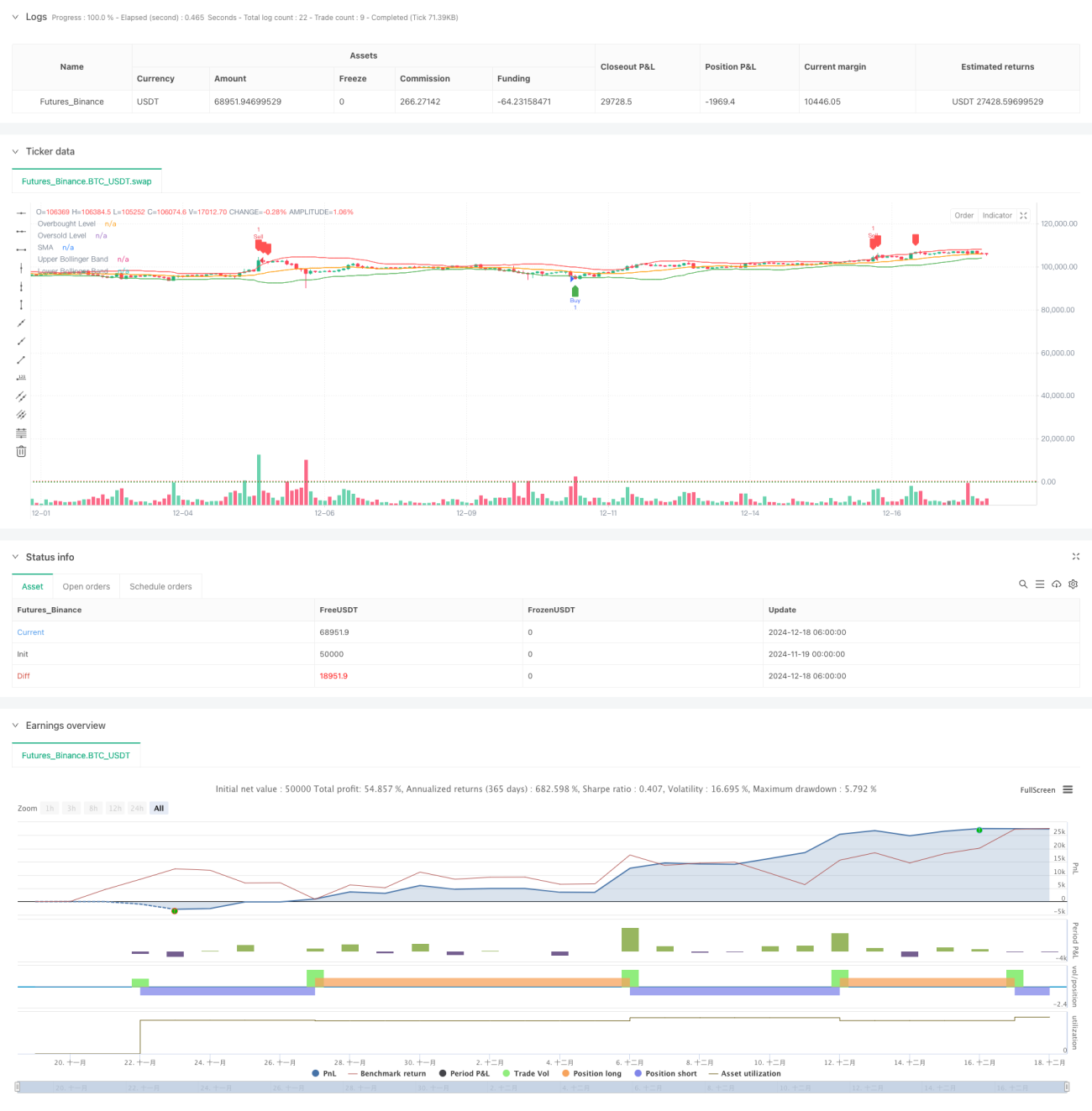

Overview

This strategy is a mean reversion trading system that combines Bollinger Bands and Relative Strength Index (RSI). It identifies extreme price deviations from the mean and uses RSI overbought/oversold signals to determine trading opportunities. Buy signals are generated when price breaks below the lower Bollinger Band and RSI is in oversold territory, while sell signals occur when price breaks above the upper Bollinger Band and RSI is in overbought territory.

Strategy Principle

The core logic is based on the mean reversion characteristic of financial markets. The implementation uses a 20-day Simple Moving Average (SMA) as the mean reference, with a standard deviation multiplier of 2.0 for Bollinger Band width calculation. A 14-day RSI is integrated as a supplementary indicator, with 70 and 30 set as overbought and oversold thresholds respectively. Trades are only triggered when price breaks the Bollinger Bands and RSI reaches extreme values, creating a dual confirmation mechanism that enhances strategy reliability.

Strategy Advantages

- Combines multiple technical indicators for more reliable trading signals

- Effectively filters false breakouts using RSI confirmation

- Highly adjustable parameters to adapt to different market conditions

- Clear strategy logic that is easy to understand and implement

- Comprehensive risk control mechanism

- Clean and efficient code implementation for easy maintenance and optimization

Strategy Risks

- May exit positions prematurely in trending markets, affecting returns

- Improper parameter selection can lead to delayed signals

- Potential for significant drawdowns during extreme market volatility

- Need to consider the impact of trading costs on strategy returns

- Strategy performance varies significantly across different market conditions

Optimization Directions

- Implement adaptive Bollinger Band width based on market volatility

- Add trend filters to reduce trading frequency in strong trend markets

- Optimize RSI parameters with adaptive periods

- Incorporate stop-loss and take-profit mechanisms to improve risk-reward ratio

- Consider adding volume indicators to enhance signal reliability

- Develop parameter optimization module for strategy auto-tuning

Summary

This strategy constructs a robust mean reversion trading system through the synergy of Bollinger Bands and RSI. The strategy design is reasonable with good scalability and adaptability. Through continuous optimization and improvement, the strategy's stability and profitability can be further enhanced. It is recommended to conduct thorough backtesting before live trading and adjust parameters according to specific market characteristics.

- 1