Multi-EMA Trend-Following Swing Trading Strategy with ATR-Based Risk Management

Overview

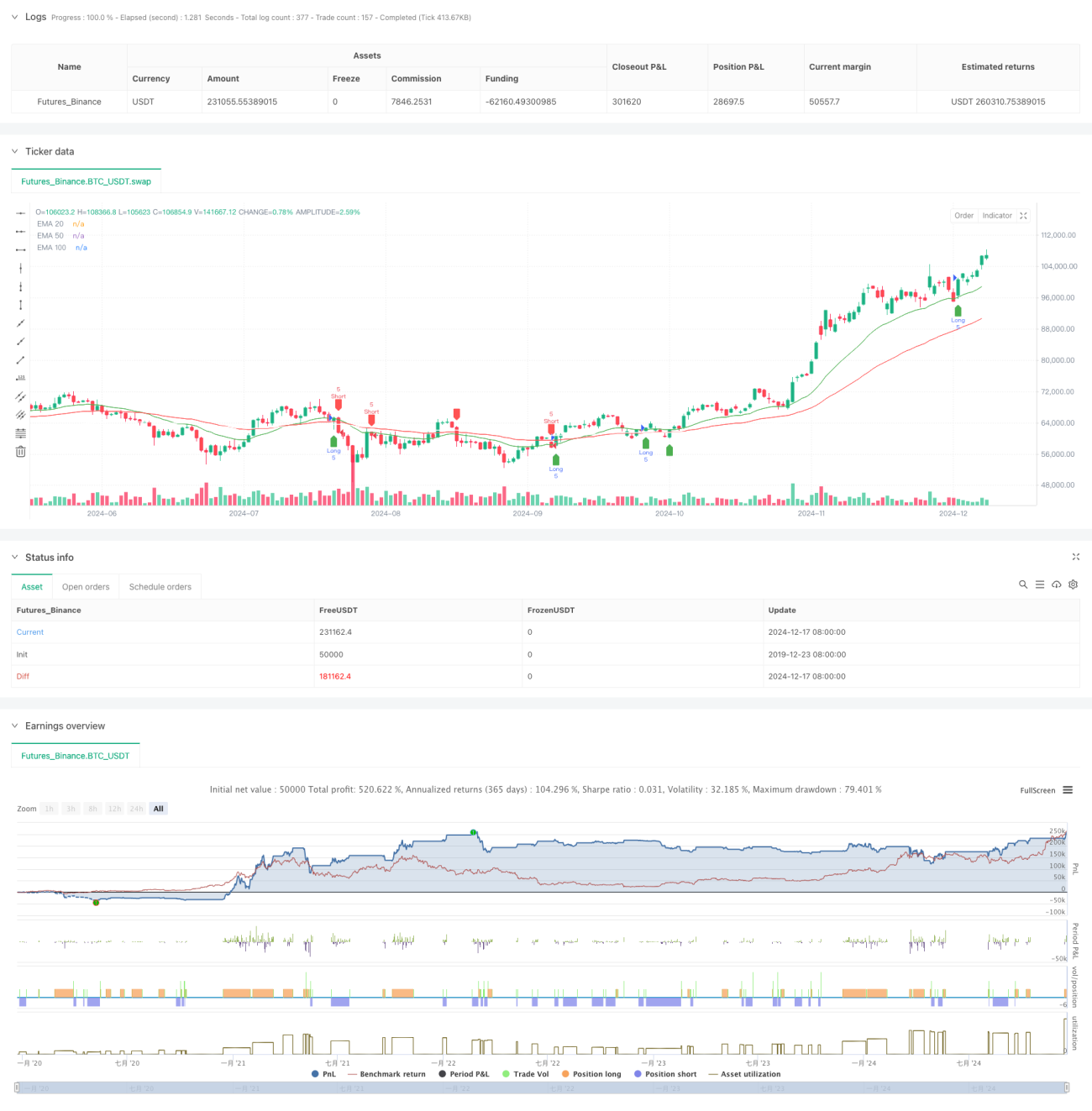

This strategy is a trend-following trading system based on multiple Exponential Moving Averages (EMAs) and Average True Range (ATR). It uses three EMAs (20, 50, and 100 periods) in conjunction with ATR for dynamic risk management and profit targeting. This approach ensures systematic trading while maintaining dynamic risk control.

Strategy Principles

The core logic is built on the interaction between price and multiple EMAs:

- Entry signals are based on price crossovers with the 20-period EMA, filtered by the 50-period EMA

- Long entry conditions: price crosses above 20 EMA and is above 50 EMA

- Short entry conditions: price crosses below 20 EMA and is below 50 EMA

- Stop-loss: dynamically calculated using 14-period ATR to adapt to market volatility

- Profit target: uses a 1.5 risk-reward ratio, setting profit targets at 1.5 times the stop-loss distance

Strategy Advantages

- Multiple timeframe validation: Uses 20/50/100 EMAs to reduce false signals

- Dynamic risk management: ATR-based stops provide market-adaptive risk control

- Clear risk-reward ratio: Fixed 1.5 R/R setting promotes long-term profitability

- Combines trend-following with swing trading: Captures both major trends and short-term opportunities

- Visualized trading signals: Provides clear graphical interface for better understanding and execution

Strategy Risks

- Choppy market risk: May generate frequent false breakout signals during consolidation

- Slippage risk: Actual execution prices may differ from signal prices during rapid market movements

- Trend reversal risk: Sudden trend reversals may result in significant losses

- Parameter optimization risk: Over-optimization may lead to poor real-world performance

Optimization Directions

- Incorporate volume indicators: Use volume to confirm price breakout validity

- Add trend strength filters: Consider ADX or similar indicators to improve entry quality

- Optimize stop-loss method: Consider implementing trailing stops for better profit protection

- Market environment classification: Adjust parameters based on different market conditions

- Add volatility filters: Suspend trading during excessive market volatility

Summary

This strategy combines multiple EMAs and ATR-based dynamic risk control to create a trading system that features both trend-following and swing trading characteristics. Its strengths lie in systematic approach and controllable risk, but practical application requires attention to market adaptability and specific optimizations based on actual conditions. Through proper parameter settings and strict risk control, the strategy has the potential to achieve stable trading results across most market environments.

- 1