Multi-Level Institutional Order Flow Quantitative Strategy with Dynamic Position Scaling System

Overview

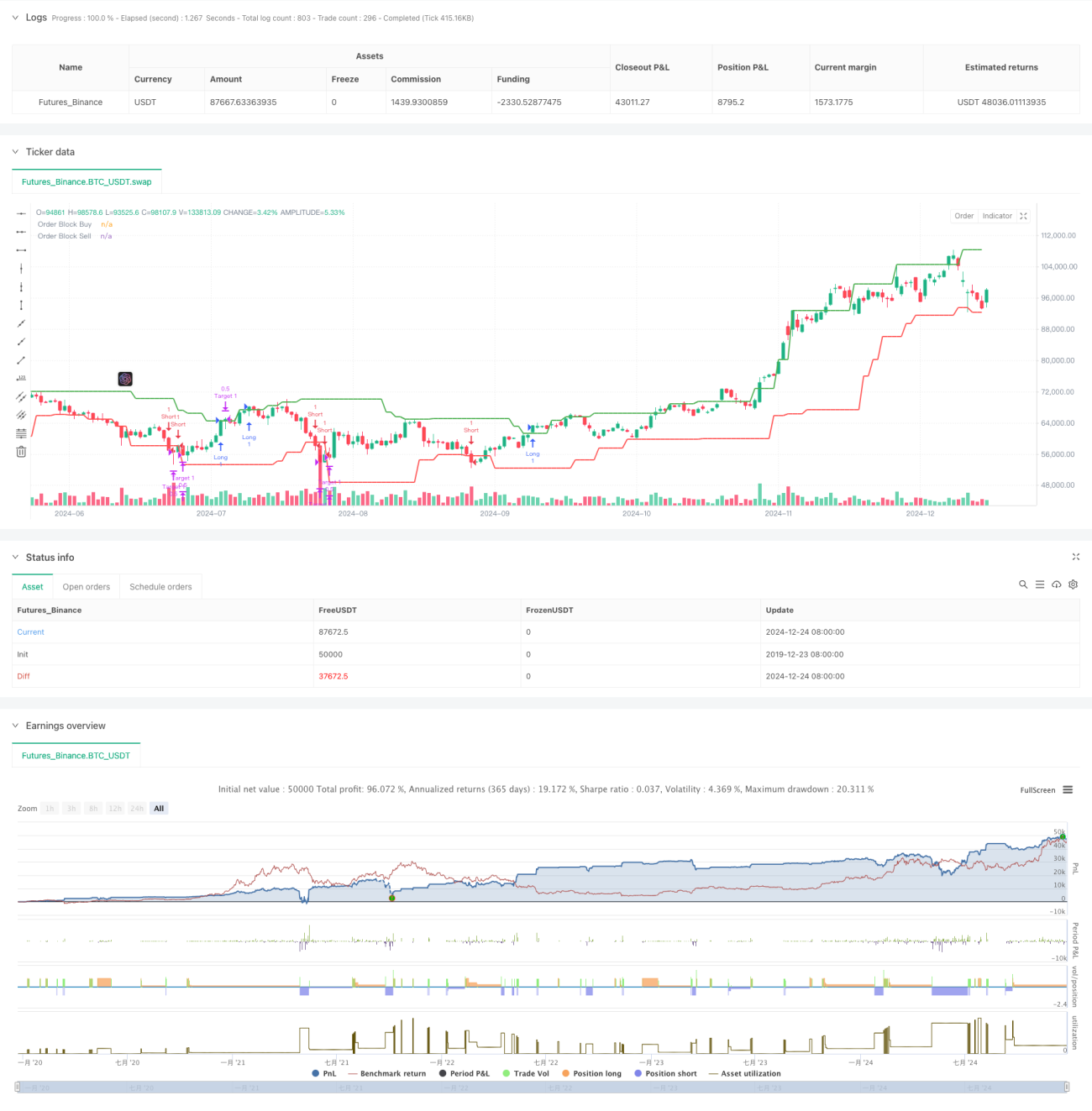

This strategy is an intelligent trading system based on institutional order flow, which predicts potential price reversal points by identifying Order Blocks in the market. The system employs a dynamic position scaling management approach with three-tier targets to optimize position management and maximize returns. The core of the strategy lies in capturing price footprints left by institutional trading behavior through statistical analysis of highs and lows.

Strategy Principles

The strategy is based on several key elements:

- Order Block Identification - Using a 20-period lookback window to identify buy and sell order blocks through candlestick pattern analysis. Buy blocks are confirmed by the combination of a previous bearish candle and current bullish candle, while sell blocks follow the opposite pattern.

- Trading Time Control - Trading is restricted to the main session of 09:30-16:00, avoiding high volatility periods during market open and close.

- Entry Logic - Long positions are opened when price breaks above the buy order block during trading hours, and short positions when price breaks below the sell order block.

- Position Scaling - Implements a 50%-30%-20% three-tier scaling system corresponding to 0.5%, 1.0%, and 1.5% targets.

Strategy Advantages

- Smart Order Detection - Accurately captures key price levels where large capital positions are built or closed through dynamic analysis of highs and lows.

- Risk Distribution - Three-tier position scaling effectively distributes risk, securing profits while allowing trends to develop fully.

- Time Filtering - Trading time restrictions avoid high volatility periods, improving trading stability.

- Visual Support - Strategy provides clear order block visualization, helping traders understand market structure.

Strategy Risks

- False Breakout Risk - Multiple false signals may occur in ranging markets, suggesting the need for volatility indicator filtering.

- Slippage Impact - Position scaling exits may face slippage in low liquidity markets, requiring appropriate target spacing adjustment.

- Trend Dependency - Strategy performs well in trending markets but may generate frequent trades in ranging conditions.

Strategy Optimization

- Volatility Adaptation - Recommend incorporating ATR indicator to dynamically adjust target percentages based on market volatility.

- Order Flow Volume Analysis - Consider combining volume analysis to increase order block confirmation reliability.

- Dynamic Time Window - Consider dynamically adjusting the lookback period based on market conditions to improve strategy adaptability.

- Enhanced Risk Control - Add maximum drawdown limits and daily loss limits to improve strategy robustness.

Summary

This strategy constructs a complete trading system through institutional order flow analysis and dynamic position management. Through order block identification and multi-level profit-taking settings, it captures opportunities from large capital operations while implementing effective risk control. Traders are advised to carefully consider market conditions and adjust parameters according to specific circumstances in live trading.

- 1