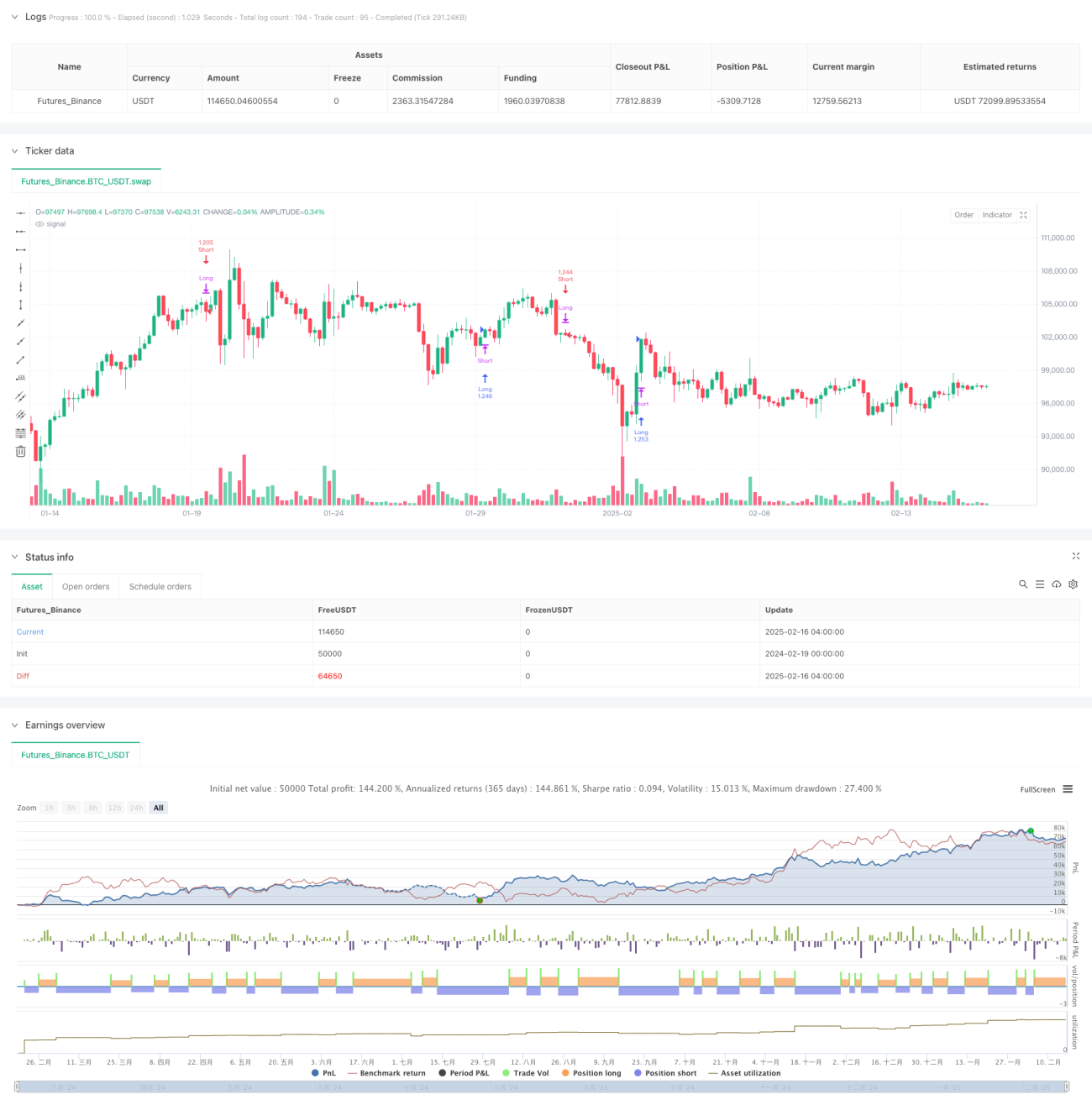

Overview

This strategy is a trend-following trading system based on an enhanced Relative Strength Index (RSI). It captures trend reversal opportunities across different market cycles by calculating an improved version of RSI and combining it with its signal line. The strategy not only computes indicator values but also provides visual representation of overbought and oversold areas to help traders make more intuitive market judgments.

Strategy Principles

The core principle revolves around identifying market trends through an Augmented RSI (ARSI) calculation, including:

- Calculating highest and lowest prices within a specified period to determine price range

- Computing differences based on price changes

- Smoothing the differences using selectable moving average methods (EMA, SMA, RMA, TMA)

- Normalizing results to a 0-100 range

- Generating long signals when ARSI crosses above its signal line below 50

- Generating short signals when ARSI crosses below its signal line above 50

Strategy Advantages

- Robust Signal Confirmation - Ensures reliability through ARSI crossovers and midline filtering

- High Adaptability - Supports multiple moving average methods for different market characteristics

- Reasonable Risk Control - Employs position percentage management for effective risk control

- Outstanding Visualization - Clearly displays overbought/oversold areas through color filling

- Reverse Position Management - Automatically closes existing positions on contrary signals

Strategy Risks

- Oscillation Market Risk - May generate frequent false signals in sideways markets

- Lag Risk - Signals have inherent lag due to moving average calculations

- Parameter Sensitivity - Different parameter settings may lead to significant performance variations

- Market Adaptability Risk - Strategy performance may vary significantly across different market environments

- Money Management Risk - Fixed percentage position sizing may pose risks during high volatility

Optimization Directions

- Volatility Filtering - Add ATR indicator to filter signals in low volatility environments

- Additional Trend Confirmation - Incorporate longer-period trend indicators to improve signal reliability

- Position Management Optimization - Dynamically adjust position sizes based on market volatility

- Stop Loss Implementation - Develop ATR-based dynamic stop-loss for better risk control

- Adaptive Parameters - Research dynamic parameter optimization methods to improve adaptability

Summary

This is a well-structured trend-following strategy with clear logic. Through innovative ARSI calculation methods and the combination of various technical indicators' advantages, it forms a reliable trading system. While inherent risks exist, the strategy shows good practical application potential through reasonable optimization and risk management measures. Traders are advised to thoroughly test parameter settings and adjust strategy configuration according to market conditions when implementing in live trading.

/*backtest

start: 2024-02-19 00:00:00

end: 2025-02-16 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Ultimate RSI [LuxAlgo] Strategy", shorttitle="ULT RSI Strat", overlay=false, initial_capital=10000, currency=currency.USD, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

//------------------------------------------------------------------------------- 1