Quantitative Momentum-Based Micropullback Breakout Strategy

Overview

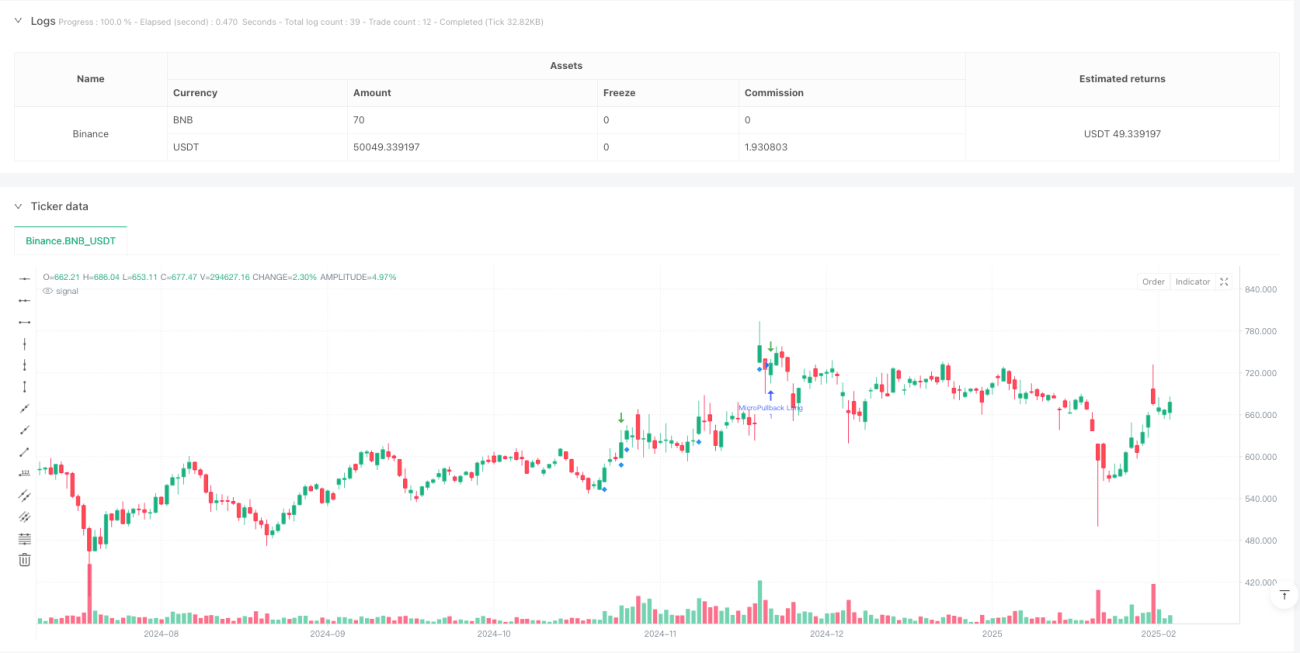

This strategy is a trading system based on price momentum and volume, focusing on identifying micropullback opportunities after strong upward movements. The strategy monitors short-term pullbacks following large green candles and enters trades when price reversal signals appear. The system employs multiple filtering conditions, including volume, ATR volatility, and pullback magnitude restrictions, to enhance trading accuracy.

Strategy Principles

The core logic is based on market momentum continuation, incorporating the following key elements:

- Identifies strong upward candles through volume and ATR multiples, requiring volume above 1.5x average and exceeding 200,000

- Monitors pullback process after upward movement, limiting maximum consecutive red candles to 3

- Sets maximum pullback magnitude at 50%, abandoning trade opportunities if exceeded

- Triggers long signals when price breaks above previous high after pullback stabilization

- Employs OCO order combination for position management, including stop-loss and profit targets

- Sets stop-loss below pullback low, with profit target at 2x risk

Strategy Advantages

- Combines price momentum and volume confirmation, improving signal reliability

- Filters false breakouts through strict pullback conditions

- Uses objective technical indicators, reducing subjective judgment impact

- Clear risk control mechanism with fixed risk-reward ratio

- High degree of system automation, suitable for batch trading multiple instruments

- Good scalability, easy to add new filtering conditions

Strategy Risks

- May trigger frequent false signals during market volatility

- High-momentum stocks' pullbacks might exceed preset limits

- Volume conditions require dynamic adjustment in different market environments

- Stop-loss placement might be too tight, susceptible to market noise

- Profit targets may be too aggressive, difficult to fully achieve

- Requires large sample size to verify strategy stability

Strategy Optimization Directions

- Introduce trend filters, such as moving average systems or trend indicators, to ensure trading with main trend

- Dynamically adjust volume thresholds to adapt to different market cycles

- Optimize stop-loss placement, consider using ATR multiples

- Add time filters to avoid market opening and closing volatility

- Incorporate multi-timeframe confirmation to improve signal reliability

- Develop adaptive parameter system to adjust strategy parameters based on market conditions

Summary

This is a well-designed trend-following strategy that captures quality trading opportunities through strict condition screening and risk management. The key to strategy success lies in parameter optimization and adaptability to market conditions. It is recommended to conduct thorough backtesting before live trading and adjust parameters according to specific trading instrument characteristics.

- 1