Dynamic DCA-based Cryptocurrency Quantitative Trading Strategy

Overview

This is a quantitative trading strategy specifically designed for the cryptocurrency market, leveraging its high volatility characteristics through intelligent Dollar-Cost Averaging (DCA) with dynamic position scaling during price retracements. Operating on a 15-minute timeframe, it effectively handles rapid cryptocurrency market fluctuations while avoiding overtrading risks.

Strategy Principles

The strategy consists of four core modules:

- Smart Entry System: Initial position based on OHLC4 weighted average price, adapted to cryptocurrency market volatility

- Dynamic Accumulation Mechanism: Triggers safety orders during price retracements, scaling position size with depth to utilize market volatility

- Risk Management System: Optimizes risk-reward ratio through pyramiding and flexible leverage adjustment

- Rapid Take-Profit Control: Designed for cryptocurrency market's quick fluctuations, including fee optimization

Strategy Advantages

- Market Adaptability: Specifically optimized for cryptocurrency market's high volatility

- Risk Diversification: Reduces sudden risks in cryptocurrency markets through dynamic staged positioning

- Arbitrage Efficiency: Effectively captures profits from cryptocurrency price volatility

- Automated Execution: Supports API integration with major cryptocurrency exchanges

- Capital Efficiency: Improves capital utilization through intelligent leverage management

Strategy Risks

- Market Risk: Extreme cryptocurrency volatility may lead to significant drawdowns

- Liquidity Risk: Some small-cap cryptocurrencies may face insufficient liquidity

- Leverage Risk: High cryptocurrency volatility increases leverage trading risks

- Technical Risk: Depends on exchange API stability and network connection quality

- Regulatory Risk: Cryptocurrency market policy changes may affect strategy execution

Strategy Optimization Directions

- Volatility Adaptation: Introduce cryptocurrency-specific volatility indicators for dynamic parameter adjustment

- Multi-coin Synergy: Develop multi-cryptocurrency trading logic to diversify single-coin risk

- Market Sentiment Filtering: Integrate cryptocurrency market sentiment indicators to optimize entry timing

- Transaction Cost Optimization: Reduce costs through smart routing and exchange selection

- Risk Alert Mechanism: Establish warning system based on market abnormal fluctuations

Summary

The strategy provides a comprehensive automated solution for cryptocurrency trading through innovative DCA methods and dynamic risk management. While cryptocurrency markets carry high risks, the strategy maintains stability in most market conditions through carefully designed risk control mechanisms and market adaptability optimization. Future improvements will focus on enhancing strategy adaptation to cryptocurrency market specificities.

/*backtest

start: 2020-08-29 15:00:00

end: 2025-02-18 17:22:45

period: 1h

basePeriod: 1h

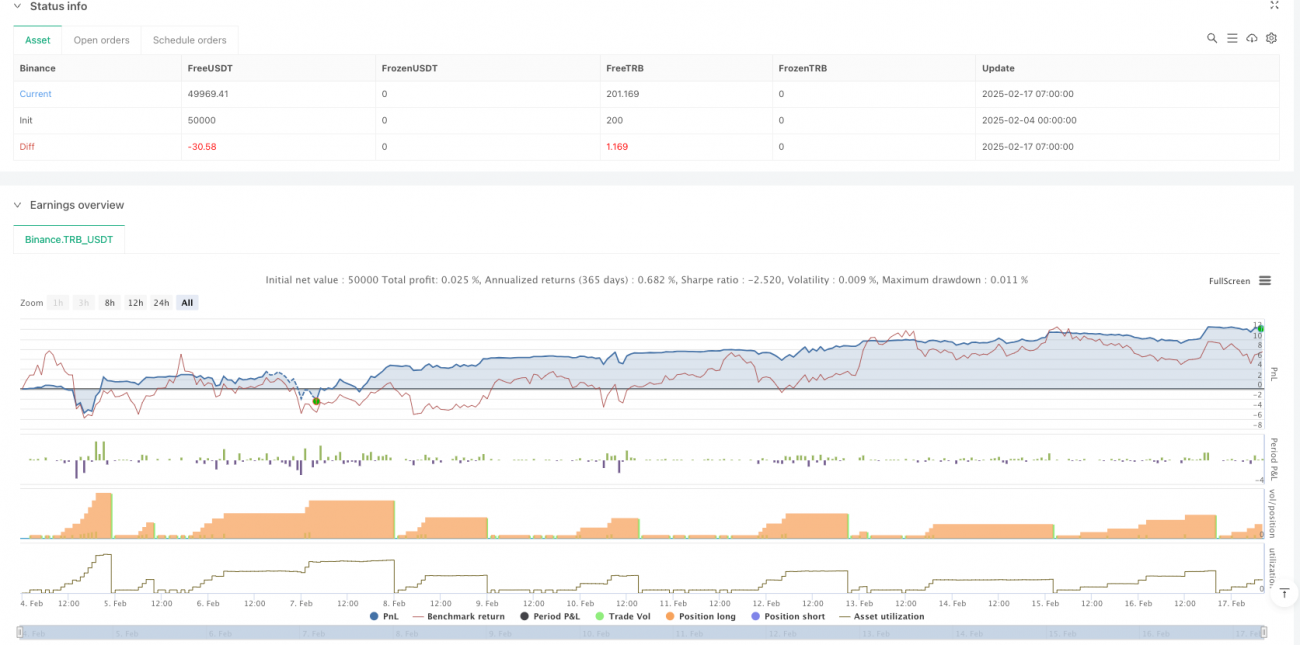

exchanges: [{"eid":"Binance","currency":"TRB_USDT"}]

*/

//@version=5

strategy('Autotrade.it DCA', overlay=true, pyramiding=999, default_qty_type=strategy.cash, initial_capital=10000, commission_value=0.02)

// Date Ranges- 1