Price Range and Breakout Based Efficient Quantitative Trading Strategy

Overview

This is an efficient quantitative trading strategy based on price range and breakout. The strategy primarily identifies consolidation zones in the market and executes trades when prices break out of these zones. It uses the ZigZag indicator to identify key price points, combines highs and lows to define consolidation areas, and generates trading signals when prices break through these areas.

Strategy Principles

The core logic includes the following key steps:

- Identify important turning points through highest and lowest prices within the Loopback Period

- Use ZigZag algorithm to track price movements and determine key support and resistance levels

- Confirm valid consolidation zones by setting minimum consolidation length

- Dynamically update upper and lower boundaries to track changes in consolidation areas

- Trigger trading signals when price breaks out of consolidation zones

Strategy Advantages

- High Adaptability - Strategy can dynamically identify and update consolidation zones, adapting to different market environments

- Controlled Risk - Provides clear stop-loss positions through well-defined consolidation zones

- Visual Support - Offers visualization of consolidation areas, helping traders understand market conditions

- Bi-directional Trading - Supports both upward and downward breakout opportunities, maximizing market opportunities

- Adjustable Parameters - Provides multiple adjustable parameters for optimization based on different market characteristics

Strategy Risks

- False Breakout Risk - Market may exhibit false breakouts leading to failed trades

- Slippage Risk - May face significant slippage in fast-moving markets

- Market Environment Dependency - Strategy performs well in ranging markets but may underperform in trending markets

- Parameter Sensitivity - Improper parameter settings may affect strategy performance

- Money Management Risk - Requires proper control of position sizing for each trade

Strategy Optimization Directions

- Incorporate Volume Indicators - Confirm breakout validity through volume analysis

- Optimize Entry Timing - Add pullback confirmation mechanism to improve entry quality

- Enhance Stop-Loss Mechanism - Design more flexible stop-loss strategies

- Add Market Environment Filters - Include trend assessment to operate in suitable market conditions

- Optimize Parameter Adaptation - Automatically adjust parameters based on market volatility

Summary

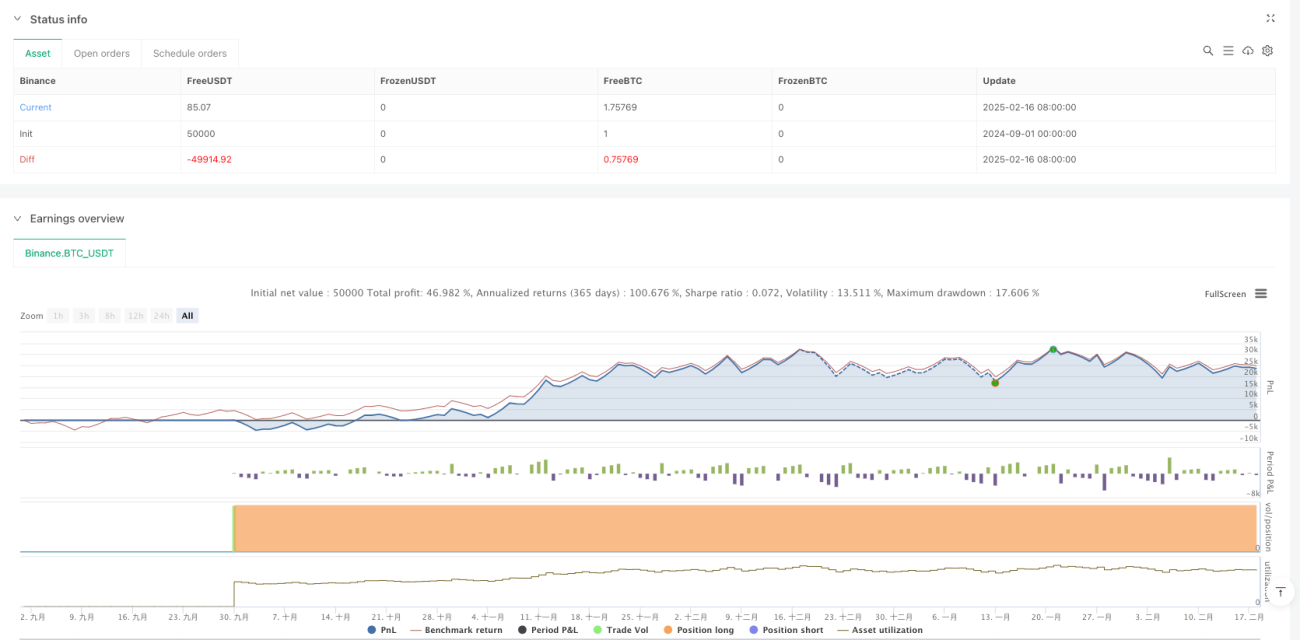

This is a well-designed quantitative trading strategy with clear logic. Through the identification of consolidation zones and capture of breakout signals, it provides traders with a reliable trading system. The strategy's visualization capabilities and parameter flexibility make it highly practical. Through continuous optimization and risk control, this strategy has the potential to achieve stable returns in actual trading.

- 1