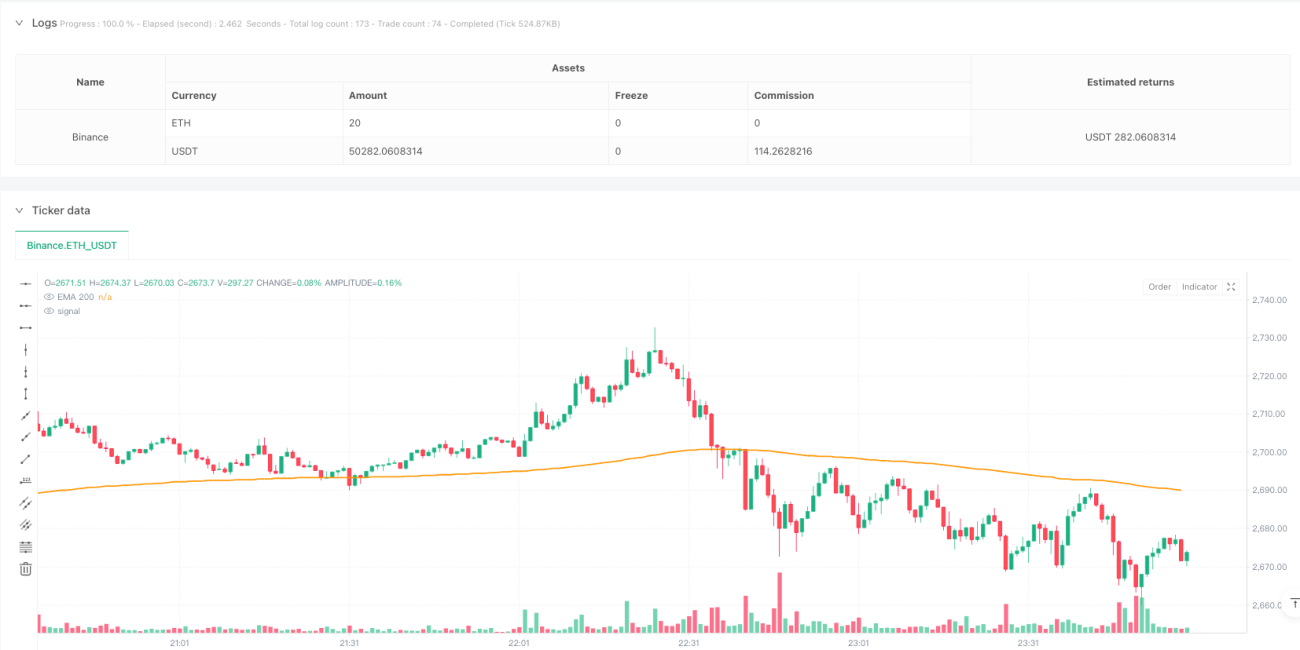

Overview

This strategy is a bidirectional trading system that combines MACD momentum indicator with EMA trend analysis. It primarily bases entry decisions on MACD crossover signals and price position relative to EMA(200). The strategy employs a 2:1 risk-reward ratio, can operate on a 5-minute timeframe, and supports flexible parameter adjustment.

Strategy Principles

The core logic is based on the following key conditions:

- Long Entry Conditions:

- Price above EMA(200)

- MACD line crosses signal line from below

- MACD value below zero line

- Short Entry Conditions:

- Price below EMA(200)

- MACD line crosses signal line from above

- MACD value above zero line

- Risk management uses preset stop-loss and take-profit ratios, defaulting to 1:2

Strategy Advantages

- Clear and simple logic, easy to understand and implement

- Combines trend and momentum indicators for more reliable trading signals

- Features flexible parameter settings for optimization across different market conditions

- Supports bidirectional trading to capture market opportunities

- Built-in risk management mechanism helps protect capital

Strategy Risks

- May generate frequent false signals in ranging markets

- Fixed stop-loss and take-profit ratios might not suit all market conditions

- Sensitive to changes in market volatility

- Frequent trading may result in high commission costs

- Might miss some opportunities in fast-moving markets

Strategy Optimization Directions

- Introduce volatility indicators for dynamic adjustment of stop-loss and take-profit levels

- Add volume confirmation signals to improve entry quality

- Implement market environment filters to avoid trading under unfavorable conditions

- Develop dynamic parameter optimization system

- Add time filters to avoid trading during low liquidity periods

Summary

This is a well-designed strategy system that provides relatively reliable trading signals through the combination of technical indicators. While there are some potential risks, the strategy shows good practical application potential through proper optimization and risk management. It is recommended to conduct thorough backtesting before live trading and adjust parameters according to specific market conditions.

- 1