Volume Spike and RSI Enhanced Trading Strategy

Overview

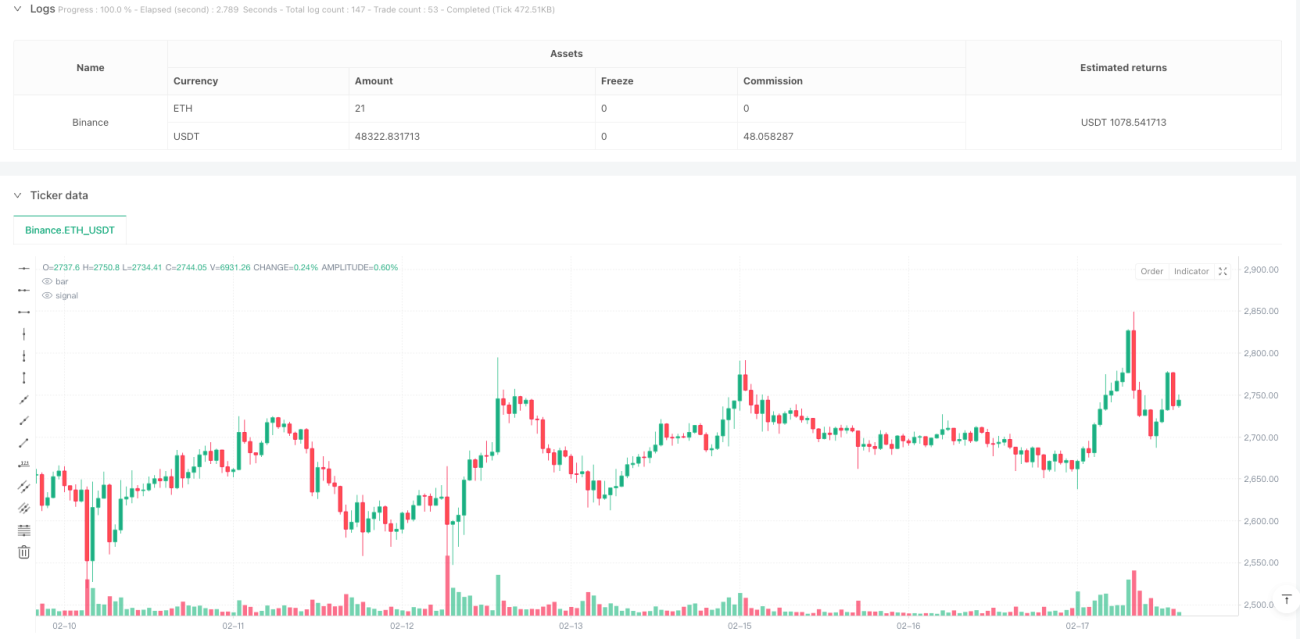

This strategy is a trading system based on volume anomalies and RSI indicators. It identifies potential trading opportunities by monitoring volume breakouts and RSI overbought/oversold levels, combined with price action confirmation. The strategy employs dynamic stop-loss and take-profit targets to optimize risk-reward configuration.

Strategy Principles

The core logic includes several key elements:

- Volume Verification: Uses 20-period SMA to calculate average volume, triggering volume spike signals when real-time volume exceeds 1.5 times the average

- RSI Indicator: Employs 14-period RSI for overbought/oversold detection, with RSI<30 considered oversold and RSI>70 overbought

- Entry Conditions:

- Long: Volume spike + RSI oversold + closing price above opening price

- Short: Volume spike + RSI overbought + closing price below opening price

- Risk Management: Uses ATR for dynamic stop-loss calculation and automatically determines profit targets based on set risk-reward ratio (1:2)

Strategy Advantages

- Multiple Confirmation Mechanism: Combines volume, RSI, and price action dimensions for trade confirmation, improving signal reliability

- Dynamic Risk Management: Adjusts stop-loss positions through ATR, better adapting to market volatility changes

- All-Session Applicability: Not restricted by time, capable of capturing trading opportunities around the clock

- High Customizability: Key parameters like RSI thresholds, volume multiplier, risk-reward ratio can be adjusted according to specific needs

- Clear Visualization: Marks trading signals with background colors, facilitating strategy monitoring and backtesting analysis

Strategy Risks

- False Breakout Risk: Volume spikes may arise from market noise, requiring optimization through volume multiplier parameter adjustment

- Off-Hours Risk: During periods of low market liquidity, slippage or execution difficulties may occur

- Market Environment Dependency: Strategy may perform better in trending markets than ranging markets

- Parameter Sensitivity: Multiple key parameter settings significantly affect strategy performance, requiring thorough testing

Strategy Optimization Directions

- Market State Recognition: Add market condition assessment mechanism to use different parameter settings under different market conditions

- Signal Filtering: Add trend filters, such as moving average systems, to improve trade direction accuracy

- Position Management: Introduce dynamic position sizing mechanism, adjusting position size based on market volatility

- Volume Analysis Enhancement: Incorporate volume pattern analysis, such as volume up/down ratio indicators, to improve volume anomaly detection accuracy

- Liquidity Assessment: Add liquidity evaluation indicators to adjust or pause trading during periods of insufficient liquidity

Summary

The strategy integrates multiple classic technical indicators to build a logically rigorous trading system. Its strengths lie in multiple confirmation mechanisms and comprehensive risk management system, while attention needs to be paid to false breakouts and off-hours risks. Through continuous optimization and improvement, the strategy shows promise for stable performance in actual trading.

- 1