Multi-Dimensional Integration Trading Strategy Based on Nadaraya-Watson

Overview

This strategy is a multi-dimensional trading system based on Nadaraya-Watson kernel regression, which integrates market information from technical, emotional, extrasensory, and intentional dimensions to form comprehensive signals for trading decisions. The strategy employs weight optimization methods, applies weighted processing to signals from different dimensions, and combines trend and momentum filters to improve signal quality. The system also includes a complete risk management module to protect capital through stop-loss and take-profit mechanisms.

Strategy Principles

The core of the strategy lies in using Nadaraya-Watson kernel regression to smooth multi-dimensional market data. Specifically:

- Technical dimension uses closing price

- Emotional dimension uses RSI indicator

- Extrasensory dimension uses ATR volatility

- Intentional dimension uses price deviation from moving average

These dimensions are smoothed through kernel regression and then integrated using preset weights (Technical 0.4, Emotional 0.2, Extrasensory 0.2, Intentional 0.2) to form the final trading signal. Trading orders are issued when the integrated signal crosses its moving average, confirmed by trend and momentum filters.

Strategy Advantages

- Multi-dimensional analysis provides a more comprehensive market perspective, avoiding limitations of single indicators

- Nadaraya-Watson kernel regression effectively reduces market noise, providing smoother signals

- Weight optimization mechanism allows adjustment of dimensional importance based on market characteristics

- Addition of trend and momentum filters significantly improves signal quality

- Comprehensive risk management system ensures capital safety

Strategy Risks

- Parameter optimization may lead to overfitting

- Multiple filtering conditions might miss some valid signals

- Kernel regression has high computational complexity, potentially affecting real-time performance

- Improper weight distribution may weaken important market signals

Mitigation measures include: using out-of-sample testing for parameter validation, dynamically adjusting filter conditions, optimizing computational efficiency, and periodically evaluating and adjusting weight distribution.

Strategy Optimization Directions

- Introduce adaptive weight system to dynamically adjust dimensional weights based on market conditions

- Develop smarter filtering mechanisms to balance signal quality and quantity

- Optimize Nadaraya-Watson algorithm implementation to improve computational efficiency

- Add market cycle recognition module to use different parameter settings in different market phases

- Expand risk management system to include dynamic stop-loss and position management functions

Summary

This is an innovative strategy combining mathematical methods with trading wisdom. Through multi-dimensional analysis and advanced mathematical tools, the strategy can capture multiple aspects of the market, providing relatively reliable trading signals. While there is room for optimization, the overall framework of the strategy is robust and has practical application value.

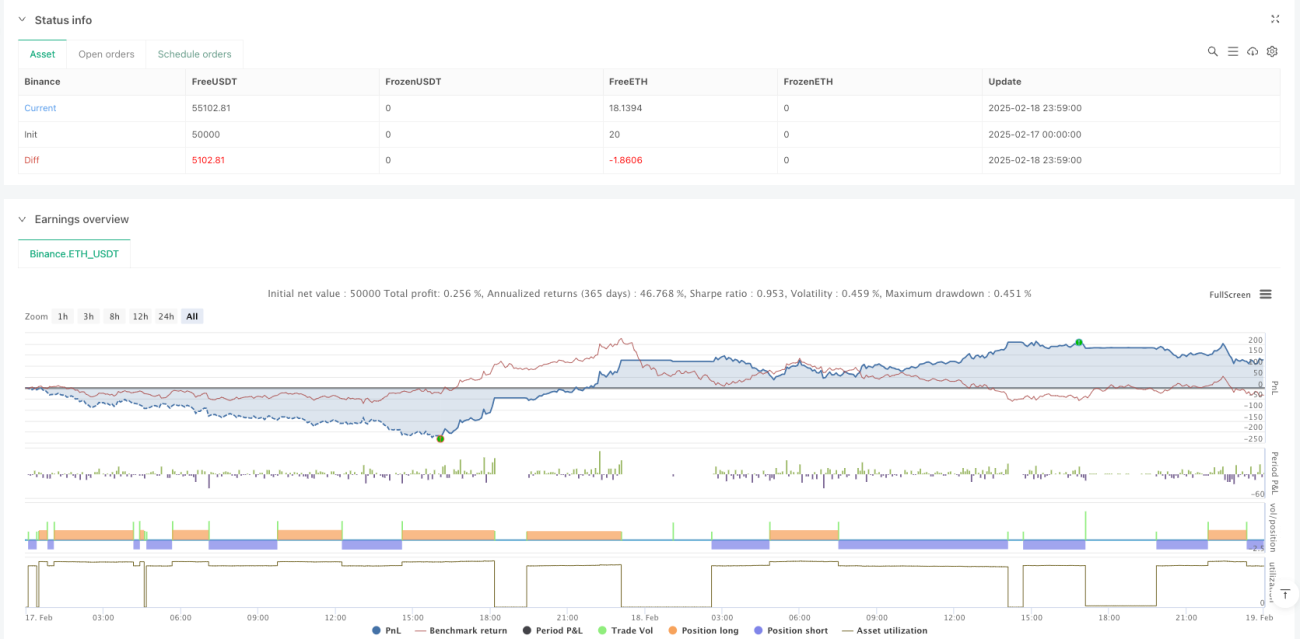

/*backtest

start: 2025-02-17 00:00:00

end: 2025-02-19 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Enhanced Multidimensional Integration Strategy with Nadaraya", overlay=true, initial_capital=10000, currency=currency.USD, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

//────────────────────────────────────────────────────────────────────────────- 1