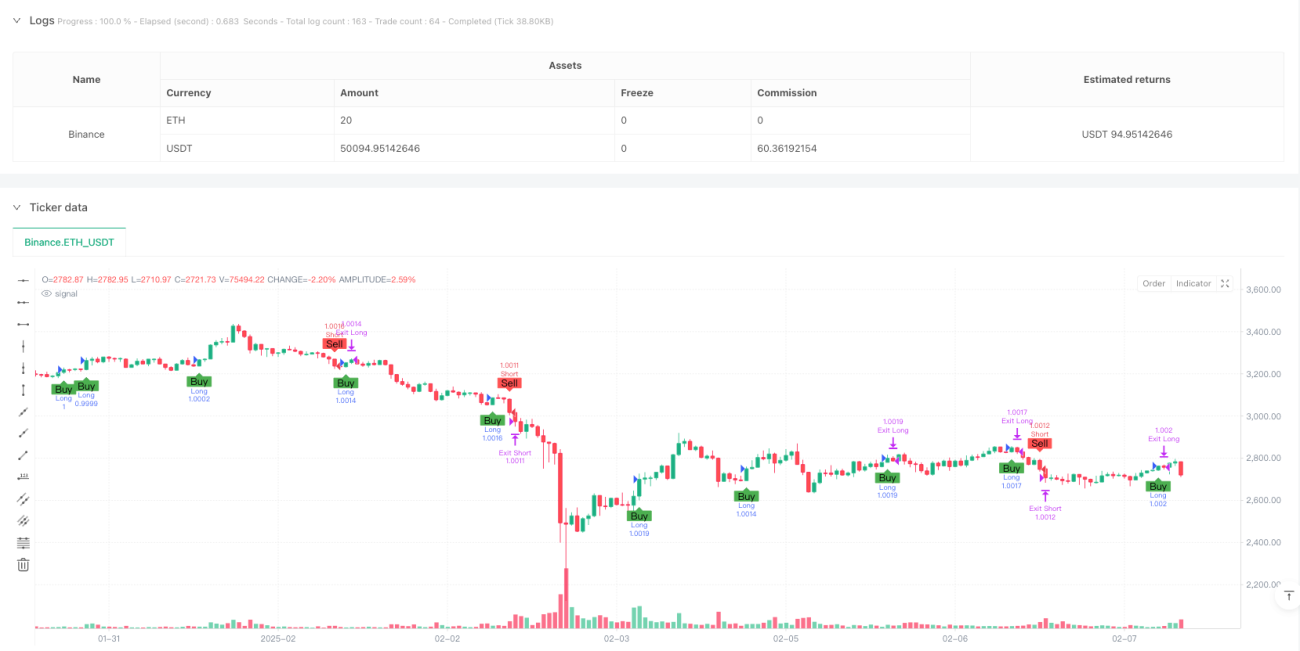

Overview

This is a fully automated trading strategy based on intraday momentum, incorporating strict risk management and precise position sizing systems. The strategy operates primarily during London trading hours, seeking trading opportunities through momentum change identification and Doji pattern exclusion, while implementing daily take-profit rules for risk control. The strategy employs dynamic position management, automatically adjusting trading size based on account equity to optimize capital utilization.

Strategy Principles

The core logic is built on several key components. First, trading is restricted to London hours (excluding 0:00 and after 19:00) to ensure adequate market liquidity. Entry signals are based on price momentum breakouts, specifically requiring the current candle's high to break above the previous candle's high (for longs) or the low to break below the previous candle's low (for shorts), while maintaining directional consistency. To avoid false breakouts, the strategy explicitly excludes Doji candles. The strategy also implements a daily take-profit rule, ceasing new positions once the target profit is achieved.

Strategy Advantages

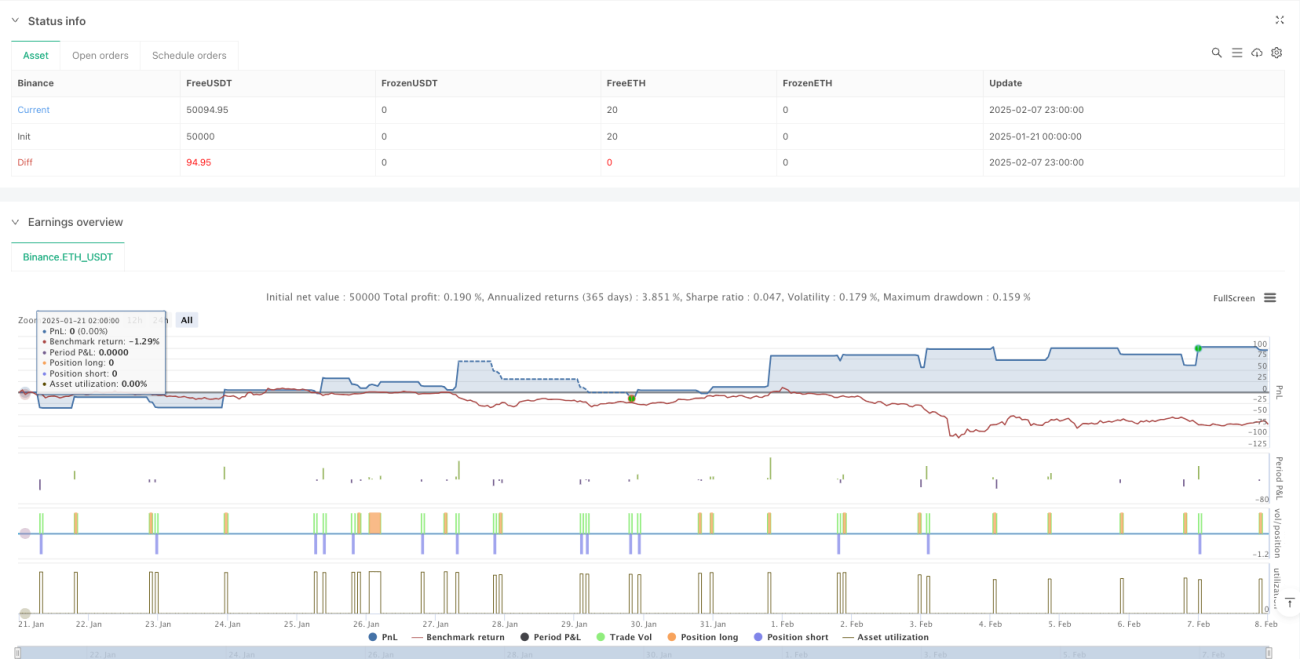

- Comprehensive Risk Management: Includes fixed stop-loss/take-profit, daily profit targets, and dynamic position sizing

- Strong Adaptability: Trading size automatically adjusts based on account equity, suitable for different capital scales

- Liquidity Assurance: Strict trading execution during London hours to avoid low liquidity risks

- False Signal Filtering: Reduces losses from false breakouts by excluding Doji patterns and consecutive signals

- Clear Execution Logic: Well-defined entry and exit conditions for easy monitoring and optimization

Strategy Risks

- Market Volatility Risk: Fixed stop-loss may lack flexibility during high volatility periods

- Price Slippage Risk: May face significant slippage during rapid market movements

- Trend Dependency: Strategy may generate false signals in ranging markets

- Parameter Sensitivity: Strategy performance heavily influenced by stop-loss/take-profit settings

Solutions include: implementing dynamic stop-loss mechanisms, adding volatility filters, and incorporating trend confirmation indicators.

Strategy Optimization Directions

- Introduce Adaptive Stop-Loss: Dynamically adjust stop-loss ranges based on ATR or volatility

- Add Market Environment Filtering: Incorporate trend strength indicators to extend holding periods in clear trends

- Optimize Signal Confirmation: Enhance signal reliability by integrating volume and other technical indicators

- Improve Capital Management: Introduce compound risk management systems considering drawdown control

- Enhance Market Microstructure Analysis: Integrate order flow data for more precise entries

Summary

The strategy builds a comprehensive trading framework by combining momentum breakouts, strict risk management, and automated execution systems. Its main strengths lie in its comprehensive risk control system and adaptive design, though improvements in market environment recognition and signal filtering are needed. Through continuous improvement and parameter optimization, the strategy shows potential for maintaining stable performance across different market conditions.

/*backtest

start: 2025-01-21 00:00:00

end: 2025-02-08 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Trading Strategy for XAUUSD (Gold) – Automated Execution Plan", overlay=true, initial_capital=10000, currency=currency.USD)

//────────────────────────────- 1