Overview

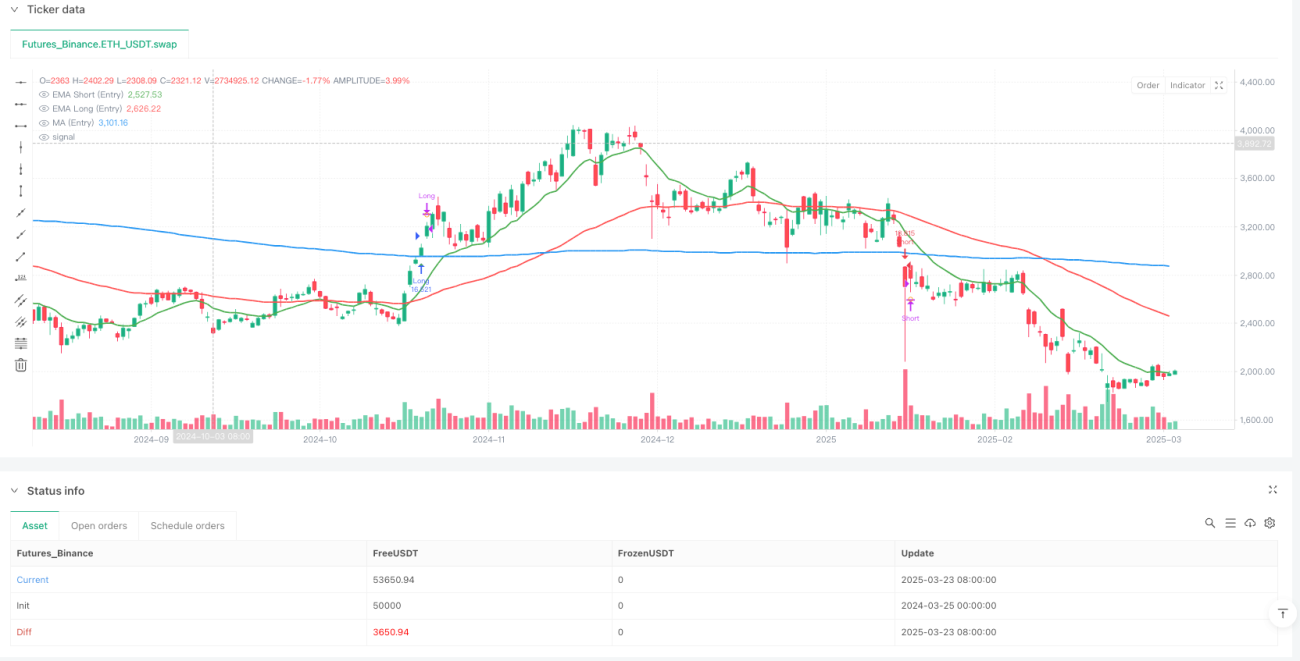

The Multi-Timeframe Momentum Convergence Trading System is a quantitative trading strategy that combines technical indicators with multi-timeframe analysis. The core concept revolves around simultaneously monitoring market trends across short-term (15-minute) and long-term (4-hour) timeframes, using the convergence of EMA (Exponential Moving Average), MA (Moving Average), and RSI (Relative Strength Index) to filter out false signals. The strategy only executes trades when multiple timeframes align in the same direction. It employs EMA crossovers, price breakouts, and RSI momentum confirmation, supplemented by volume verification, to generate high-quality entry signals. Additionally, the system incorporates comprehensive risk management features including ATR-based dynamic stop-losses, fixed percentage take-profit/stop-loss levels, and trailing stops to form a complete trading framework.

Strategy Principles

The core principles of this strategy are based on the synthesis of multiple technical indicators across different timeframes, divided into the following components:

-

Multi-Timeframe Analysis: The strategy simultaneously analyzes 15-minute (entry) and 4-hour (trend confirmation) timeframes to ensure trade direction aligns with the broader market trend.

-

Entry Conditions (15-minute timeframe):

- Long Entry: EMA13 > EMA62 (short-term bullish momentum), close price > MA200 (price above major trend indicator), Fast RSI(7) > Slow RSI(28) (increasing momentum), Fast RSI > 50 (bullish momentum bias), and volume greater than 20-period average.

- Short Entry: Opposite of long conditions, requiring EMA13 < EMA62, close price < MA200, Fast RSI(7) < Slow RSI(28), Fast RSI < 50, with increased volume.

-

Trend Confirmation (4-hour timeframe):

- Long Confirmation: Similar to 15-minute conditions but with slightly different RSI requirements, requiring Slow RSI > 40.

- Short Confirmation: Similarly opposite to long conditions, with Slow RSI < 60.

-

Precise Entry Requirements: The strategy requires either a fresh EMA13 crossover of EMA62 or a price crossing of MA200, providing more precise entry points and avoiding blind entries into trends that have been established for extended periods.

-

Exit Mechanisms: Multiple exit options including technical indicator reversals (EMA relationship changes or RSI reaching overbought/oversold), ATR-based dynamic stops, fixed percentage stop-loss/take-profit, and trailing stops.

Strategy Advantages

-

Systematic Multi-Timeframe Analysis: By analyzing market conditions across different timeframes, the strategy filters out short-term market noise and only enters when trends are clear and consistent, significantly reducing the probability of false signals.

-

Multiple Confirmation Mechanisms: The synergy of EMA, MA, and RSI confirmations increases the reliability of trading signals. Particularly, requiring EMA crossovers or price breakouts as trigger conditions enhances entry timing precision.

-

Flexible Risk Management: The strategy offers various risk control options, including ATR-based dynamic stops, fixed percentage stop-loss/take-profit, and trailing stops, allowing traders to adjust risk parameters according to personal risk preferences and market conditions.

-

Volume Confirmation: The addition of increased volume as a condition further filters potential false breakouts, as genuine price movements are typically accompanied by increased trading volume.

-

Visual Interface: The strategy provides an intuitive visual dashboard displaying the status of various indicators and signals, enabling traders to clearly understand current market conditions and strategy assessments at a glance.

-

High Customizability: Almost all parameters of the strategy can be adjusted through input settings, including EMA lengths, MA type, RSI parameters, and risk control multipliers, allowing traders to optimize the strategy for different market environments.

Strategy Risks

-

Sideways Market Risk: In range-bound, consolidating markets, EMA and MA may frequently cross, leading to increased false signals and frequent trading, potentially resulting in consecutive losses. The solution is to add additional filtering conditions, such as volatility assessment or trend strength confirmation, pausing trading when markets are clearly identified as ranging.

-

Parameter Optimization Overfitting: Excessive optimization of indicator parameters may cause the strategy to perform excellently on historical data but fail in future markets. It is recommended to use walk-forward analysis to verify strategy robustness and test a fixed set of parameters across multiple trading instruments.

-

Large Gap Risk: Following major news or sudden events, markets may experience significant gaps, preventing stops from executing at preset levels. Consider using more conservative position sizing or implementing volatility-based position adjustment mechanisms.

-

Limitations of Reliance on Quantitative Indicators: The strategy completely relies on technical indicators, ignoring fundamental factors. Before major economic data releases or central bank policy changes, consider reducing position size or pausing trading to avoid risks from sudden news.

-

Signal Lag: EMA, MA, and other indicators are inherently lagging, potentially generating signals when trends are already nearing their end. This can be improved by adjusting EMA periods or incorporating other forward-looking indicators (such as price patterns or volatility changes).

Strategy Optimization Directions

-

Market Environment Filtering: Introduce adaptive indicators or market structure assessment to identify whether the current market is trending or ranging before strategy execution, adjusting trading parameters or pausing trading accordingly. For example, using ADX (Average Directional Index) to quantify trend strength and only trading when trends are clear.

-

Dynamic Parameter Adjustment: The current strategy uses fixed technical indicator parameters; consider automatically adjusting parameters based on market volatility. For example, using shorter-period EMAs to quickly capture movements in low-volatility environments and longer-period EMAs to reduce noise in high-volatility environments.

-

Position Sizing Optimization: The current strategy uses fixed percentage money management; this could be improved to dynamic position sizing based on volatility, expected win rate, or Kelly formula to maximize risk-adjusted returns.

-

Machine Learning Integration: Introduce machine learning algorithms, such as decision trees or random forests, to optimize weight allocation to various indicators or predict which market environments the strategy might perform better in.

-

Fundamental Filtering: Automatically adjust stop-loss ranges or pause trading before important economic data releases to address potential high-volatility events.

-

Multi-Timeframe Weight Optimization: The current strategy simply requires confirmation from two timeframes; consider introducing a more complex multi-timeframe weighting system, assigning different weights to different timeframes to form a comprehensive score for determining entry timing.

-

Seasonal Analysis Addition: Some trading instruments may exhibit temporal seasonal characteristics; analyze historical data to mine these patterns and adjust strategy parameters or trading periods accordingly.

Summary

The Multi-Timeframe Momentum Convergence Trading System is a structurally complete, logically clear quantitative trading system that effectively filters market noise and captures high-probability trading opportunities through multi-timeframe analysis and multi-indicator confirmation. The strategy integrates classic technical analysis indicators EMA, MA, and RSI, and enhances trading quality through precise entry requirements and a comprehensive risk management system.

The strategy's greatest advantage lies in its multiple confirmation mechanisms and multi-timeframe collaborative analysis, which not only reduces false signals but also ensures trades align with the primary trend. Meanwhile, comprehensive risk management options allow traders to flexibly control risk exposure. However, the strategy also faces risks including poor performance in ranging markets, parameter optimization overfitting, and technical indicator lag.

Future optimization directions primarily focus on market environment classification, dynamic parameter adjustment, machine learning applications, and integration of additional temporal dimension analyses. Through these optimizations, the strategy has the potential to maintain stable performance across different market environments, further improving win rates and risk-adjusted returns.

For traders seeking systematic, disciplined trading methods, this strategy provides a solid framework that can be either directly applied or customized and extended as the foundation for a personalized trading system.

- 1