Early Morning Range Breakout Quantitative Trading Strategy

Overview

The Early Morning Range Breakout Quantitative Trading Strategy is an intraday trading system based on price range breakout principles. The core concept of this strategy is to capture the price range formed during the first five minutes after market opening (9:15-9:19) and generate trading signals when the price breaks through this range. The strategy design takes full advantage of the short-term price fluctuation range that typically forms during the early market session and uses it as a reference benchmark for subsequent price movements. By entering positions at range breakouts, the strategy aims to capture potential intraday trend movements.

Strategy Principle

The working principle of this strategy is based on the following key steps:

- Data Collection Phase: The strategy precisely records the high and low points of each one-minute candle from 9:15 to 9:19.

- Range Calculation Phase: At 9:20, the system automatically calculates the highest high and lowest low formed by the previous five-minute candles, thus establishing the price fluctuation range.

- Signal Generation Phase: When the price breaks above the highest point of the range, the system generates a long signal; when the price breaks below the lowest point, the system generates a short signal.

- Trade Execution Phase: Based on the generated signals, the system automatically executes the corresponding buy or sell operations.

- End-of-Day Reset Phase: At the end of each trading day, the system resets all variables to prepare for the next trading day.

In terms of technical implementation, the strategy employs precise time control logic to ensure data is collected and trading signals are generated only within specific time periods. Through conditional judgments and variable recording, the strategy can accurately identify price breakout behaviors and trigger corresponding trading operations.

Strategy Advantages

The Early Morning Range Breakout Quantitative Trading Strategy has the following significant advantages:

- Clear Trading Rules: The strategy is based on objective price range breakout rules, making trading standards objective and the decision-making process free from subjective influence.

- Capturing Short-term Trends: By identifying breakouts of the early morning price range, the strategy can promptly capture potential intraday short-term trends.

- Adaptation to Market Structure: The strategy is particularly suitable for markets with distinct opening ranges followed by trending developments.

- Automated Execution: Fully automated trading logic reduces human intervention, avoiding the negative impacts of emotional trading.

- High Flexibility: Through parameter adjustments (such as enabling/disabling strategy execution, debug mode, etc.), the strategy can flexibly respond to different market environments.

- Clear Visual Feedback: The strategy provides an intuitive graphical interface, including range lines, trade signal markers, and debug information, facilitating strategy execution monitoring.

Strategy Risks

Despite its many advantages, the Early Morning Range Breakout Quantitative Trading Strategy still has the following potential risks:

- False Breakout Risk: The market may exhibit brief breakouts followed by quick retracements, leading to incorrect signals and unnecessary trading losses.

- Range Quality Risk: If the early morning price range is too narrow, it may lead to frequent breakout signals and excessive trading.

- Data Missing Risk: The strategy heavily relies on price data from the first five minutes; missing data may affect the accurate calculation of the range.

- Market Opening Characteristics Risk: Some markets may experience violent fluctuations or insufficient liquidity during opening, affecting the representativeness of the range.

- Single Factor Risk: The strategy relies solely on price breakouts as a single factor, lacking auxiliary judgment from other technical indicators or fundamental factors.

To address these risks, consider the following solutions:

- Add confirmation mechanisms, such as requiring breakout prices to maintain for a certain time or magnitude before triggering trades

- Set dynamic range width thresholds to avoid generating trading signals in overly narrow ranges

- Incorporate data validation mechanisms to ensure complete and reliable data for range calculations

- Introduce other technical indicators as auxiliary filtering conditions to improve signal quality

Strategy Optimization Directions

Based on the analysis of the strategy code, optimization can be pursued in the following directions:

- Add Dynamic Stop-Loss Mechanism: The current strategy lacks explicit stop-loss settings. Adding dynamic stop-loss based on range width or ATR can control single trade risk.

- Introduce Trend Filters: Combine moving averages or other trend indicators to trade in the direction of the major trend, avoiding frequent trading in oscillating markets.

- Optimize Range Calculation Logic: Consider using VWAP or other volume-weighted methods to determine more representative price ranges, rather than simply using the highest and lowest prices.

- Add Time Filtering: Set trading windows to avoid trading during periods of low market volatility or high uncertainty.

- Incorporate Volatility Adjustment: Dynamically adjust the range breakout trigger thresholds based on market volatility, requiring larger breakout magnitudes in high-volatility environments.

- Enhance Backtesting Capabilities: Add more detailed performance statistics and risk assessment metrics for more comprehensive strategy performance evaluation.

- Optimize Code Structure: The current code contains repetitive logic and lengthy conditional judgments. Using arrays and loop structures can simplify the code and improve readability and maintainability.

These optimization directions are important because they can significantly improve the strategy's robustness and adaptability. For example, dynamic stop-loss and trend filtering can reduce false breakout risk and improve risk-reward ratios; range calculation optimization can increase range representativeness and reduce ineffective trades; time filtering and volatility adjustment help the strategy adapt to different market environments.

Summary

The Early Morning Range Breakout Quantitative Trading Strategy is a concise and effective intraday trading system focused on capturing price range breakouts formed after market opening. The strategy precisely records price fluctuations during the first five minutes of the early market session, establishes a reference range, and generates trading signals when prices break through this range. Its core advantages lie in clear trading rules, objective decision-making processes, and automated execution mechanisms.

However, the strategy also faces potential risks such as false breakouts, poor range quality, and dependency on a single factor. By adding stop-loss mechanisms, introducing trend filters, optimizing range calculation logic, and incorporating dynamic parameter adjustments, the robustness and adaptability of the strategy can be significantly enhanced.

For traders interested in using this strategy, it is recommended to first conduct thorough backtesting in different market environments to understand the strategy's performance characteristics in various situations and adjust parameter settings and risk control mechanisms accordingly. Additionally, using this strategy as part of a more comprehensive trading system, combined with other technical analysis tools and risk management principles, will help maximize its effectiveness.

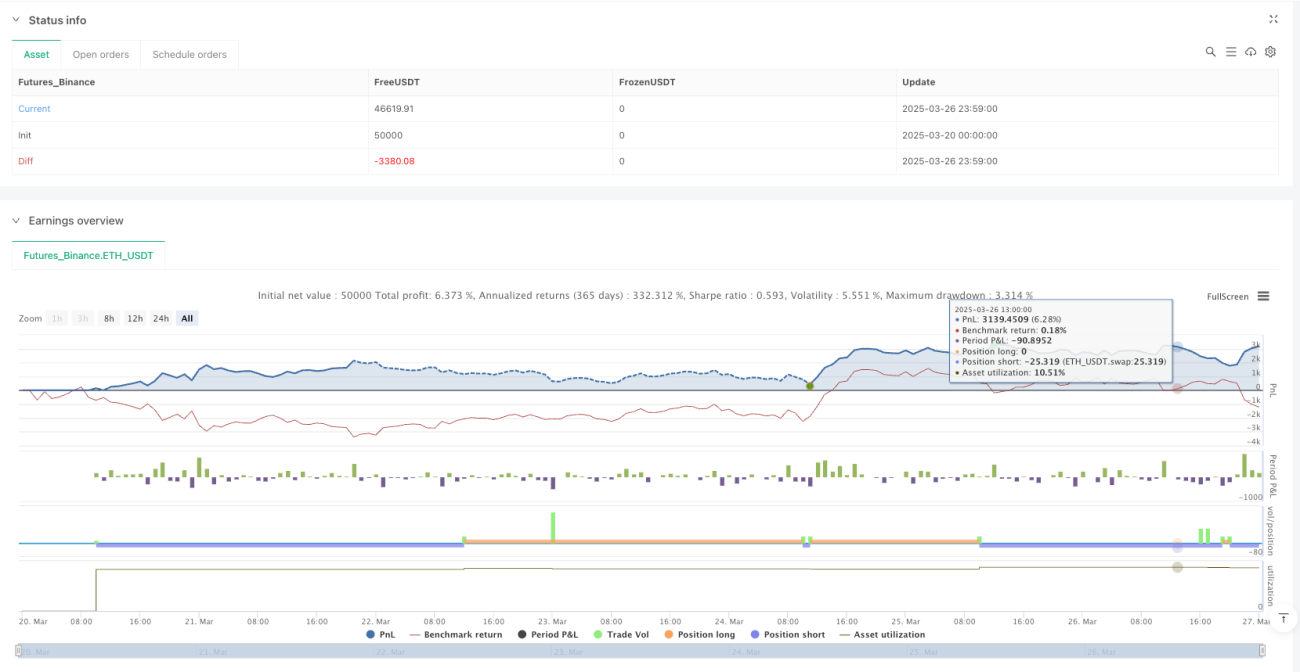

/*backtest

start: 2025-03-20 00:00:00

end: 2025-03-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Morning Range Breakout Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input parameters- 1