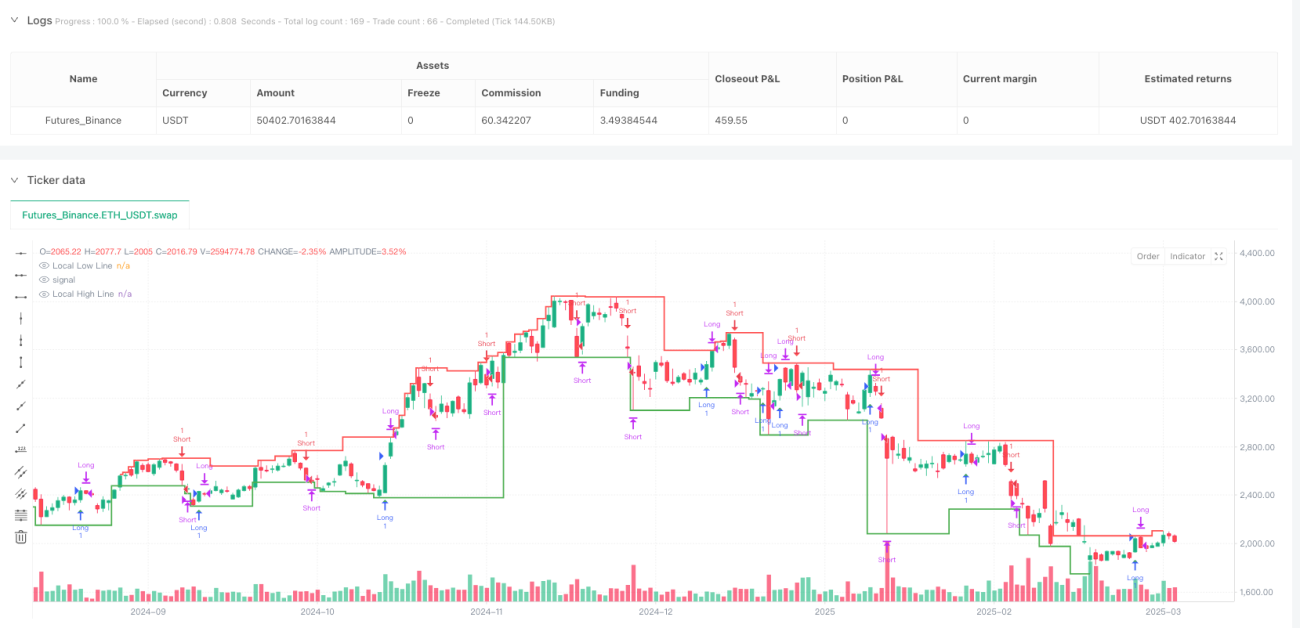

Overview

This is an innovative trading strategy that combines liquidity zone analysis with dynamic internal market structure, aiming to identify high-probability entry points. By tracking price interactions with key market levels and utilizing internal market shifts to trigger trades, the strategy provides traders with a flexible and precise market entry approach.

Strategy Principles

The core logic is based on two key components: liquidity zone identification and internal market shifts. Liquidity zones are dynamically determined by analyzing local highs and lows, while internal market shifts are judged by price breakouts of previous bullish or bearish levels.

The strategy features the following core characteristics:

- Internal Market Shift Logic: Relies on price breakouts of key levels rather than traditional candlestick patterns

- Liquidity Zone Tracking: Dynamically identifies key liquidity zones to prevent trading in weak market conditions

- Mode Flexibility: Offers three trading modes - "Both", "Bullish Only", and "Bearish Only"

- Risk Management: Customizable stop-loss and take-profit levels

- Time Range Control: Precise control of trading time periods

Strategy Advantages

- Dynamic Adaptability: Quickly responds to market structure changes

- Precise Entry: Enhances entry accuracy by combining liquidity zones and internal market shifts

- Controllable Risk: Built-in stop-loss and take-profit mechanisms

- High Flexibility: Can choose trading modes based on different market conditions

- Multi-Dimensional Analysis: Simultaneously considers price behavior, liquidity, and market structure

Strategy Risks

- Extreme market volatility may trigger stop-losses

- Frequent signals in range-bound markets may increase trading costs

- Improper parameter settings may affect strategy performance

- Potential discrepancies between backtesting and live trading results

Strategy Optimization Directions

- Introduce machine learning algorithms for parameter adaptive optimization

- Add more filtering conditions, such as trading volume and volatility indicators

- Develop multi-timeframe verification mechanisms

- Optimize stop-loss and take-profit algorithms with dynamic market volatility adjustments

Summary

This is an innovative trading strategy that integrates liquidity analysis and market structure dynamics. By providing flexible internal market shift logic and precise liquidity zone tracking, it offers traders a powerful trading tool. The strategy's key strength lies in its adaptability and multi-dimensional analysis capabilities, maintaining high execution efficiency across different market conditions.

- 1