Overview

The Multi-band Price Reversal Identification Strategy is a price structure-based trading approach that relies on the "Horn Pattern" to capture short-term reversal opportunities in the market. The strategy integrates pattern recognition, trend filtering, and volatility confirmation across three dimensions, identifying specific three-bar combinations and triggering trade signals when the fourth bar (confirmation bar) meets certain conditions. The strategy employs EMA20 as the primary trend filter to ensure trade direction aligns with the medium-term trend, while using the ATR indicator to filter low volatility environments, effectively improving trade quality.

Strategy Principles

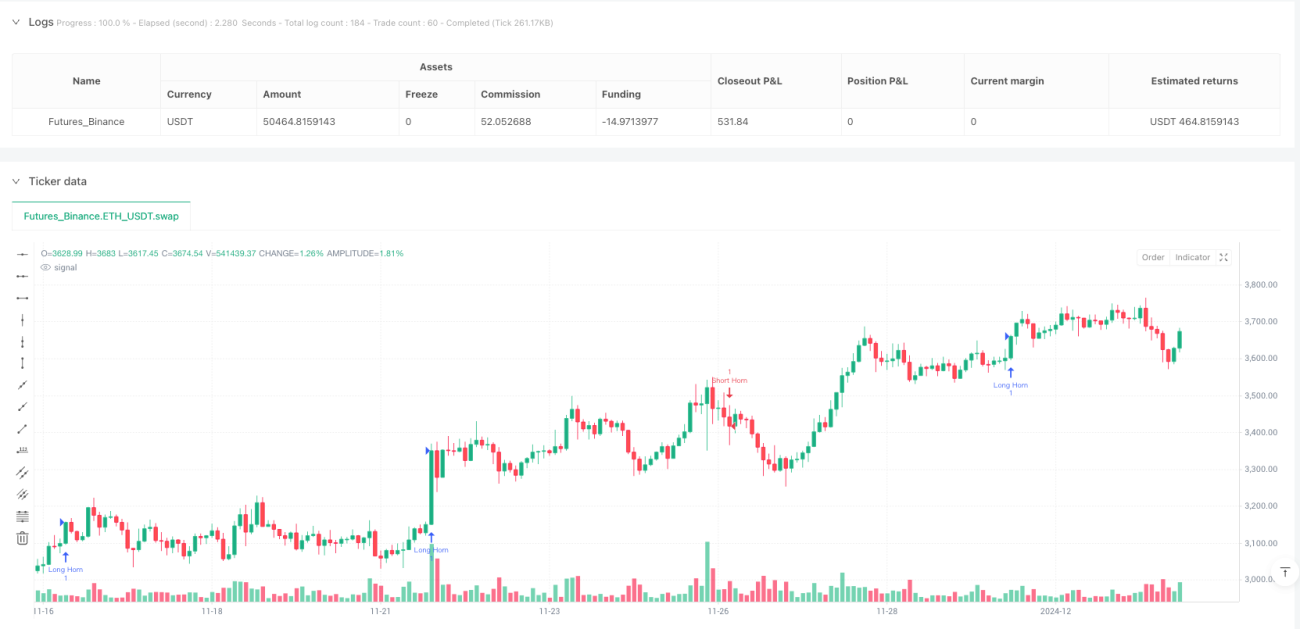

The core principle of this strategy is based on the "Horn Pattern" in price structure, which is a specific price pattern formed by three bars:

-

Bullish Horn Pattern:

- Requires the middle bar (bar[2]) to have a low higher than the lows of the bars on either side

- The first and third bars must be bullish (closing price higher than opening price)

- Forms a "low-higher low-low" W-shaped structure

-

Bearish Horn Pattern:

- Requires the middle bar to have a high lower than the highs of the bars on either side

- The first and third bars must be bearish (closing price lower than opening price)

- Forms a "high-lower high-high" M-shaped structure

-

Confirmation Conditions:

- Bullish signal: The fourth bar (confirmation bar) must close above the highest point of the previous three bars and be bullish

- Bearish signal: The fourth bar must close below the lowest point of the previous three bars and be bearish

-

Filtering Conditions:

- Trend filter: Bullish signals require the confirmation bar to close above EMA20, bearish signals require it to close below EMA20

- Volatility filter: The confirmation bar or the previous bar's range must be greater than ATR, ensuring avoidance of low volatility environments

The strategy employs precise entry price settings and risk management methods: bullish entries are placed one tick above the confirmation bar's closing price, while bearish entries are placed one tick below. Stop losses are set at the structural extreme of the Horn pattern (lowest point minus one tick for longs, highest point plus one tick for shorts), with profit targets at 1R (risk-reward ratio of 1:1).

Strategy Advantages

-

Structured Trading Logic: The strategy is based on clear price structures and pattern recognition, reducing subjective judgment and improving trading consistency and repeatability.

-

Multiple Filtering Mechanisms: Through EMA trend filtering and ATR volatility filtering, signal quality is significantly improved, avoiding erroneous trades in unfavorable market environments.

-

Precise Entry and Risk Management: The strategy sets clear entry points, stop-loss levels, and profit targets, making risk management simple and effective, with predetermined risk for each trade.

-

Visual Assistance: The strategy draws structure lines of the Horn pattern, entry price lines, and target price lines on the chart, helping traders intuitively understand trading logic and price movements.

-

Strong Adaptability: The strategy is applicable to multiple timeframes (5-minute to 1-hour) and high-volatility instruments, offering a wide range of application scenarios.

-

Parameter Adjustability: Key parameters such as EMA length, ATR length, and volatility threshold can be adjusted according to different market conditions and personal preferences, enhancing strategy flexibility.

Strategy Risks

-

False Breakout Risk: In highly volatile markets, prices may form false breakouts, triggering signals before quickly reversing, leading to stop-losses being hit. The solution is to add additional confirmation indicators or adjust entry timing, such as waiting for pullbacks before entering.

-

Trend Transition Point Uncertainty: Near trend transition points, EMA filtering may cause missed initial reversal signals. Consider adding other trend identification tools or setting more sensitive EMA parameters to mitigate this issue.

-

Low Liquidity Environment Risk: In low liquidity environments, slippage may cause actual entry prices to deviate from ideal prices, affecting risk-reward ratios. It is recommended to use this strategy with highly liquid instruments or during main trading sessions.

-

Parameter Sensitivity: The choice of EMA and ATR parameters significantly impacts strategy performance, with different market environments potentially requiring different parameter settings. It is advisable to optimize parameters through backtesting under various market conditions.

-

Consecutive Loss Risk: Any trading strategy can experience consecutive losses, requiring reasonable money management to control single trade risk and avoid significant equity curve drawdowns.

Strategy Optimization Directions

-

Multiple Timeframe Confirmation: Introduce higher timeframe trend confirmation mechanisms, executing trades only when higher timeframe trend direction is consistent, improving signal quality. This can be implemented by adding longer-period EMAs or other trend indicators.

-

Dynamic Profit Target Mechanism: The current strategy uses a fixed 1R profit target; consider introducing dynamic profit target mechanisms, such as trailing stops or ATR-based dynamic profit targets, to capture more profit in strong trends.

-

Volatility Adaptability: The current strategy uses a fixed ATR threshold to filter low volatility environments; consider implementing a volatility adaptive mechanism that automatically adjusts thresholds based on recent market volatility characteristics.

-

Entry Optimization: Consider adding pullback entry logic, waiting for minor retracements after confirmation signals before entering, potentially achieving better entry prices and risk-reward ratios.

-

Price Action Confirmation: On top of the basic Horn pattern, add price action confirmation factors, such as volume confirmation, candlestick pattern confirmation, etc., to further improve signal quality.

-

Machine Learning Integration: Consider introducing machine learning algorithms to train models through historical data to identify Horn patterns most likely to succeed, achieving intelligent filtering of signal quality.

Summary

The Multi-band Price Reversal Identification Strategy is a trading system that combines price structure recognition, trend filtering, and volatility confirmation, capturing specific Horn pattern reversal signals and executing trades in alignment with medium-term trends. The strategy's advantages lie in its clear structured trading logic, precise risk management, and multiple filtering mechanisms, suitable for medium to short-term traders capturing reversal opportunities in the market.

Strategy risks mainly come from false breakouts, uncertainty at trend transition points, and parameter sensitivity, but these risks can be effectively managed through additional confirmation mechanisms, parameter optimization, and improved money management. Future optimization directions include multiple timeframe confirmation, dynamic profit target mechanisms, volatility adaptability, and machine learning integration, which are expected to further enhance the strategy's robustness and profitability.

Overall, this strategy provides traders with a systematic, quantifiable method to identify and trade price reversals, and with reasonable risk management and continuous optimization, it has the potential to become an effective tool in a trader's toolbox.

- 1