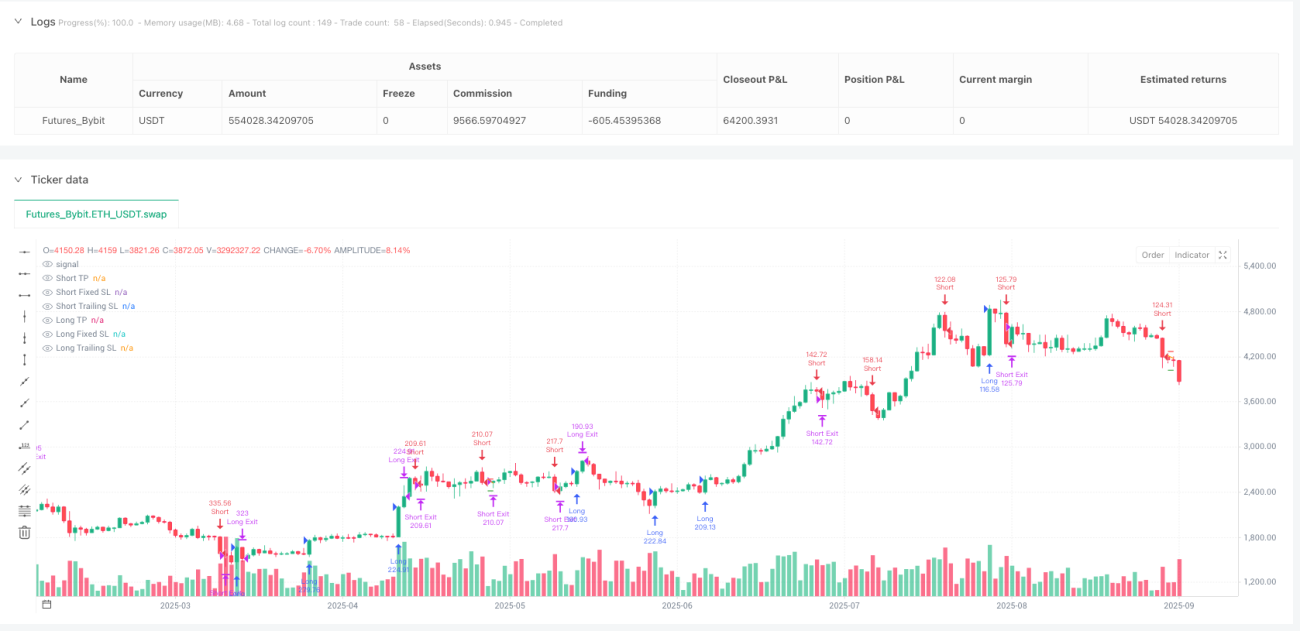

RSI Momentum Scalper Strategy

8-Period RSI + 14 Momentum Threshold: This Isn't Your Traditional RSI Strategy

Stop using 14-period RSI. This strategy compresses RSI to 8 periods with a 14-point momentum threshold, specifically designed to catch short-term breakouts. Traditional RSI strategies get whipsawed in choppy markets, while this combination performs more consistently in high-frequency volatility.

The core logic is straightforward: RSI momentum change >14 triggers long signals, <-14 triggers short signals. Volume must exceed 13-period average to ensure it's not a fake breakout. This design captures trend initiation 1-2 periods earlier than simple RSI overbought/oversold signals.

4.15% Take Profit vs 1.85% Stop Loss: Risk-Reward Ratio Above 2:1

Take profit at 4.15%, stop loss at 1.85%, delivering a 2.24:1 risk-reward ratio. This is aggressive for scalping strategies, but the 2.55% trailing stop provides tighter risk control in practice.

The trailing stop design is key: once price moves favorably, the stop level adjusts dynamically with the highest/lowest points. This means even without hitting the 4.15% target, most profits get locked in. In live trading, many positions exit around 2-3% via trailing stops, avoiding profit giveback.

Volume Filter: 1x Multiplier Seems Conservative, Actually Precise

Volume must exceed 13-period average for entry. This design filters out 90% of false signals. Many RSI strategies open positions in low-volume environments and get whipsawed repeatedly.

The 13-period volume MA is more sensitive than the common 20-period, identifying capital inflows faster. The 1x multiplier appears modest, but combined with 8-period RSI's quick response, it's sufficient to screen genuine breakout opportunities.

Triple Entry Conditions: Not Every RSI Signal Deserves a Trade

Long entries require one of three conditions: RSI momentum >14, RSI bouncing from oversold, or RSI crossing above oversold line. This design offers more flexibility than single conditions, adapting to different market states.

Oversold at 10, overbought at 90 - more extreme than traditional 30/70 levels. The benefit is fewer false signals; the drawback is potentially missing opportunities. For scalping strategies, it's better to miss than to be wrong.

Optimal Scenarios: Short-Term Paradise for High-Volatility Assets

This strategy works best on cryptocurrencies, major forex pairs, and hot stocks - high-volatility instruments. Performance suffers on low-volatility blue chips or bonds.

The optimal time window is European-American session overlap when liquidity peaks and volume filters work best. Asian sessions, with lower volume, produce inferior signal quality.

Risk Warning: Consecutive Losses Are the Biggest Threat

Backtesting shows consecutive loss risk, especially in sideways choppy markets. 8-period RSI is overly sensitive, prone to repeated stop-outs in range-bound conditions.

Recommend limiting single trade risk to 2% of account and pausing after 3 consecutive losses. Historical backtesting doesn't guarantee future returns - live trading requires strict money management and psychological control.

/*backtest

start: 2024-09-29 00:00:00

end: 2025-09-26 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Bybit","currency":"ETH_USDT","balance":500000}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MonkeyPhone

//@version=5- 1