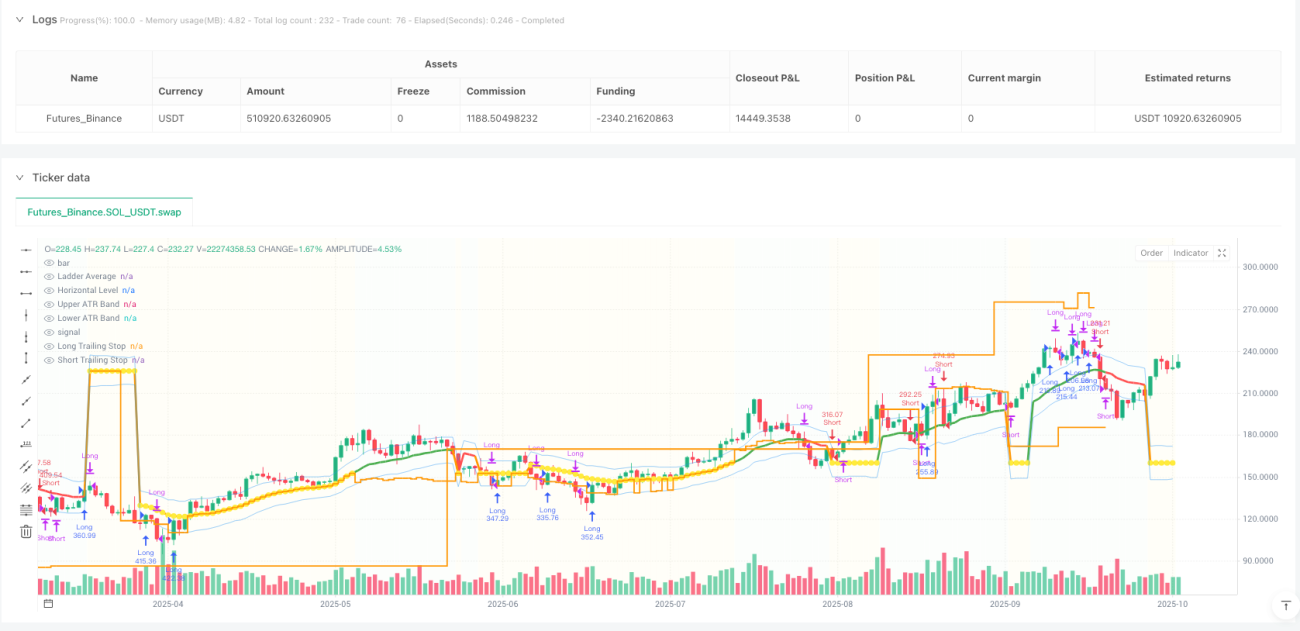

Trend Ladder Average Strategy: How to Gracefully "Lie Flat" During Sideways Markets?

Why Do Traditional Trend-Following Strategies Frequently "Crash" in Choppy Markets?

As a quantitative trading practitioner, I'm often asked this question: Why do strategies that perform excellently in trending markets start experiencing significant drawdowns once choppy conditions emerge?

The answer is actually quite simple: Most trend-following strategies suffer from "trend obsession" - they always try to maintain high-frequency trading in any market environment, ignoring a fundamental fact: markets spend 70% of their time in sideways consolidation.

The "Trend Ladder Average Strategy" we're analyzing today addresses this pain point with an interesting solution: actively track in trending markets, "gracefully lie flat" in choppy markets.

What is "Ladder Average"? How Does This Concept Redefine Trend Following?

Traditional moving average strategies have a fatal flaw: they're always changing. Whether the market is in a strong trend or sideways consolidation, moving averages constantly adjust with price fluctuations, leading to numerous false signals.

The core idea of "Ladder Average" is: let the moving average "freeze" under specific conditions.

The specific implementation logic is as follows:

-

Trend State Detection: Use ADX indicator to judge market trend strength

- ADX > 25: Strong trending market

- Moving average slope < 0.3%: Sideways market

-

Dynamic Moving Average Switching:

- Strong trend: Normal EMA(21) tracking

- Sideways: Moving average "freezes" at horizontal position, forming support/resistance

The brilliance of this design lies in: it makes the strategy exhibit different "personalities" in different market environments - sensitive during trends, steady during consolidation.

How to Implement the "Trend Catching" System?

Besides the basic ladder average mechanism, this strategy also integrates a "trend catching" module, which I consider the most innovative part:

Quick Reversal Mechanism:

- When a strong counter-trend emerges right after closing a position

- Quickly establish new positions within 3 periods

- Conditions: ADX > 30 and DI+/DI- difference > 10

This design solves an important problem with traditional strategies: how to quickly adjust positions during early trend reversals.

Imagine this scenario: you just closed a long position due to stop loss, and the market immediately shows a strong downward trend. Traditional strategies might need to wait for new signal confirmation, but this "trend catching" system can quickly establish short positions within 3 periods.

Risk Management: Why Differentiate Market States?

The most valuable aspect of this strategy is its differentiated risk management mechanism:

Risk Control in Sideways Markets:

- Adjust stop loss near ladder average

- Reduce ATR multiplier, tighten stops

- Set more conservative profit targets

Risk Control in Trending Markets:

- Use standard ATR multiplier stops

- Enable ladder-style trailing stops

- Allow larger price fluctuation space

This design reflects an important trading philosophy: different market environments require different risk preferences. In sideways markets, we should be more cautious; in trending markets, we need to give profits more room to run.

Ladder Trailing Stop: How to Balance Profit Protection with Trend Following?

Traditional trailing stops are often too mechanical - either too tight causing premature exits, or too loose failing to effectively protect profits. This strategy's ladder trailing stop provides a more intelligent solution:

Ladder Setup Logic:

- Dynamically calculate ladder spacing based on ATR

- Set maximum of 5 ladder levels

- Adjust stop loss accordingly when each ladder is breached

The advantage of this design: it can protect profits while giving trends sufficient development space.

What Should You Pay Attention to in Practical Application?

Based on my live trading experience, using this type of strategy requires attention to the following points:

-

Parameter Optimization Trap: Don't over-optimize ADX thresholds; values between 25-30 perform stably in most markets

-

Market Adaptability: This strategy is more suitable for moderately volatile markets; in extreme volatility environments, ATR multipliers may need adjustment

-

Money Management: Recommend single position size not exceeding 10% of total capital, especially when trend catching is enabled

-

Backtesting Trap: Pay special attention to slippage and commission impacts, particularly frequent trading in choppy markets

Where is the Innovation Value of This Strategy?

From the perspective of quantitative strategy development, this strategy represents an important evolutionary direction: transition from single logic to multi-state adaptive systems.

Traditional strategies often try to use one fixed logic for all market conditions, while this strategy demonstrates "local adaptation" wisdom:

- Behaves like an aggressive trend follower in trending markets

- Behaves like a conservative range trader in choppy markets

This design approach has important implications for strategy developers: we should give strategies "market perception" capabilities rather than blindly executing fixed logic.

Finally, it's important to emphasize that no strategy is omnipotent. While this ladder average strategy is theoretically elegant, it still needs to be adjusted according to specific market environments and personal risk preferences in practical application. Remember, the best strategy is always the one that suits you best.

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1