🎯 What's This Amazing Strategy? 20 Indicators Working Together!

Did you know? This strategy is like having a super intelligent AI assistant for your trading! It simultaneously monitors 20 different market signals and only gives you trading advice when most indicators say "go". It's like buying a house - you check location, price, layout, transportation... only when everything looks good do you make the move!

Key point! This isn't your ordinary single-indicator strategy, but a "multi-dimensional confluence system". Imagine if only one friend recommended a stock, you might be skeptical; but if 20 professional friends all say it's good, wouldn't you be more confident?

📊 Core Arsenal Revealed

Trend Identification Triple Threat 🗡️

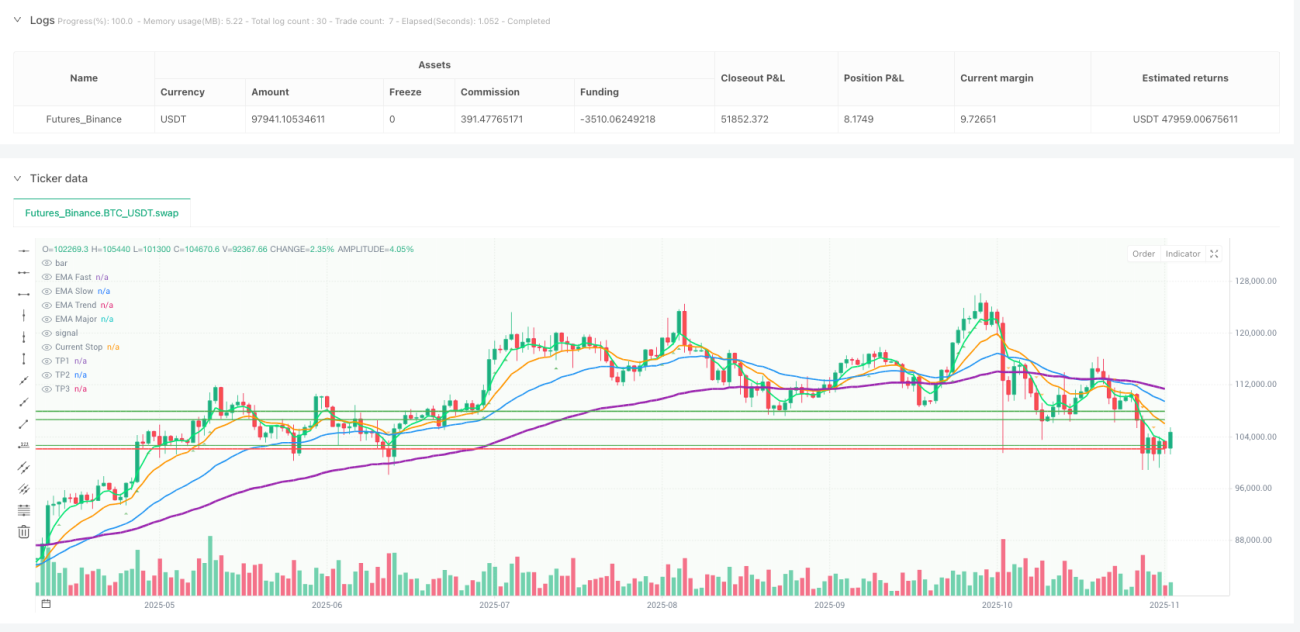

- Fast EMA(5) vs Slow EMA(13): Catches short-term trend reversals

- Trend Filter EMA(34): Confirms medium-term direction

- Major Trend EMA(89): Captures the big picture, avoiding small noise

Multi-Timeframe Analysis ⏰

This feature is awesome! The strategy looks at both 1-hour and 4-hour trends simultaneously, like driving where you watch both the road ahead and your GPS route. Avoids the awkward situation of "short timeframe bullish, long timeframe bearish"!

Smart Risk Management 🛡️

- Dynamic position sizing: Auto-adjusts bet size based on market volatility

- Partial profit taking: Don't be greedy, secure some profits

- Trailing stops: The profit protection hero

🔥 20-Layer Protection Trading Logic

Long Signal Requirements:

- Upward trend: All EMAs in bullish alignment

- Sufficient momentum: RSI, MACD, Stochastic RSI all green-light

- Volume confirmation: Rising volume confirms real moves

- Healthy market structure: Higher highs pattern

- Liquidity support: Key support levels intact

Short signals work in reverse!

Pitfall Alert ⚠️: The strategy includes "Bollinger Band squeeze detection" - when markets are too quiet, it pauses trading to avoid getting whipsawed in choppy conditions!

💰 Profit Maximization Secret Weapons

Staged Profit Taking Strategy 📈

- First take profit: Sell 30% at 2x risk-reward

- Second take profit: Sell another 40% at 3.5x

- Remaining position: Protected by trailing stops, let profits run

Smart Stop Loss Upgrade 🎯

After reaching 2.5x profit, stops automatically move to breakeven, ensuring this trade at least doesn't lose money. Like buying insurance for your profits!

Dynamic Trailing Stops 🏃♂️

When profits reach certain levels, stops follow price like a shadow, protecting gains while leaving room for further upside.

🚀 Why This Strategy Rocks?

- Complete Coverage: Technical analysis, money management, risk control - nothing missing

- Smart Filtering: 20 conditions layer by layer, dramatically improving success rates

- Highly Adaptive: Multi-timeframe analysis suits different market environments

- User-Friendly Design: Automated execution avoids emotional trading

This strategy is like having an experienced trading team coded into software, working 24/7 to find the best trading opportunities for you!

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1