Trendshift [CHE] Strategy

🎯 What Does This Strategy Actually Do?

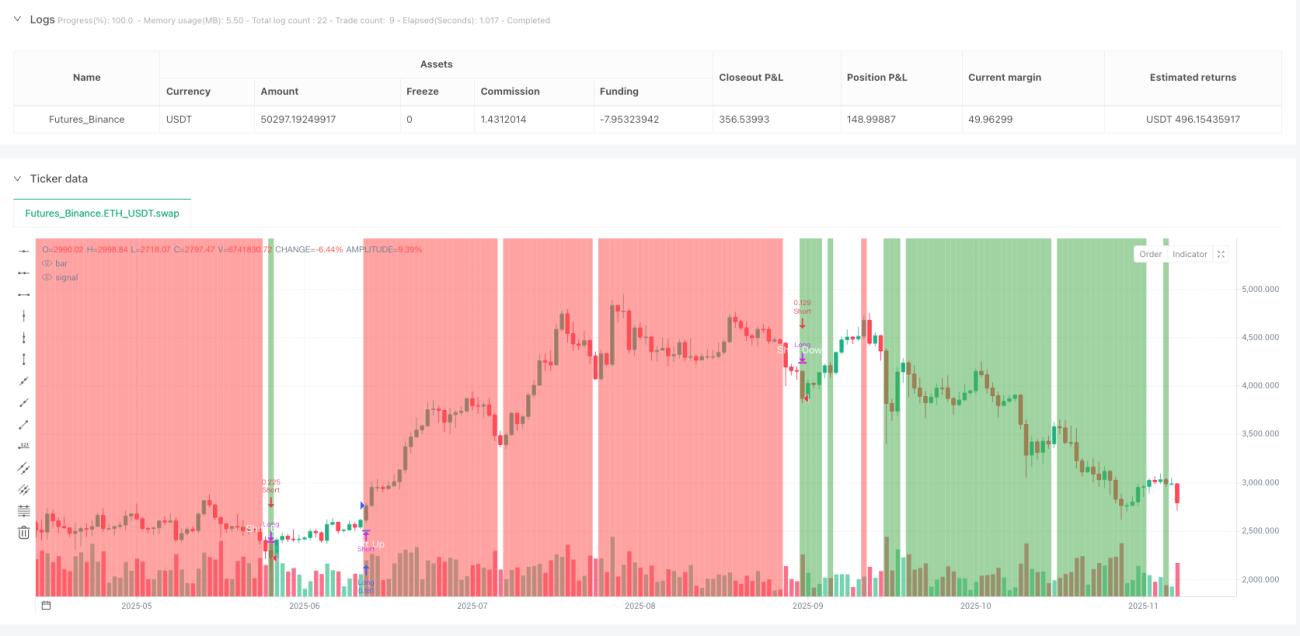

You know what? This strategy is like a "mood detector" for the market! 📊 It specializes in catching those pivotal turning points that catch retail traders off guard. Imagine if you could know in advance when prices are about to "change face" - wouldn't that be like having trading superpowers?

The core idea is super simple: when price breaks through important highs or lows, market structure shifts. It's like climbing a mountain and suddenly realizing the path ahead goes downhill - trend changes often happen in that instant!

🔍 Key Point! Three Core Mechanisms

1. Swing Point Identification System 🎢

The strategy automatically finds important highs and lows from past periods, essentially drawing "peaks" and "valleys" for the market. When price breaks through these key levels, it signals potential trend changes!

2. ATR Filter 📏

Here's the brilliant design! The strategy won't be fooled by minor fluctuations - breakouts must exceed a certain ATR multiple to be valid. It's like setting a "minimum threshold" to filter out false breakouts.

3. Premium/Discount Zone Framework 💎

Here's the most interesting part! The strategy divides price ranges into "cheap zones" and "expensive zones." Buy in cheap zones, sell in expensive zones - isn't this the golden rule of investing?

🚀 What Are the Practical Advantages?

Pitfall Avoidance Guide #1: Say goodbye to chasing highs and selling lows! This strategy enters at the first sign of trend reversal, making you "smart money" instead of a "bag holder."

Pitfall Avoidance Guide #2: Risk control is super thoughtful! It can automatically calculate position sizes based on account percentage and set zone-based stop losses, letting you sleep peacefully.

Pitfall Avoidance Guide #3: Visualization is amazing! Charts automatically mark turning points, and backgrounds change color to indicate whether you're in cheap or expensive zones - crystal clear!

💡 What Type of Trader Is This For?

If you're the type who likes to "buy low, sell high" but always struggles with timing, this strategy is practically tailor-made for you! It's especially suitable for medium to long-term traders because it focuses on fundamental market structure changes, not short-term noise.

Remember, the best strategy isn't one that makes you trade every day, but one that helps you do the right thing at the right time! 🎯

- 1