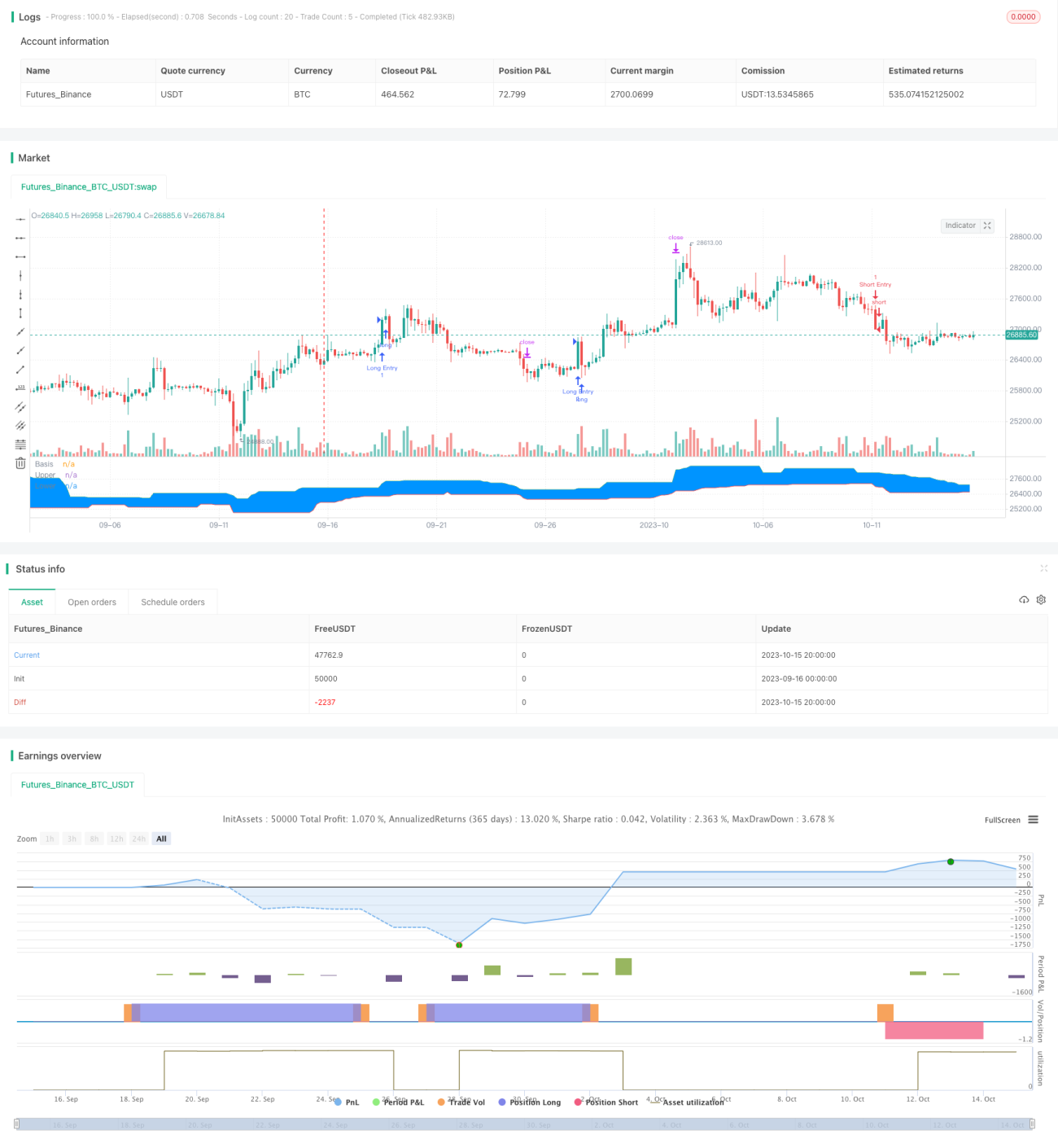

Estrategia de ruptura con seguimiento

Resumen

Esta estrategia implementa principalmente una estrategia de trading de ruptura con seguimiento mediante el indicador "Canal de Donchian". Combina las ideas de tendencia y ruptura, basándose en el juicio de la tendencia a largo plazo para buscar puntos de ruptura en ciclos más cortos para entrar, logrando operaciones a favor de la tendencia en mercados con tendencia. Además, la estrategia establece niveles de stop loss y take profit para controlar la relación riesgo-beneficio de cada operación. En general, la estrategia tiene la ventaja de seguir la tendencia, permitiendo operar en la dirección de la tendencia y aprovechar las oportunidades de tendencias a largo plazo.

Principio de la estrategia

-

Establecer los parámetros del indicador "Canal de Donchian", con un período predeterminado de 20;

-

Establecer la media móvil suavizada exponencial (EMA), con un período predeterminado de 200;

-

Establecer la relación riesgo-beneficio, con un valor predeterminado de 1,5;

-

Establecer los parámetros de retroceso tras la ruptura, para posiciones largas y cortas respectivamente;

-

Registrar si la última ruptura fue un máximo o un mínimo;

-

Señal larga: si la última ruptura fue un mínimo, y el precio está por encima de la banda superior de Donchian y por encima de la media EMA, se genera una señal larga;

-

Señal corta: si la última ruptura fue un máximo, y el precio está por debajo de la banda inferior de Donchian y por debajo de la media EMA, se genera una señal corta;

-

Al entrar en una posición larga, se establece el stop loss en la banda inferior de Donchian con un retroceso de 5 puntos, y el take profit como la relación riesgo-beneficio multiplicada por la distancia del stop loss;

-

Al entrar en una posición corta, se establece el stop loss en la banda superior de Donchian con un retroceso de 5 puntos, y el take profit como la relación riesgo-beneficio multiplicada por la distancia del stop loss.

De esta manera, la estrategia combina el juicio de tendencia y las operaciones de ruptura, permitiendo operar a favor de la tendencia, capturando oportunidades de ciclos más cortos dentro de una tendencia a largo plazo. Al mismo tiempo, el establecimiento de stop loss y take profit permite controlar la relación riesgo-beneficio de cada operación.

Análisis de ventajas

-

Sigue la tendencia a largo plazo, opera a favor de la tendencia y evita operar en contra de ella.

-

El Canal de Donchian como indicador de largo plazo, combinado con el filtro de la media EMA, puede juzgar bien la dirección de la tendencia.

-

El mecanismo de stop loss y take profit controla el riesgo de cada operación, limitando las posibles pérdidas.

-

La optimización de la relación riesgo-beneficio puede ampliar la relación ganancia-pérdida, buscando rendimientos extraordinarios.

-

Los parámetros de backtesting se pueden ajustar de manera flexible para encontrar la mejor combinación de parámetros para diferentes mercados.

Análisis de riesgos

-

El Canal de Donchian y la media EMA como indicadores de filtro pueden generar señales falsas.

-

Las operaciones de ruptura pueden quedar atrapadas fácilmente, por lo que es necesario identificar claramente el contexto de la tendencia.

-

Las distancias de stop loss y take profit son fijas y no se pueden ajustar según la volatilidad del mercado.

-

El espacio de optimización de parámetros es limitado, y el rendimiento en vivo es difícil de garantizar.

-

El sistema de trading no es resistente a muchos eventos aleatorios; eventos de cisne negro pueden causar grandes pérdidas.

Direcciones de optimización

-

Se puede considerar agregar más indicadores para filtrar, por ejemplo, indicadores osciladores, para mejorar la calidad de las señales.

-

Se puede establecer un stop loss y take profit inteligentes, que se ajusten dinámicamente según la volatilidad del mercado y el indicador ATR.

-

Se pueden utilizar métodos como el aprendizaje automático para probar y optimizar los parámetros, haciéndolos más cercanos al mercado real.

-

Se puede optimizar la lógica de entrada, estableciendo indicadores de volumen o volatilidad como condiciones auxiliares para evitar trampas.

-

Se puede considerar combinarlo con estrategias de seguimiento de tendencias o aprendizaje automático para formar una estrategia híbrida que mejore la estabilidad.

Resumen

Esta estrategia, como una estrategia de ruptura con seguimiento, tiene como idea central operar a favor de la tendencia utilizando la ruptura como señal, bajo la premisa de identificar una tendencia a largo plazo, y establecer stop loss y take profit para controlar el riesgo de cada operación. La estrategia tiene ciertas ventajas, pero también hay espacio para optimización. En general, si se manejan bien los parámetros, la selección del momento de entrada y se complementa con otras técnicas para mejorar, esta estrategia puede convertirse en una estrategia práctica de seguimiento de tendencias. Sin embargo, los inversores deben recordar que ningún sistema de trading puede evitar completamente el riesgo del mercado, por lo que es necesario una buena gestión del riesgo.

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1