Estrategia de trading de oscilación de triple patrón

Resumen

La Estrategia de Trading de Oscilación de Triple Modo es una estrategia de trading a corto plazo basada en la combinación de múltiples indicadores técnicos. Utiliza el indicador SuperTrend, la media mixta SSL y el QQE modificado para generar señales de trading estables. Es adecuada para instrumentos con alta volatilidad, como criptomonedas y acciones, y muestra un buen rendimiento especialmente después de periodos de ruptura.

Principio

Señales de entrada

Entrada en largo:

- El SuperTrend cambia de bajista a alcista.

- El precio de cierre cruza por encima del borde superior de la media mixta SSL.

- El QQE modificado se muestra en azul (alcista).

Entrada en corto:

- El SuperTrend cambia de alcista a bajista.

- El precio de cierre cruza por debajo del borde inferior de la media mixta SSL.

- El QQE modificado se muestra en rojo (bajista).

Señales de salida

Salida de largo: El SuperTrend cambia de alcista a bajista.

Salida de corto: El SuperTrend cambia de bajista a alcista.

Stop loss

Se puede elegir entre un stop loss porcentual, un stop loss basado en ATR o un stop loss basado en el máximo o mínimo reciente.

Take profit

Se puede configurar una relación de recompensa para el take profit, calculando automáticamente el precio de take profit.

Gestión del capital

Opcionalmente, se puede utilizar una lógica de gestión de capital para controlar el tamaño de la posición.

Gráficos

- Se dibujan la línea SuperTrend y el canal de la media mixta SSL.

- Se puede optar por dibujar o no la media móvil EMA.

- Se dibujan las líneas de apertura, stop loss y take profit tanto para largos como para cortos.

- Se dibujan etiquetas de apertura de posiciones largas y cortas.

Ventajas

-

Combinación de múltiples indicadores para señales estables.

Al combinar SuperTrend, la media mixta SSL y el QQE modificado, los diferentes indicadores se validan entre sí, filtrando falsas rupturas y generando señales de trading de alta calidad. -

Adecuada para el trading de oscilación en instrumentos volátiles.

La estrategia adopta un enfoque de corto plazo, enfocándose en capturar movimientos de precios a mediano y corto plazo. El SuperTrend sigue eficazmente la tendencia de precios, mientras que la media mixta SSL identifica claramente los niveles de soporte y resistencia. Ambos trabajan en conjunto para obtener ganancias en mercados oscilantes. -

Múltiples opciones de stop loss y take profit.

El stop loss puede ser porcentual, basado en ATR o en extremos recientes. El take profit permite configurar una relación de recompensa. La gestión de capital puede controlar el tamaño de la posición. El usuario puede combinarlos libremente según las características del instrumento y su tolerancia al riesgo. -

Gráficos claros.

La estrategia dibuja líneas de stop loss y take profit de forma clara y visual. Las marcas de líneas de apertura facilitan la identificación de las señales de trading.

Riesgos y optimización

-

Posibles pequeñas pérdidas.

Debido al trading a corto plazo, no se pueden evitar por completo las pequeñas pérdidas por oscilaciones normales. Se puede ajustar apropiadamente la amplitud del stop loss y optimizar la lógica de gestión de capital. -

Riesgo de falsa ruptura.

Cuando el precio muestra una falsa ruptura, puede generar señales erróneas. Se pueden probar diferentes periodos de EMA para filtrar falsas rupturas, u optimizar los parámetros de los indicadores de identificación de tendencia. -

Riesgo de fallo de los indicadores.

Si los indicadores base fallan, pueden aparecer múltiples señales erróneas. Es necesario verificar periódicamente la efectividad de los indicadores y ajustarlos si se detectan problemas. -

Optimización del período de backtesting.

El período de backtesting actual es fijo y puede no corresponder a los diferentes ciclos del mercado del instrumento. Se recomienda optimizar para que coincida con el período principal de negociación del contrato correspondiente. -

Optimización de la adaptabilidad al instrumento.

Se pueden ajustar los parámetros de la estrategia según las características de los datos de diferentes instrumentos para mejorar la tasa de acierto de largos y cortos. Se recomienda utilizar un método de optimización por pasos para comparar el impacto de diferentes parámetros en la estrategia.

Conclusión

Esta estrategia combina múltiples indicadores para generar señales de trading, filtrando eficazmente las falsas rupturas. Es adecuada para criptomonedas y acciones individuales con alta volatilidad. Además, ofrece múltiples opciones de stop loss y take profit, lo que la hace flexible. En general, la estrategia genera señales de trading estables y puede obtener buenos rendimientos en mercados oscilantes de mediano y corto plazo. Mediante una optimización adicional, se pueden ajustar los parámetros para diferentes instrumentos, mejorando el factor de beneficio de la estrategia. Esta estrategia es un sistema de trading eficiente que merece un estudio en profundidad.

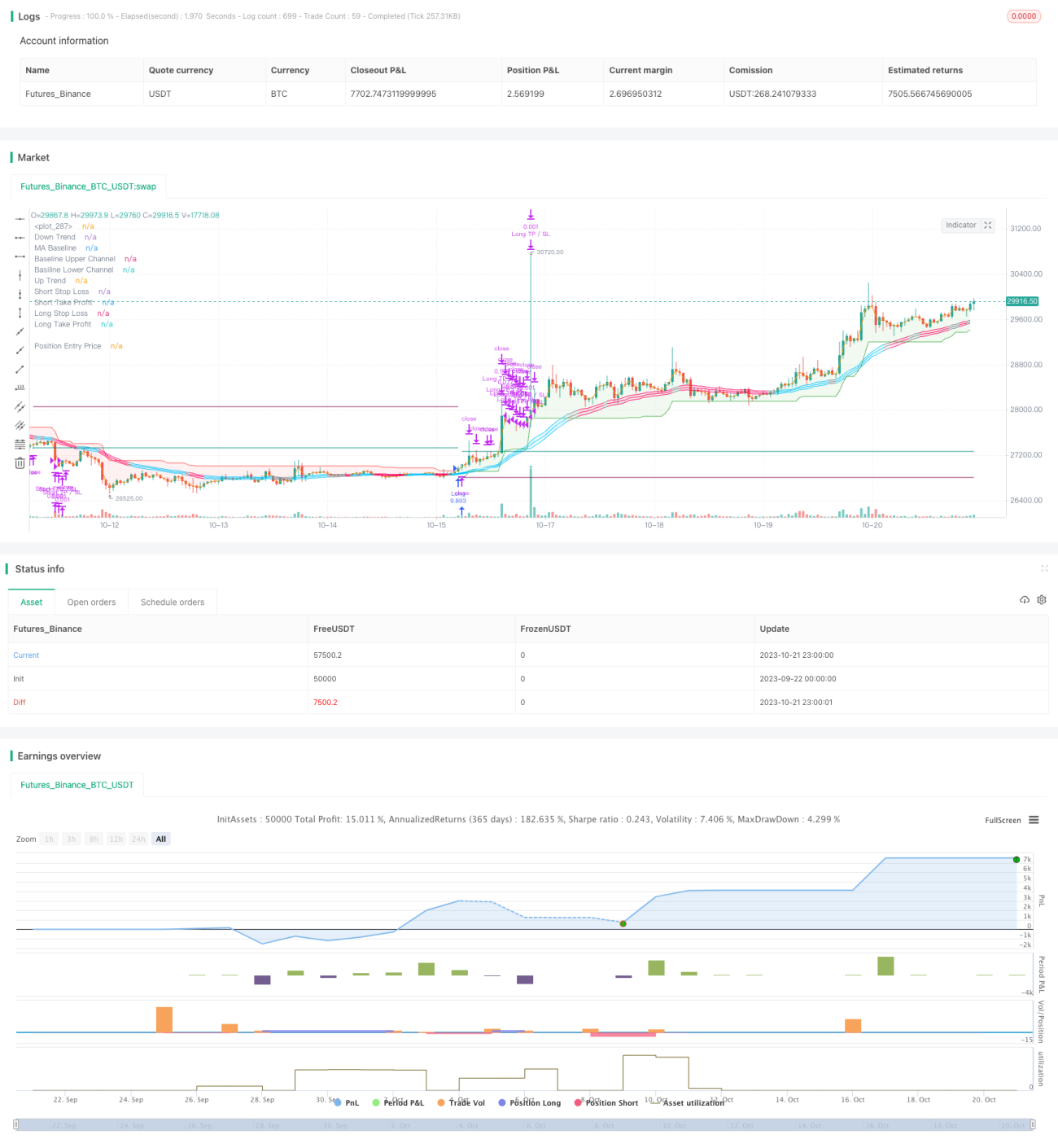

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1