Estrategia de compra en caídas en patrón de corrección

Resumen

Esta estrategia combina el indicador RSI con una media móvil de precios, buscando oportunidades de sobreventa para abrir posiciones largas cuando el precio de la acción cae por debajo de la media móvil. A medida que el precio sigue bajando, la estrategia va añadiendo capas de posiciones según un porcentaje predefinido, con el objetivo de promediar el coste de la posición. Cuando las ganancias de la posición alcanzan el porcentaje de toma de ganancias configurado, la estrategia opta por cerrar la posición. Al mismo tiempo, se introduce un mecanismo progresivo de toma de ganancias que ajusta dinámicamente el precio de toma de ganancias de toda la posición en función de las ganancias ya realizadas por cada lote individual. Esto permite reducir eficazmente el riesgo de pérdidas y lograr una salida gradual.

Principio de la estrategia

-

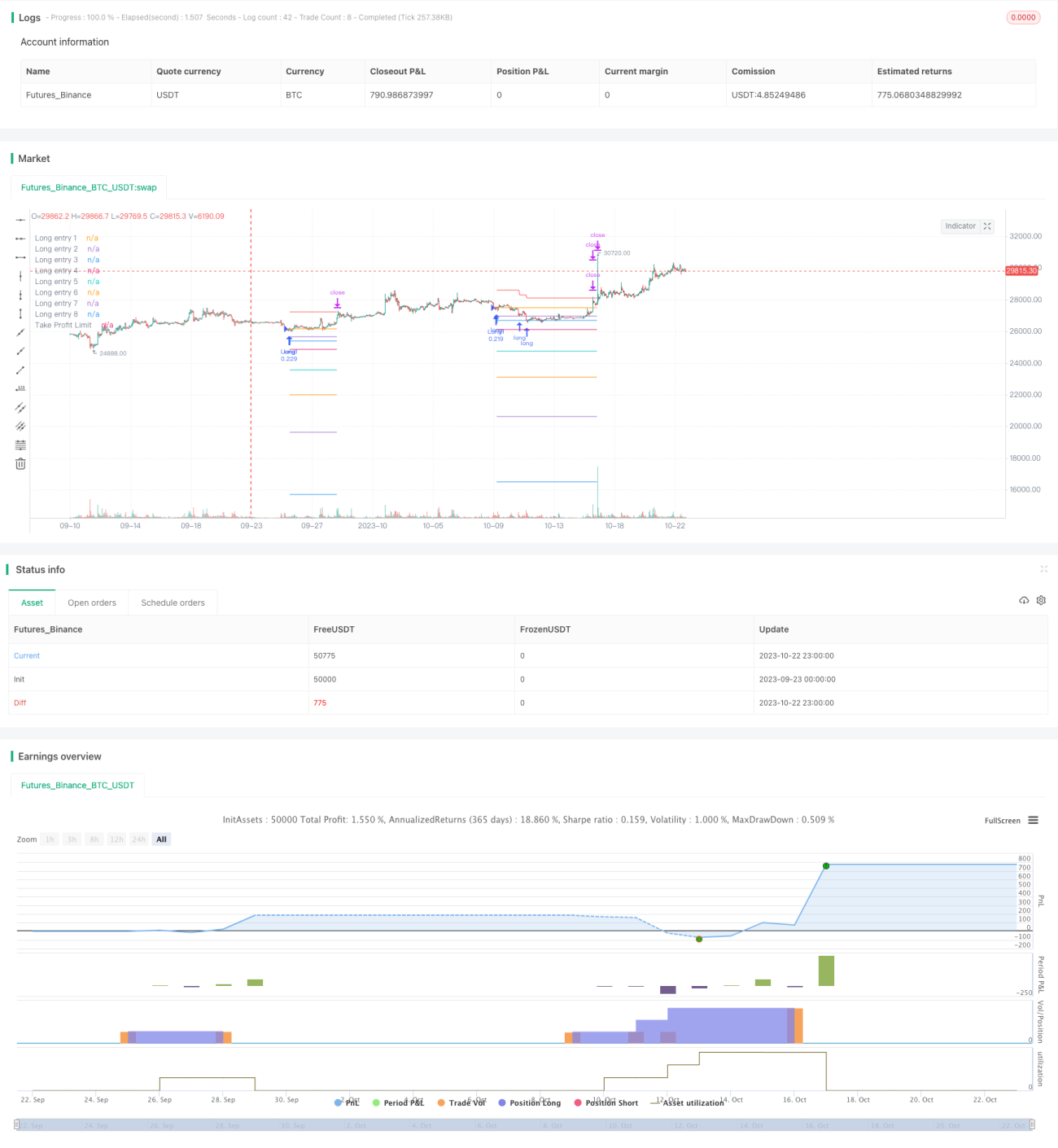

Cuando el RSI está por debajo del nivel de sobreventa de 29 y el precio de cierre está por debajo de la media móvil, se abre la primera posición larga.

-

Cuando el precio cae un 2% respecto a la primera posición, se añade una nueva capa larga; cuando la caída alcanza el 3%, se añade una tercera capa, y así sucesivamente hasta un máximo de 8 adiciones. Esto logra un efecto de construcción de posiciones por lotes.

-

Tras cada apertura, se registra el precio de apertura en ese momento. Estos precios sirven como referencia de entrada y se dibujan como líneas de precio en el gráfico.

-

Después de abrir posiciones, se calcula el precio medio de la cartera. El 3% de ese precio medio se usa como precio de toma de ganancias para cada lote, y el 4% como precio de toma de ganancias para toda la posición.

-

Cuando el precio sube por encima del precio de toma de ganancias de un lote, se cierra ese lote.

-

El cálculo de la toma de ganancias progresiva: cada vez que se cierra un lote, se resta la ganancia realizada de ese lote del precio de toma de ganancias total. Esto hace que la línea de toma de ganancias descienda lentamente, y solo cuando las ganancias de todos los lotes sean suficientes para cubrir la pérdida máxima, se cierran todas las posiciones.

-

Cuando el precio alcanza la línea de toma de ganancias progresiva, se cierran todas las posiciones.

Análisis de ventajas

-

El RSI puede identificar con bastante precisión las zonas de sobreventa, lo que favorece la captura de oportunidades de reversión.

-

La adición de lotes en múltiples ocasiones permite promediar el coste de la posición en los puntos bajos.

-

La toma de ganancias progresiva reduce el riesgo de pérdidas y permite una salida gradual. Incluso en caso de pérdidas, estas pueden controlarse dentro de un rango.

-

Los porcentajes de toma de ganancias y de adición de lotes son configurables, lo que permite ajustar el riesgo de la estrategia según el mercado.

-

La representación en el gráfico de las líneas de referencia de apertura y de toma de ganancias permite una visualización intuitiva de la distribución de las posiciones.

Análisis de riesgos

-

En mercados laterales, puede activar múltiples aperturas y tomas de ganancias, generando un alto número de operaciones y pérdidas por deslizamiento. Se puede ajustar el parámetro del RSI para reducir la frecuencia de operaciones.

-

Una configuración inadecuada del número y el porcentaje de adiciones puede llevar a un exceso de operaciones; se debe configurar con prudencia según el capital disponible.

-

Si el mercado sigue cayendo después de las adiciones, puede enfrentarse a un riesgo de pérdida ilimitada. Se debe establecer un límite máximo de adiciones y un porcentaje conservador para la última capa.

-

Si el porcentaje de toma de ganancias es demasiado pequeño, puede provocar un cierre prematuro. Se debe fijar un porcentaje adecuado basado en datos históricos de backtesting.

Direcciones de optimización

-

Se pueden introducir indicadores como el MACD para filtrar las señales del RSI y reducir operaciones no rentables.

-

Se puede usar el ATR para establecer un stop loss y evitar grandes pérdidas en condiciones extremas del mercado.

-

Se pueden optimizar parámetros como el número de adiciones, el porcentaje de adición y el porcentaje de toma de ganancias para adaptar la estrategia a diferentes instrumentos.

-

Se puede ajustar inteligentemente el porcentaje de toma de ganancias según la volatilidad, relajándolo cuando la volatilidad sea alta.

Resumen

Esta estrategia aprovecha plenamente el RSI para identificar zonas de sobreventa y combina una media móvil para operar en reversiones. Además, utiliza un mecanismo inteligente de adición de lotes y toma de ganancias progresiva para lograr una estrategia larga eficiente controlando el riesgo. Optimizando los parámetros del indicador y el mecanismo de toma de ganancias, la estrategia puede volverse más estable y eficiente. Esta estrategia se puede aplicar ampliamente a instrumentos financieros con características de reversión de tendencia, como futuros de índices bursátiles y criptomonedas, y tiene valor práctico de inversión.

- 1