Estrategia de ruptura con trailing stop loss V2

Resumen

Esta estrategia combina las ventajas de una estrategia de ruptura y una estrategia de trailing stop basada en tendencia, con el objetivo de capturar señales de ruptura de soporte y resistencia en gráficos de largo plazo, mientras utiliza medias móviles para el trailing stop, logrando obtener ganancias en la dirección de la tendencia de largo plazo y controlando el riesgo al mismo tiempo.

Principio de la Estrategia

-

La estrategia primero calcula varios conjuntos de medias móviles con diferentes parámetros, que se utilizan respectivamente para determinar la tendencia, identificar soporte/resistencia y realizar el trailing stop.

-

Luego, encuentra los puntos más altos y más bajos dentro de un período especificado como zonas de soporte y resistencia para la entrada. Cuando el precio rompe estos soportes o resistencias, se genera una señal.

-

La estrategia toma una señal de ruptura del punto más alto como señal de compra (largo) y una ruptura del punto más bajo como señal de venta (corto).

-

Después de entrar, la estrategia mantiene la posición utilizando el punto más bajo de la ruptura como nivel de stop loss.

-

Una vez que la posición entra en ganancias, el stop loss se convierte en un trailing stop basado en la media móvil. Cuando el precio cae por debajo de la media móvil, el stop se establece en el punto más bajo de esa vela.

-

Esto permite asegurar las ganancias mientras se da suficiente espacio a la posición para seguir la tendencia.

-

La estrategia también incorpora el Average True Range (ATR) para asegurar que las rupturas solo se ejecuten en rangos adecuados, evitando rupturas excesivamente extendidas.

Análisis de Ventajas de la Estrategia

-

Combina las dobles ventajas de la estrategia de ruptura y la estrategia de trailing stop basada en tendencia.

-

Puede comprar rupturas basándose en la tendencia de largo plazo, aumentando la probabilidad de ganancias.

-

La estrategia de stop loss protege la posición y al mismo tiempo le da suficiente espacio para operar.

-

Incorpora un filtro de volatilidad para evitar rupturas desfavorables excesivamente extendidas.

-

Es una operación automatizada, adecuada para seguimiento parcial.

-

Permite personalizar diferentes períodos de medias móviles para operar.

-

Permite ajustar de manera flexible el método de trailing stop.

Análisis de Riesgos de la Estrategia

-

Las estrategias de ruptura corren el riesgo de presentar falsas rupturas. Se puede flexibilizar la confirmación de la ruptura.

-

Se requiere suficiente volatilidad para generar señales de ruptura; en mercados laterales puede resultar ineficaz.

-

Algunas rupturas pueden ser demasiado breves para ser capturadas. Se puede reducir el marco temporal para encontrar más oportunidades.

-

El trailing stop en mercados oscilantes puede generar demasiadas paradas. Se puede ampliar la distancia del stop.

-

El filtro de volatilidad puede hacer perder algunas oportunidades. Se pueden reducir los parámetros del filtro.

Direcciones de Optimización de la Estrategia

-

Probar diferentes combinaciones de parámetros de medias móviles para encontrar los mejores parámetros.

-

Probar diferentes mecanismos de confirmación de ruptura, como canales, patrones de velas, etc.

-

Experimentar con diferentes métodos de trailing stop para encontrar el mejor.

-

Optimizar la estrategia de gestión de capital, como el puntaje de posición (position score).

-

Incorporar filtros de indicadores técnicos estadísticos para mejorar la precisión del filtro.

-

Probar la efectividad de la estrategia en diferentes activos.

-

Incorporar algoritmos de aprendizaje automático para mejorar el rendimiento de la estrategia.

Conclusión

Esta estrategia integra el enfoque de ruptura y el enfoque de trailing stop basado en tendencia. Siempre que el juicio de largo plazo sea correcto, puede optimizar el espacio de ganancias. La clave es encontrar la mejor combinación de parámetros y combinarla con una buena estrategia de gestión de capital para aprovechar las oportunidades de largo plazo mientras se mantiene el riesgo controlado. Esta estrategia tiene el potencial de convertirse en una estrategia de tendencia de largo plazo más confiable mediante una mayor optimización.

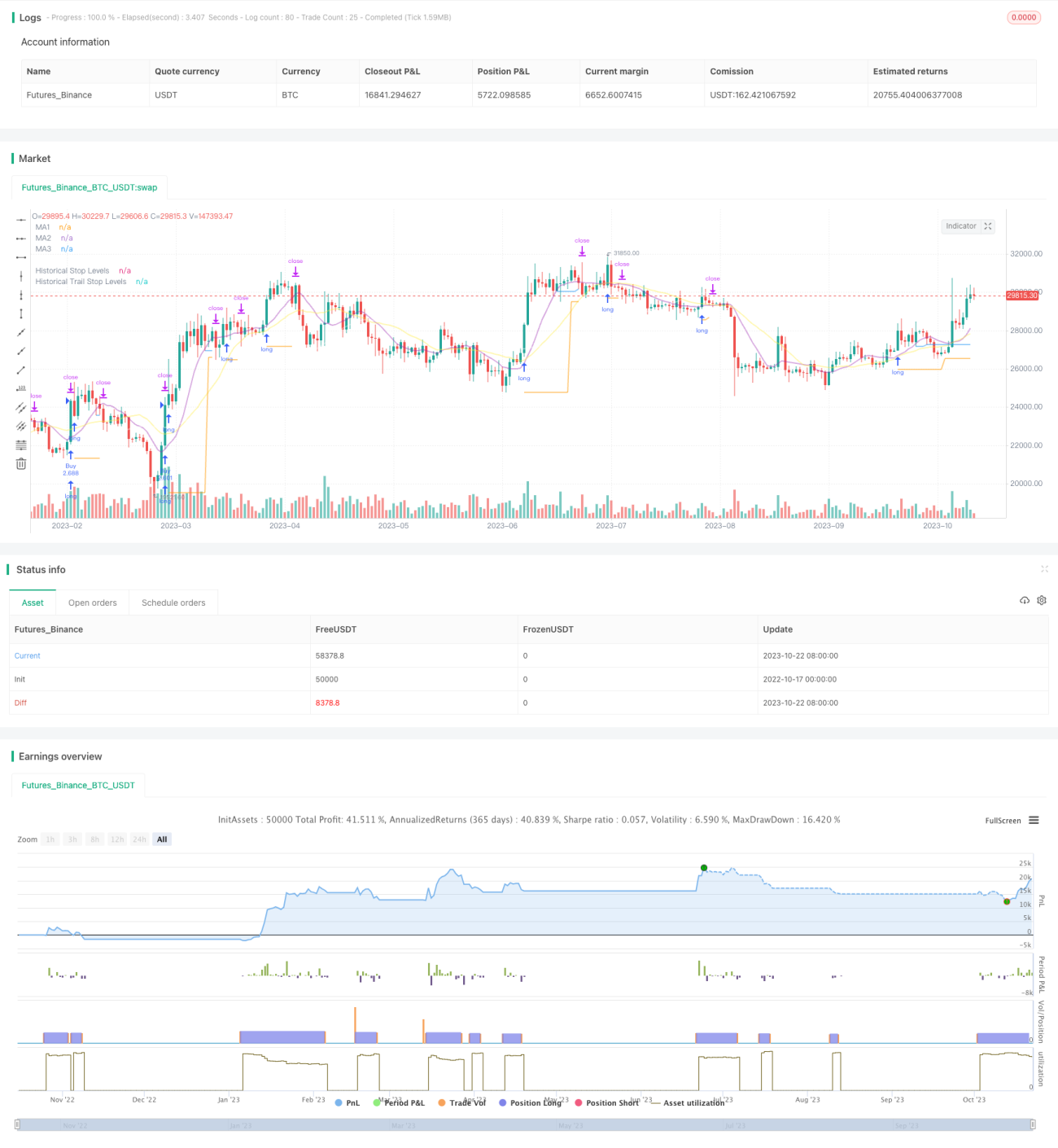

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1