Estrategia de trading bidireccional con líneas oscilantes dobles del RSI

Resumen

La estrategia de negociación bidireccional de líneas de oscilación de doble banda RSI es una estrategia que utiliza el indicador RSI para realizar operaciones en ambas direcciones. Basándose en el principio de sobrecompra y sobreventa del RSI, combinado con la configuración de doble banda y las señales de negociación de medias móviles, logra una apertura y cierre de posiciones eficientes en ambos sentidos.

Principio de la estrategia

La estrategia se basa principalmente en el principio de sobrecompra y sobreventa del indicador RSI para tomar decisiones de negociación. Primero calcula el valor del RSI (vrsi), así como la banda superior (sn) y la banda inferior (ln) de la doble banda. Cuando el valor del RSI cruza por debajo de la banda inferior ln, se genera una señal de compra; cuando cruza por encima de la banda superior sn, se genera una señal de venta.

La estrategia también detecta los cambios alcistas y bajistas de las velas, generando señales adicionales de compra y venta. Específicamente, cuando la vela rompe al alza, se genera una señal de compra (longLogic), y cuando rompe a la baja, se genera una señal de venta (shortLogic). Además, la estrategia ofrece parámetros que permiten operar solo en largo, solo en corto, o invertir las señales.

Tras generar las señales de compra y venta, la estrategia cuenta el número de señales para controlar el número de aperturas de posiciones. Mediante parámetros se pueden configurar diferentes reglas de adición de posiciones. Las condiciones de cierre incluyen take profit, stop loss, trailing stop loss, etc., y se pueden configurar diferentes porcentajes de take profit y stop loss.

En resumen, esta estrategia integra múltiples técnicas como el indicador RSI, cruces de medias móviles, adición de posiciones basada en conteo, take profit y stop loss, para lograr una negociación automática bidireccional.

Ventajas de la estrategia

- Utiliza el principio de sobrecompra y sobreventa del RSI para abrir posiciones largas y cortas en niveles razonables.

- La configuración de doble banda evita señales falsas. La banda superior impide el cierre prematuro de posiciones largas, y la banda inferior impide el cierre prematuro de posiciones cortas.

- Las señales de cruce de medias móviles filtran falsas rupturas. Solo se generan señales cuando el precio rompe la media móvil, evitando señales engañosas.

- Cuenta el número de señales y adiciones de posiciones para controlar el riesgo.

- Permite personalizar los porcentajes de take profit y stop loss, con riesgo y rentabilidad controlables.

- El trailing stop loss sigue la tendencia para asegurar ganancias adicionales.

- Posibilidad de operar solo en largo, solo en corto, o invertir señales, adaptándose a diferentes entornos de mercado.

- Sistema de negociación automatizado que reduce los costos de operación manual.

Riesgos de la estrategia

- El indicador RSI corre el riesgo de fallos en los giros. No siempre se produce un giro cuando el RSI entra en zona de sobrecompra o sobreventa.

- Los niveles fijos de take profit y stop loss pueden quedar atrapados. Una configuración inadecuada puede provocar un stop loss o take profit prematuros.

- Dependencia de indicadores técnicos, con riesgo de sobreoptimización de parámetros. Una mala configuración de los parámetros del indicador puede afectar el rendimiento de la estrategia.

- La activación simultánea de múltiples condiciones puede provocar órdenes perdidas.

- Los sistemas de negociación automatizados están expuestos a errores anómalos.

Para mitigar estos riesgos, se pueden optimizar los parámetros, ajustar las estrategias de stop loss/take profit, agregar filtros de liquidez, mejorar la lógica de generación de señales y aumentar la supervisión de errores anómalos.

Direcciones de optimización de la estrategia

- Probar diferentes parámetros de período para optimizar los parámetros del RSI.

- Probar diferentes configuraciones de porcentajes de take profit y stop loss.

- Agregar filtros de volumen de negociación o rendimiento para evitar problemas de liquidez.

- Optimizar la lógica de generación de señales, mejorando la forma de cruce de medias móviles.

- Realizar backtesting en múltiples marcos temporales para verificar la estabilidad.

- Considerar la inclusión de otros indicadores para optimizar la efectividad de las señales.

- Incorporar estrategias de gestión de posiciones.

- Agregar monitoreo de errores anómalos.

- Optimizar el algoritmo de trailing stop loss automático.

- Considerar la inclusión de aprendizaje automático para mejorar la estrategia.

Resumen

La estrategia de negociación bidireccional de líneas de oscilación de doble banda RSI, mediante la integración de múltiples técnicas como el indicador RSI, los principios de apertura estadística y stop loss, logra una negociación automática bidireccional. Esta estrategia ofrece una alta capacidad de personalización; los usuarios pueden ajustar los parámetros según sus necesidades para adaptarse a diferentes entornos de mercado. Al mismo tiempo, la estrategia tiene margen de mejora, que se puede optimizar en aspectos como la configuración de parámetros, las estrategias de control de riesgos y la lógica de generación de señales, para hacerla más estable y fiable. En general, esta estrategia proporciona a los usuarios una solución de trading cuantitativo relativamente eficiente.

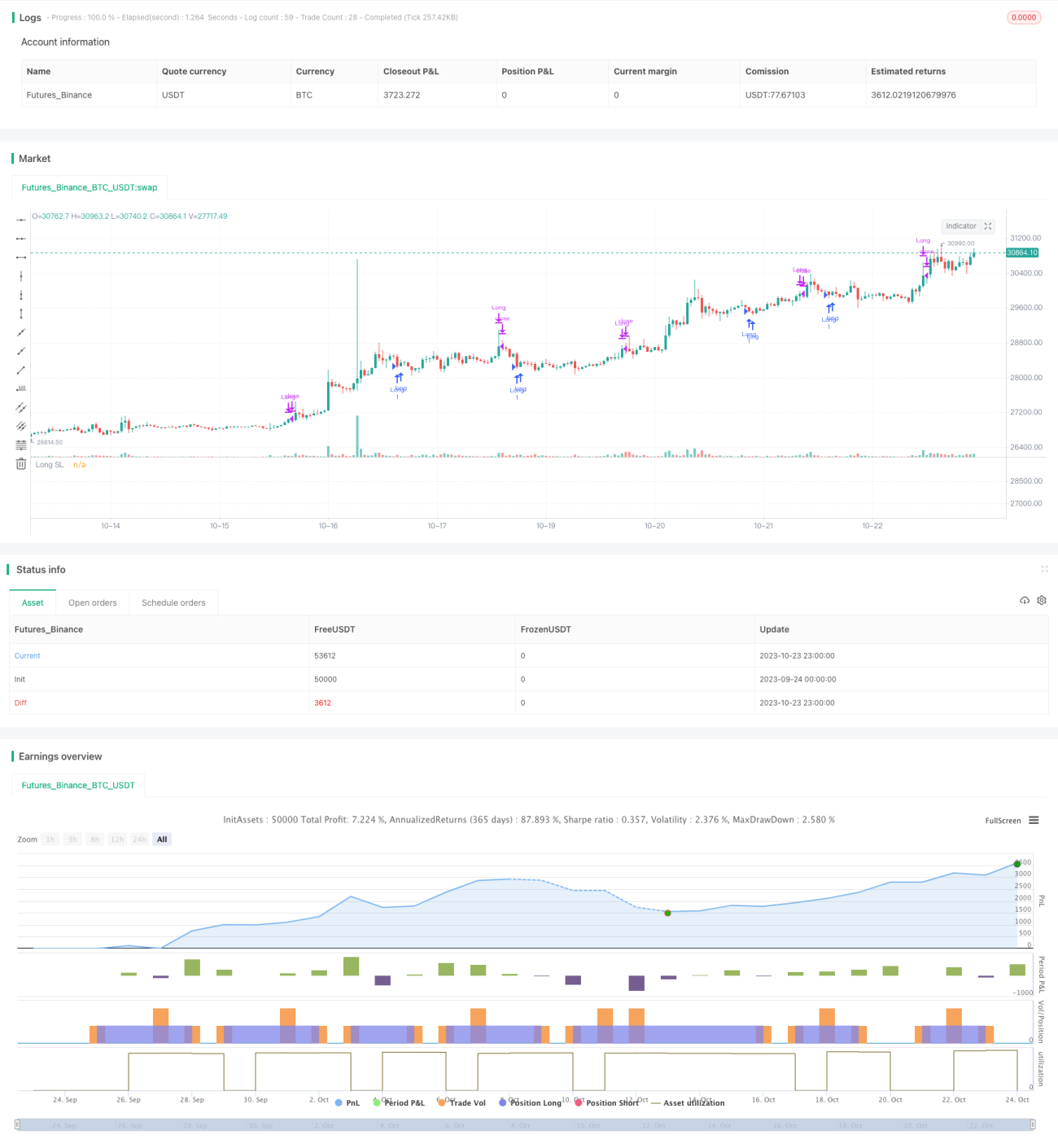

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1