Estrategia de tendencia a corto plazo basada en la decisión de indicadores multidimensionales

Resumen

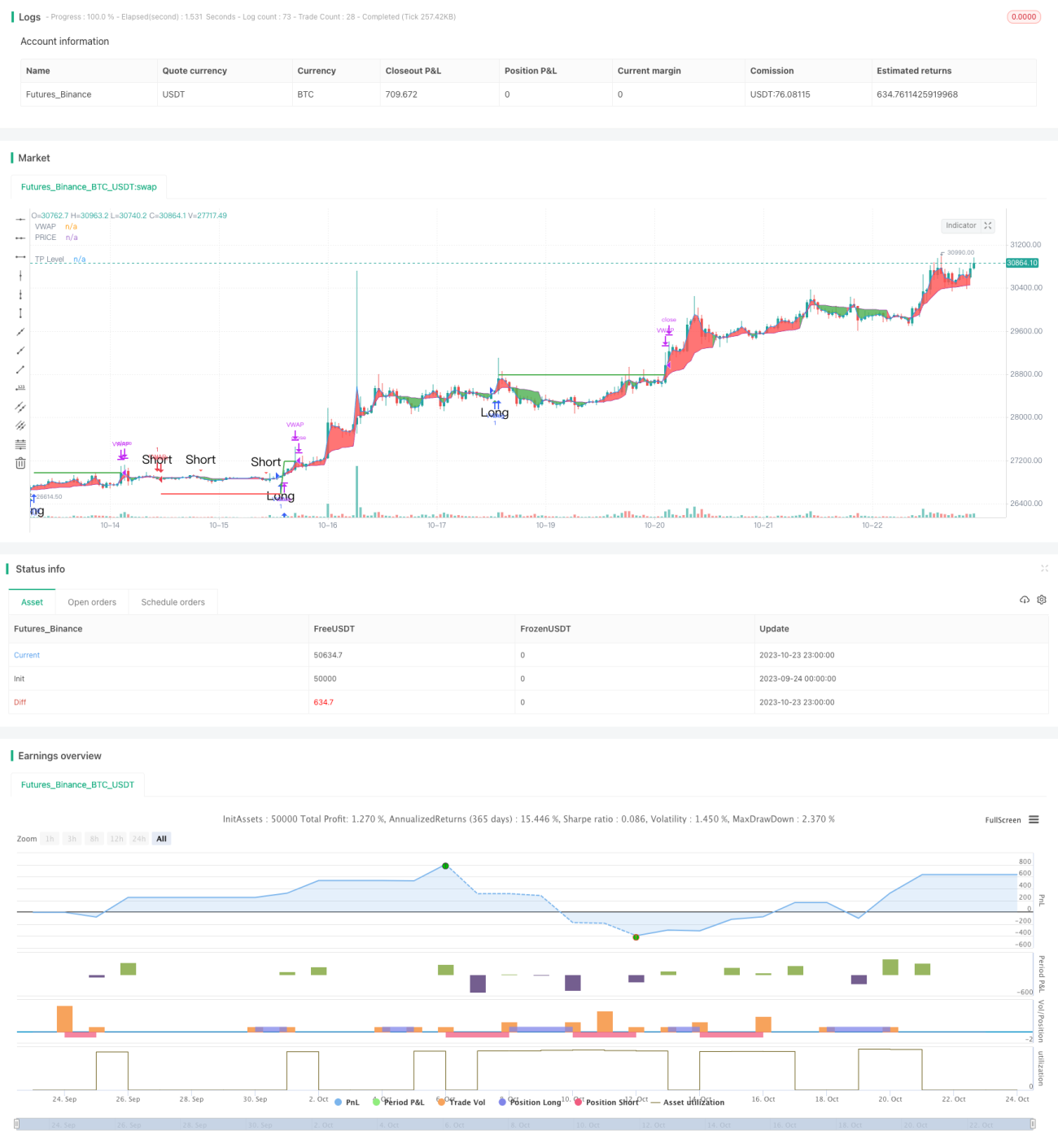

Esta estrategia combina tres indicadores técnicos de diferentes dimensiones: niveles de soporte y resistencia, sistema de medias móviles e indicadores de sobrecompra/sobreventa. Según sus señales integradas, determina la dirección de la tendencia a corto plazo para obtener una alta tasa de aciertos.

Principio de la Estrategia

En el código, primero se calculan los niveles de soporte y resistencia del precio, incluyendo el eje de oscilación estándar y los niveles de soporte y resistencia de Fibonacci, y se dibujan en el gráfico. Cuando el precio supera estos niveles clave, se considera una señal de tendencia importante.

A continuación, se calculan la media móvil ponderada por volumen (VWAP) y el precio promedio, identificando sus señales de cruce dorado y de cruce de muerte. Esto corresponde a un juicio de tendencia de medio a largo plazo.

Finalmente, se calcula el indicador Stochastic RSI, identificando sus señales de cruce dorado y de cruce de muerte, que es un indicador de sobrecompra/sobreventa.

Combinando estos tres indicadores, si los niveles de soporte/resistencia, la media VWAP y el Stochastic RSI emiten simultáneamente una señal de compra, se abre una posición larga; si los tres emiten simultáneamente una señal de venta, se abre una posición corta.

Análisis de Ventajas

La mayor ventaja de esta estrategia es que combina indicadores de tres dimensiones diferentes, lo que hace que el juicio sea más completo y preciso, con una alta tasa de aciertos. Primero, los niveles de soporte/resistencia determinan la tendencia general; segundo, el VWAP determina la tendencia a medio-largo plazo; y finalmente, el Stochastic RSI evalúa las condiciones de sobrecompra/sobreventa. Cuando los tres indicadores emiten señales simultáneamente, se filtran en gran medida las señales falsas, aumentando la tasa de éxito de las entradas.

Además, la estrategia incorpora una función de toma de ganancias, que permite fijar un porcentaje de ganancias, lo que favorece la gestión del capital.

Análisis de Riesgos

El principal riesgo de esta estrategia es que las decisiones de largos y cortos dependen de que los indicadores emitan señales sincronizadas. Si alguno de los indicadores emite una señal errónea, podría provocar una decisión incorrecta. Por ejemplo, si el Stochastic RSI emite una señal de sobrecompra pero el VWAP y los niveles de soporte/resistencia aún son alcistas, se podría perder un punto de compra y no entrar.

Además, una configuración inadecuada de los parámetros de los indicadores también puede provocar errores en las señales, por lo que es necesario realizar pruebas retrospectivas repetidas para encontrar los parámetros óptimos.

Asimismo, en el mercado de valores pueden aparecer eventos inesperados a corto plazo que hagan que los indicadores pierdan validez. Para mitigar este riesgo, se puede añadir una estrategia de stop loss para evitar pérdidas excesivas en una sola operación.

Direcciones de Optimización

Esta estrategia puede optimizarse en los siguientes aspectos:

-

Añadir más señales de indicadores, como el volumen de operaciones, para evaluar la fuerza de la tendencia y mejorar la precisión de las decisiones.

-

Incorporar modelos de aprendizaje automático para entrenar con indicadores multidimensionales y encontrar automáticamente la estrategia de negociación óptima.

-

Optimizar los parámetros según las diferentes variedades, configurando parámetros adaptativos.

-

Agregar una estrategia de stop loss y controlar el tamaño de la posición según la reducción, para gestionar mejor el riesgo.

-

Realizar una optimización de cartera, encontrando variedades con baja correlación para combinarlas y reducir la reducción de la cartera.

Conclusión

En general, esta estrategia es muy adecuada para el trading de tendencias a corto plazo. Utiliza indicadores multidimensionales para tomar decisiones, lo que permite filtrar gran parte del ruido y lograr una alta tasa de aciertos. Sin embargo, aún es necesario tener en cuenta el riesgo de que los indicadores emitan señales erróneas. Mediante una optimización continua, esta estrategia tiene el potencial de convertirse en una estrategia de corto plazo eficiente y estable.

- 1